Download as PDF, PPTX

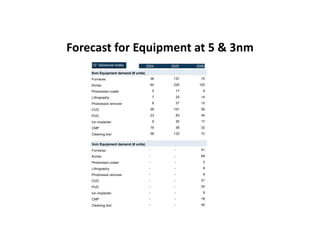

![Anji - CMP Competitors

• Cabot (tungsten, dielectrics, metal interconnect)

• DuPont (dielectrics, barrier metals, TSV [Through Silicon Via])

• Hitachi Chemical (barrier metals, TSV)

• Fujimi (dielectrics, barrier metals)

• Fuji Film (copper, barrier metals)

• Versum (advanced oxide STI barrier, copper strengthening, and tungsten

We estimate China’s CMP slurry consumption to grow by 39% CAGR from 23k tons in

2019 to 234k tons in 2026E, with a market size of US$150mn in 2019 to US$1.6bn in 2026E

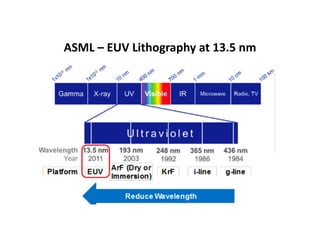

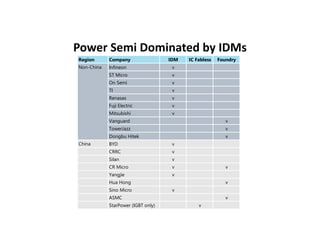

Exhibit 274: Anji vs. global peers CMP slurry offerings by logic node and memory

Company 130nm 65nm 45nm 28nm 20nm 16/14 nm 10nm 7nm 5nm 3D NAND 3D DRAM

Anji R&D R&D R&D

Cabot

Hitachi

Fujimi

Source: Company data

China Semiconductor

Wafer Fab Supplies](https://image.slidesharecdn.com/chipindustrytutorialv7-211015225805/85/Semiconductor-Industry-Tutorial-187-320.jpg)

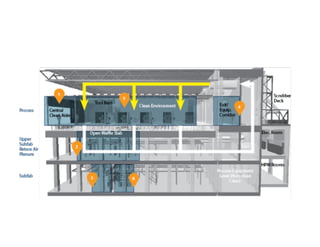

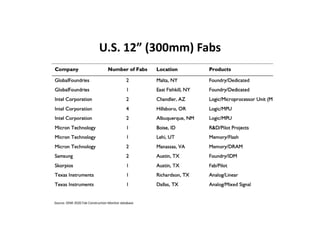

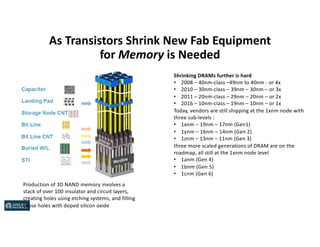

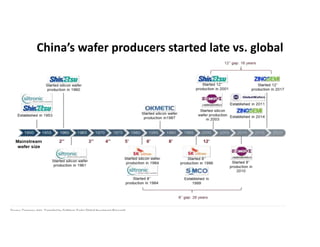

The document provides an extensive overview of the semiconductor industry, detailing its ecosystem, including chip design and manufacturing processes, as well as various types of companies like fabless firms, integrated device manufacturers, and foundries. It also discusses specific technologies and materials involved in chip fabrication, the significance of advancements in manufacturing nodes, and the trusted foundry program managed by the DOD. In addition, it outlines current trends in the industry, such as new fab constructions and key players in the global semiconductor market.