Download to read offline

![9

0914000N

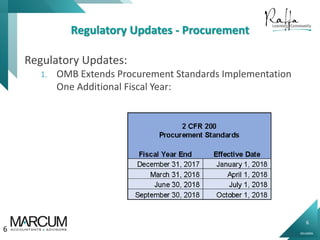

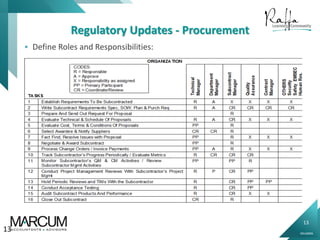

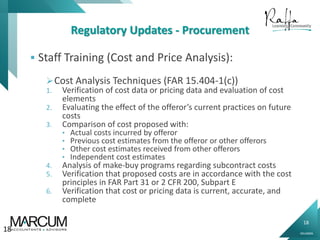

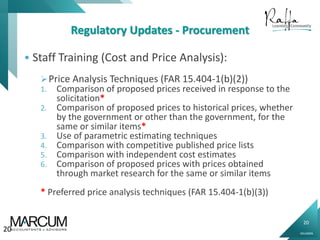

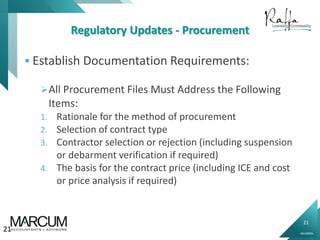

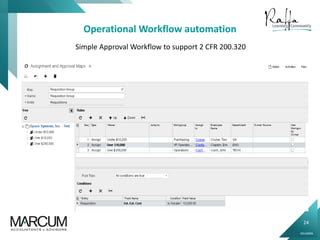

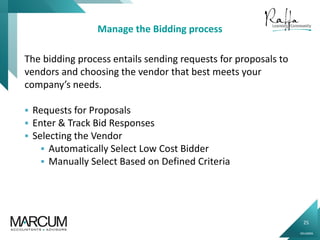

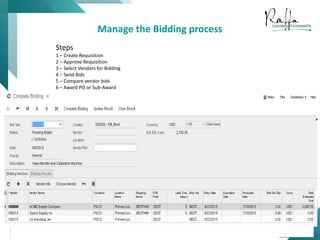

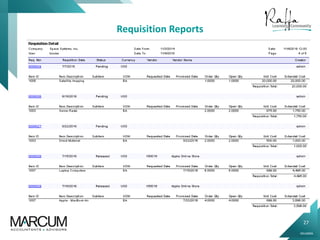

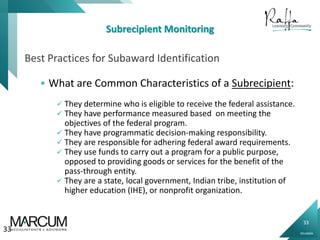

Regulatory Updates - Procurement

Most Common Pitfalls for Early Adopters:

3. The procurement was NOT supported by

documentation of justifiable rationale to limit

competition in those cases where competition was

limited [2 CFR sections 200.319 and 200.320(f) and 48

CFR section 52.244-5].

4. The procurement was NOT supported by a cost or price

analysis (for all procurement actions exceeding the

simplified acquisition threshold) (2 CFR section

200.323 and 48 CFR section 15.404-3).

9](https://image.slidesharecdn.com/2018-11-15compliaceissues-181115203521/85/2018-11-15-Compliance-Issues-9-320.jpg)

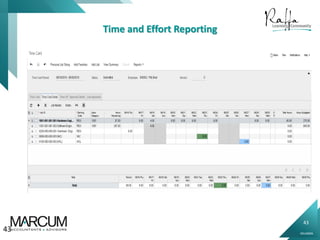

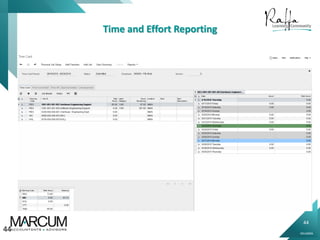

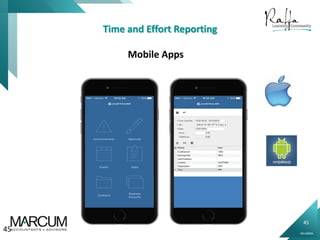

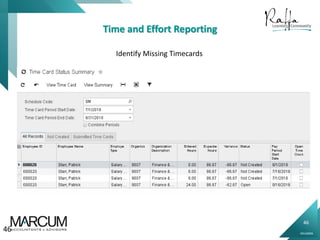

This document summarizes a presentation about high risk compliance issues for non-profits and how to avoid them. It discusses recent regulatory updates to procurement standards, subrecipient monitoring requirements, and time and effort reporting. It provides an overview of common pitfalls organizations experience with these topics. Best practices are presented for procurement workflows, identifying subawards versus contracts, and implementing compliant time tracking systems. The role of accounting systems in supporting compliance with these areas is also addressed.

![Getting Started with Apache Spark: Big Data Made Simple [Free Meetup]](https://cdn.slidesharecdn.com/ss_thumbnails/apachesparkgettingstarted-260203175547-8361bcc3-thumbnail.jpg?width=640&height=640&fit=bounds)