Download as PDF, PPTX

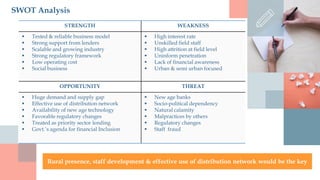

This document provides an investment memorandum for IGT Financial Services, a proposed social sector organization seeking equity investment. It outlines IGT's mission to improve quality of life for underprivileged communities. The organization will provide microfinance, microinsurance, and other services through a rural-focused NBFC-MFI model. Projections show the business growing to serve over 5 million customers within 5 years and generating annual revenue of over $90 million. The memorandum requests $2.3 million in seed funding and outlines plans for future funding rounds and exit opportunities.

![WFM Made easy (002)[3]](https://cdn.slidesharecdn.com/ss_thumbnails/62f603d8-e3d3-4ca0-a8b3-dceb949abf56-161212120540-thumbnail.jpg?width=640&height=640&fit=bounds)