Downloaded 35 times

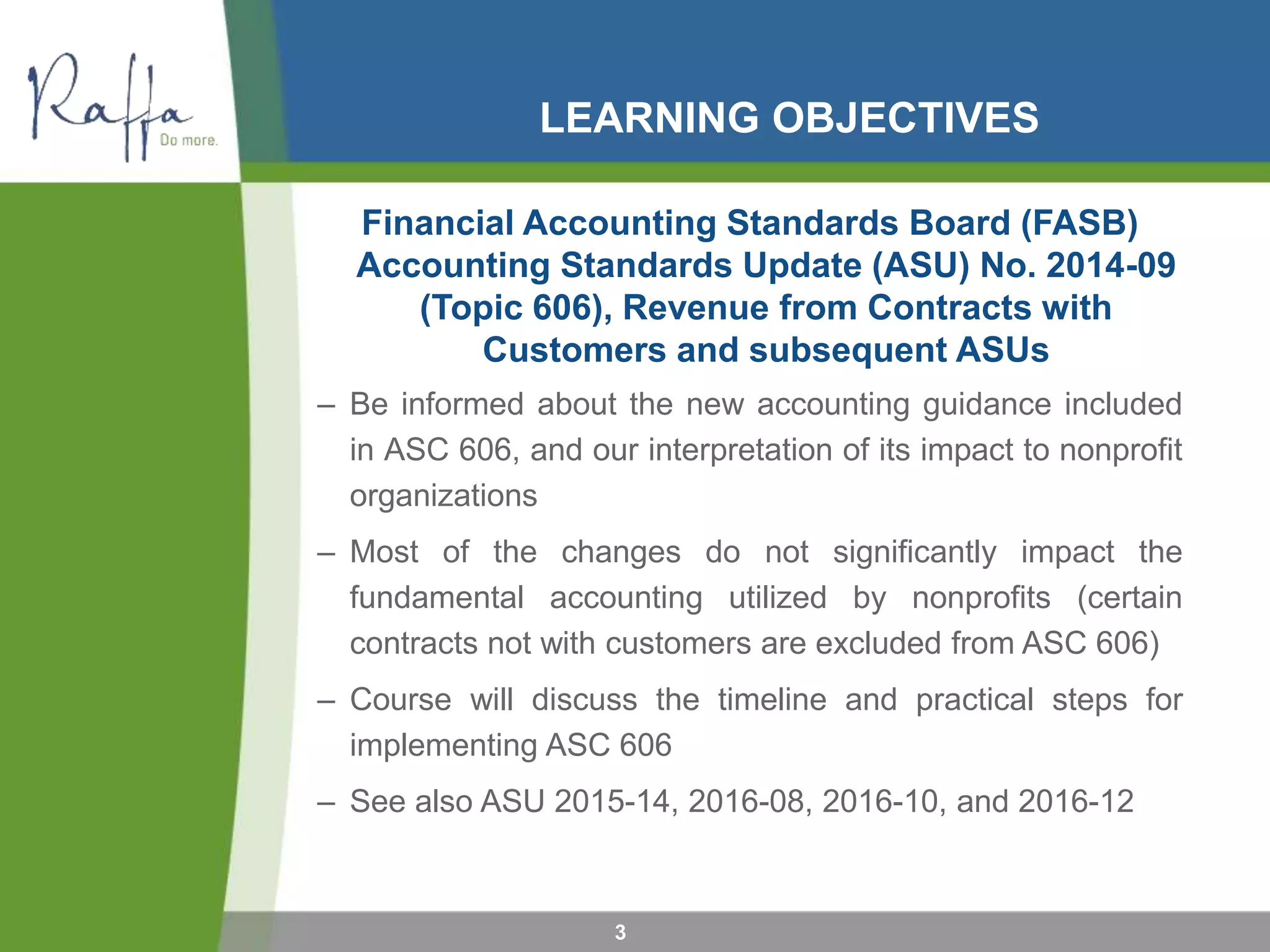

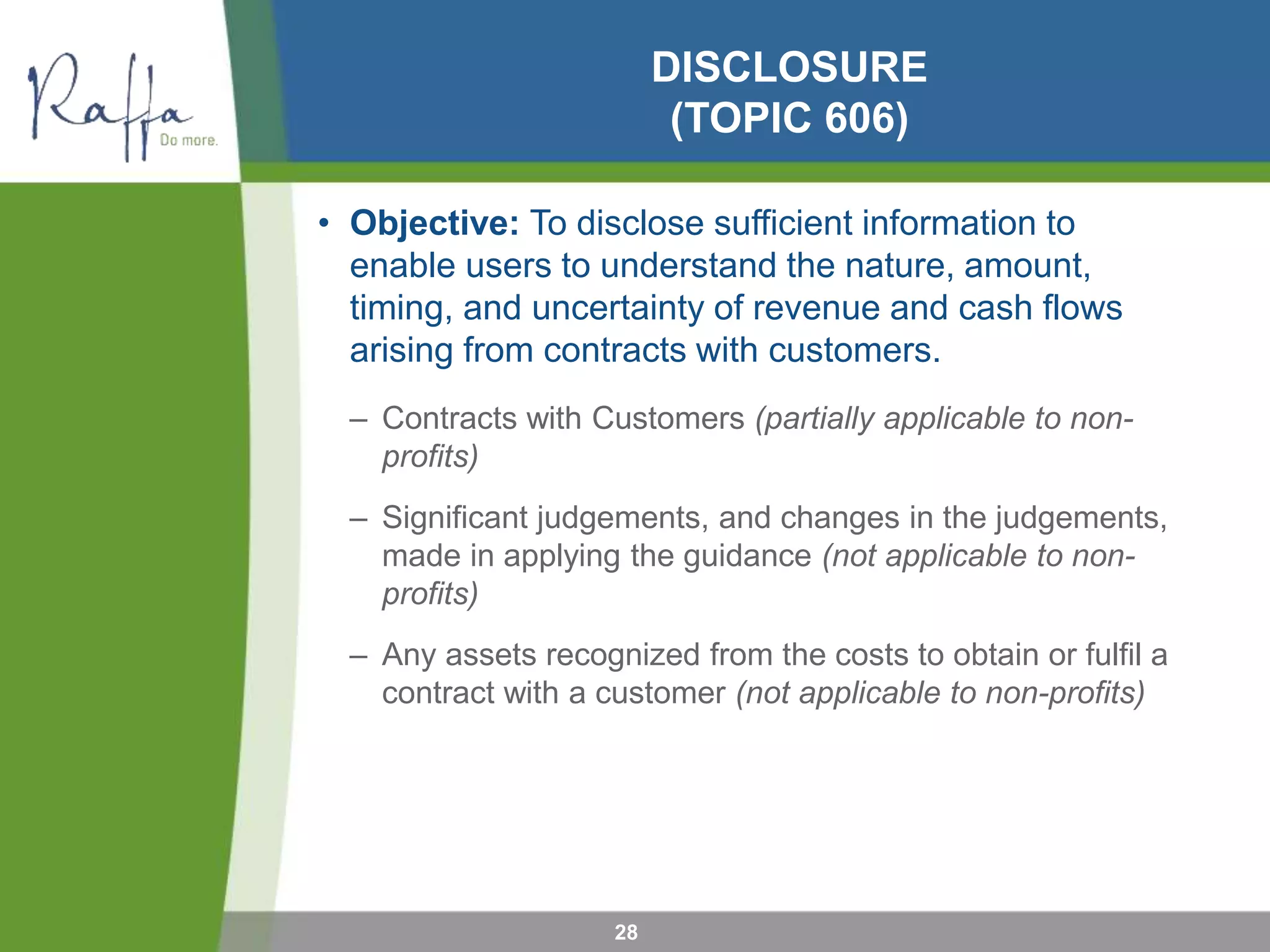

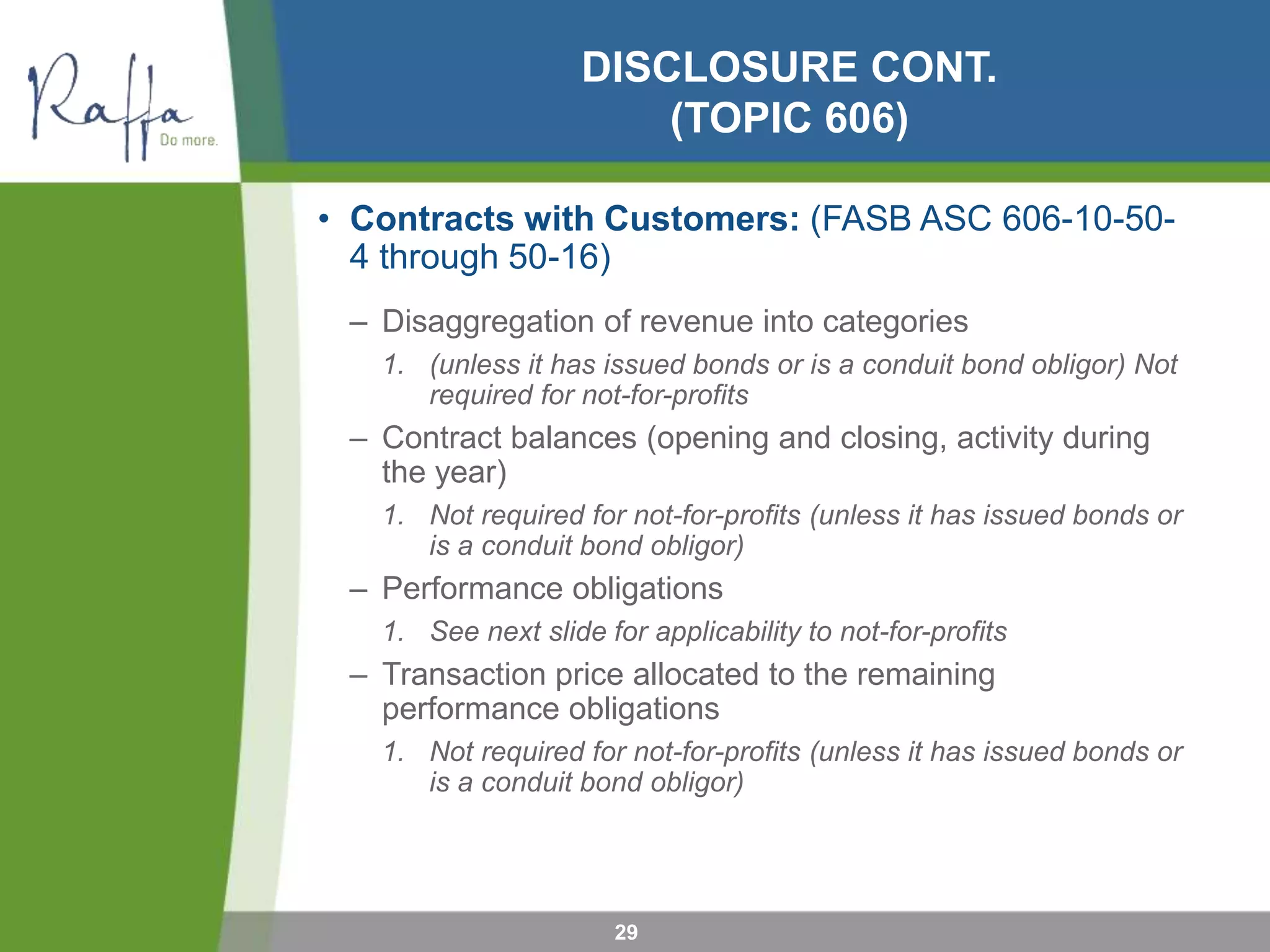

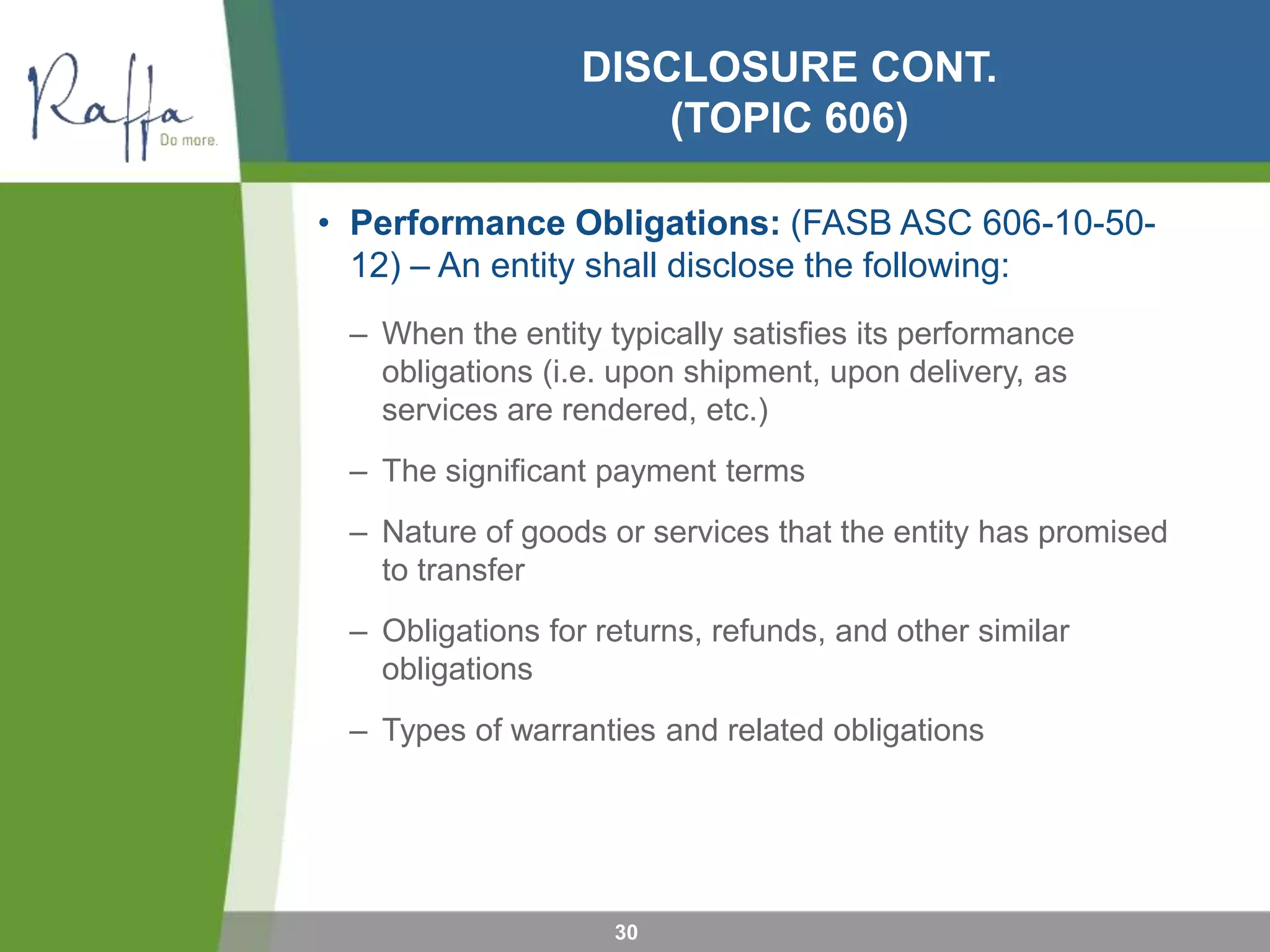

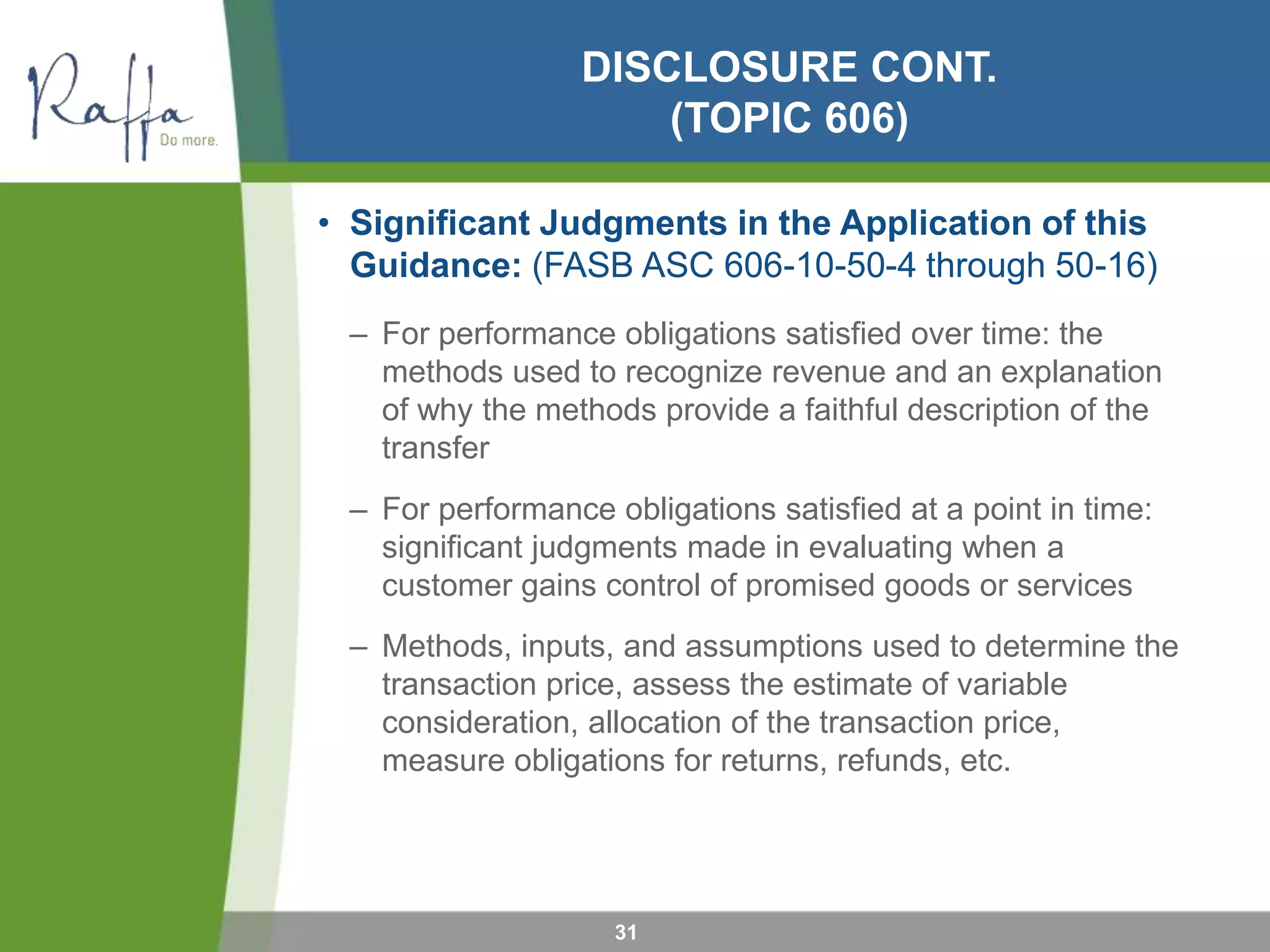

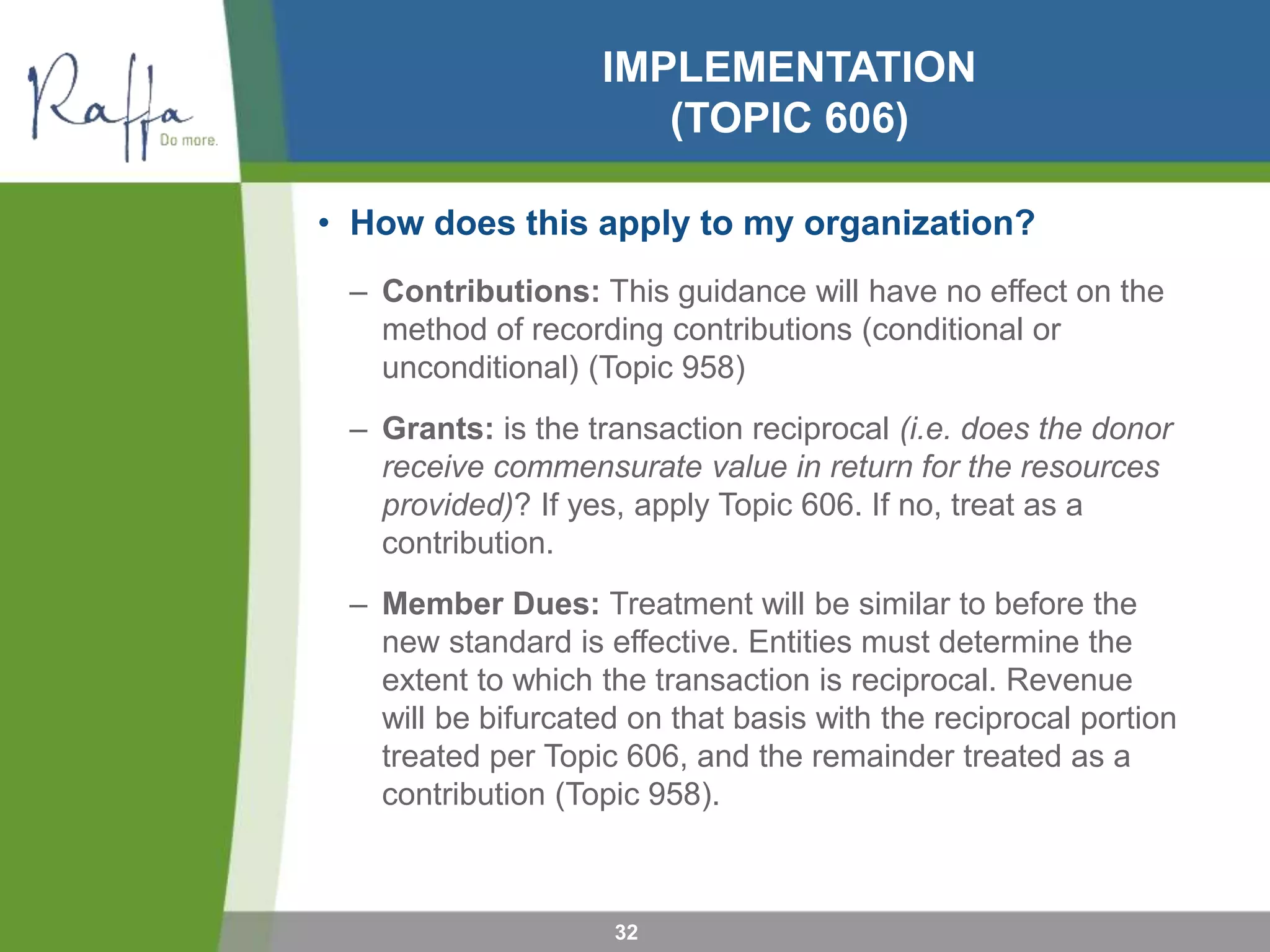

The document outlines the Financial Accounting Standards Board's (FASB) Accounting Standards Update (ASU) No. 2014-09 regarding revenue recognition from contracts with customers, which became mandatory for public entities after December 15, 2017, and for all other entities after December 15, 2018. It details a five-step process to apply the core principle of recognizing revenue based on contracts while also discussing specific exceptions and disclosure requirements applicable to both public and nonprofit organizations. The document emphasizes the importance of providing consistent and useful financial information while clarifying distinctions between contributions and exchange transactions.