Downloaded 378 times

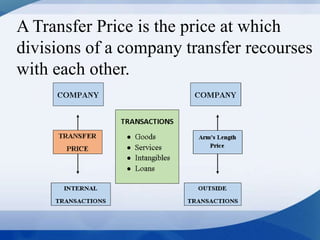

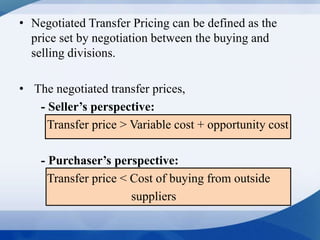

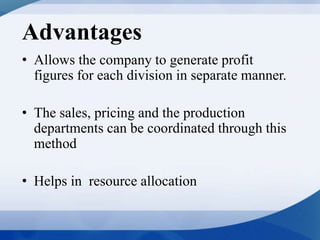

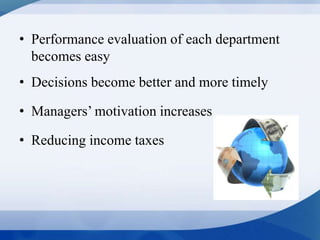

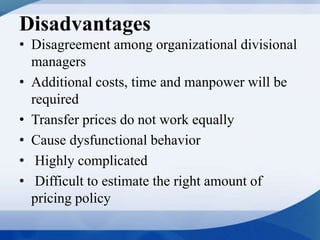

The document discusses the concept of transfer pricing, which is the price at which company divisions trade resources. It outlines various methods of transfer pricing, such as cost-based, market-based, and negotiated pricing, along with their advantages and disadvantages. The objectives of transfer pricing include minimizing tax liability, maintaining divisional autonomy, and enhancing competitive positioning.