Downloaded 66 times

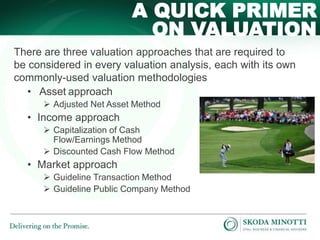

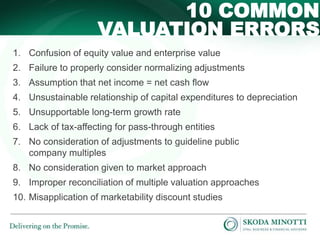

The document outlines 10 common errors in valuations and provides guidance on identifying and addressing these issues, as well as effectively cross-examining opposing experts. Key errors include confusing equity and enterprise value, failing to consider normalizing adjustments, and using unsupportable long-term growth rates. The document emphasizes the importance of proper valuation approaches and methodologies to avoid significant over- or undervaluation of businesses.