( Jasmin ) Top VIP Escorts Service Dindigul 💧 7737669865 💧 by Dindigul Call G...

Market Outlook - July 26, 2010

1. Market Outlook

India Research

July 26, 2010

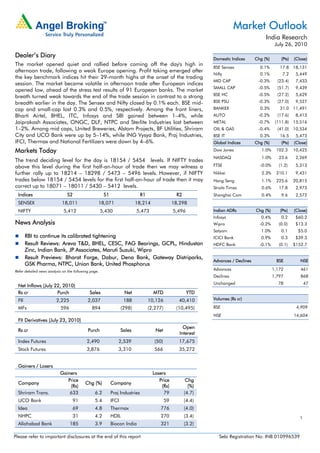

Dealer’s Diary Domestic Indices Chg (%) (Pts) (Close)

The market opened quiet and rallied before coming off the day's high in

BSE Sensex 0.1% 17.8 18,131

afternoon trade, following a weak Europe opening. Profit taking emerged after

Nifty 0.1% 7.2 5,449

the key benchmark indices hit their 29-month highs at the onset of the trading

MID CAP -0.3% (23.4) 7,433

session. The market became volatile in afternoon trade after European indices

SMALL CAP -0.5% (51.7) 9,439

opened low, ahead of the stress test results of 91 European banks. The market

breath turned weak towards the end of the trade session in contrast to a strong BSE HC -0.5% (27.2) 5,629

breadth earlier in the day. The Sensex and Nifty closed by 0.1% each. BSE mid- BSE PSU -0.3% (27.0) 9,527

cap and small-cap lost 0.3% and 0.5%, respectively. Among the front liners, BANKEX 0.3% 31.0 11,491

Bharti Airtel, BHEL, ITC, Infosys and SBI gained between 1–4%, while AUTO -0.2% (17.6) 8,413

Jaiprakash Associates, ONGC, DLF, NTPC and Sterlite Industries lost between METAL -0.7% (111.8) 15,516

1–2%. Among mid caps, United Breweries, Alstom Projects, BF Utilities, Shriram OIL & GAS -0.4% (41.0) 10,534

City and UCO Bank were up by 5–14%, while ING Vysya Bank, Praj Industries, BSE IT 0.3% 16.5 5,473

IFCI, Thermax and National Fertilizers were down by 4–6%. Global Indices Chg (%) (Pts) (Close)

Markets Today Dow Jones 1.0% 102.3 10,425

NASDAQ 1.0% 23.6 2,269

The trend deciding level for the day is 18154 / 5454 levels. If NIFTY trades

above this level during the first half-an-hour of trade then we may witness a FTSE -0.0% (1.2) 5,313

further rally up to 18214 – 18298 / 5473 – 5496 levels. However, if NIFTY Nikkei 2.3% 210.1 9,431

trades below 18154 / 5454 levels for the first half-an-hour of trade then it may Hang Seng 1.1% 225.6 20,815

correct up to 18071 – 18011 / 5430 – 5412 levels. Straits Times 0.6% 17.8 2,973

Indices S2 S1 R1 R2 Shanghai Com 0.4% 9.6 2,572

SENSEX 18,011 18,071 18,214 18,298

NIFTY 5,412 5,430 5,473 5,496 Indian ADRs Chg (%) (Pts) (Close)

Infosys 0.4% 0.2 $60.2

News Analysis Wipro -0.2% (0.0) $13.3

Satyam 1.0% 0.1 $5.0

RBI to continue its calibrated tightening ICICI Bank 0.9% 0.3 $39.3

Result Reviews: Areva T&D, BHEL, CESC, FAG Bearings, GCPL, Hindustan HDFC Bank -0.1% (0.1) $152.7

Zinc, Indian Bank, JP Associates, Maruti Suzuki, Wipro

Result Previews: Bharat Forge, Dabur, Dena Bank, Gateway Distriparks,

Advances / Declines BSE NSE

GSK Pharma, NTPC, Union Bank, United Phosphorus

Refer detailed news analysis on the following page.

Advances 1,172 461

Declines 1,797 868

Unchanged 78 47

Net Inflows (July 22, 2010)

Rs cr Purch Sales Net MTD YTD

FII 2,225 2,037 188 10,126 40,410 Volumes (Rs cr)

MFs 596 894 (298) (2,277) (10,495) BSE 4,909

NSE 14,604

FII Derivatives (July 23, 2010)

Open

Rs cr Purch Sales Net

Interest

Index Futures 2,490 2,539 (50) 17,675

Stock Futures 3,876 3,310 566 35,272

Gainers / Losers

Gainers Losers

Price Price Chg

Company Chg (%) Company

(Rs) (Rs) (%)

Shriram Trans. 633 6.2 Praj Industries 79 (4.7)

UCO Bank 91 5.4 IFCI 59 (4.4)

Idea 69 4.8 Thermax 776 (4.0)

NHPC 31 4.2 HDIL 270 (3.4) 1

Allahabad Bank 185 3.9 Biocon India 321 (3.2)

Please refer to important disclosures at the end of this report Sebi Registration No: INB 010996539

2. Market Outlook | India Research

RBI to continue its calibrated tightening

Signs of a revival in growth momentum are increasing, with IIP growth at 11.5% in May

2010. At the same time, food inflation (12.6% yoy) has taken the overall WPI in double

digits at 10.6%. We believe the engines of growth are clearly shifting from government-

driven consumption to risk capital-driven private consumption and investments. Hence, the

RBI’s priority is likely to be controlling inflation using monetary policy tools. Accordingly, we

expect the RBI to hike repo and reverse repo rates by 25bp each to 5.75% and 4.25%,

respectively. However, considering the current liquidity situation, we do not expect a CRR

hike in the coming policy.

Result Reviews-1QFY2011

Areva T&D-2QCY2010

Areva T&D India announced its results. The company posted top-line growth of 10.3% yoy

to Rs885.4cr (Rs802.4cr), which was below our estimates. On the operating front, the

company extended its weak performance reporting a sharp dip in EBITDA margin by

410bps to 9.2% (13.3%). Consequently, net profit for the quarter plunged by 35.6% yoy to

Rs32.2cr (Rs50.1cr). We maintain our Neutral recommendation on the stock.

BHEL

Bharat Heavy Electricals Ltd. (BHEL) came out with its results. Top line for the quarter grew

by 16% yoy to Rs6,480cr (Rs5597cr), which was below our estimates. Segment-wise, the

power segment posted revenue growth of 18% yoy to Rs5,400cr (Rs4,568cr), whereas the

industry segment grew by modest 11% to Rs1,476cr (Rs1,332cr). The bottom line

increased by a healthy 42% yoy to Rs667cr (Rs470cr). We maintain our Neutral

recommendation on the stock.

CESC

CESC registered 33.7% yoy growth in its standalone top line to Rs1,096cr, aided by a

10.9% yoy increase in sales volume to 2,321MU. Growth in sales volume was due to the

recent commissioning of the 250MW Budge-Budge plant and marginally higher PLFs in

Titagarh and southern plants. Growth in top line was also aided by higher tariff

Rs4.57/unit charged by the company in the Kolkata regulated area as against Rs3.91/unit

in 1QFY2010. However, the company's OPM declined by 119bp yoy to 23.7%. On the

bottom-line front, the company’s standalone net profit grew by a marginal 4.8% yoy to

Rs110cr. The per sq. ft. sales of the company’s retail subsidiary Spencers’ stood at Rs906

in June 2010, up by 23.1% on a yoy basis. Further, management has indicated that the

store EBITDA/sq. ft. for Spencers’ has turned positive in June 2010. We maintain a Buy

view on the stock with a target price of Rs460.

July 26, 2010 2

3. Market Outlook | India Research

FAG Bearing - 2QCY2010

FAG Bearing (FAG) recorded robust performance in 2QCY2010. FAG reported net sales

growth of 34.7% yoy to Rs273cr (Rs202cr), above our expectations of Rs244cr. This was

largely driven by a substantial jump in overall auto volume and sharp recovery in the

industrial bearing segment. EBITDA margins expanded by a substantial 364bp yoy to

19.1% (15.5%), basically due to the decrease in raw material costs by 558bp during the

quarter and better operating leverage. For 2QCY2010, FAG registered 81.6% yoy

increase in bottom line to Rs33.8cr (Rs18.6cr) largely on account of robust top-line growth

and substantial jump in operating performance. Further, higher other income and lower

tax rate aided robust net profit growth to a certain extent, which helped the company to

register NPM of 12.4% (9.2%).

We have revised our estimates upward: 1) ~9% upward revision in revenue to account

robust top-line growth in 2QCY2010, 2) higher OPM on better operating leverage and 3)

~30% revision in earnings. We believe that the company will register a CAGR of around

20% in net sales and 33% in net profit over CY2009–11E. We maintain Buy on the stock

with a target price of Rs931, at which it will trade at a multiple of 12x its earnings.

Godrej Consumer Products

Godrej Consumer (GCPL) reported strong top-line growth at 47% yoy to Rs643cr (Rs439cr)

driven largely by consolidation of recent acquisitions (Megasari, Tura, Issue and Argencos)

and remaining 51% consolidation of GHPL. Domestic business registered a growth of 35%

yoy to Rs457cr (Rs338cr) largely aided by six weeks consolidation of 100% GHPL revenue.

We estimate Soaps registered a ~7-9% yoy decline and Hair colours registered a ~2% yoy

decline during the quarter. International business stood at Rs186cr (Rs101cr) registering a

growth of 84% yoy aided by Rs83cr revenue from Megasari (consolidated for six weeks)

and Rs12cr revenue from Issue (consolidated for only 1 month). GCPL’s consolidated

earnings on a recurring basis registered a muted growth of 9% yoy to Rs76cr (Rs70cr),

despite strong top-line growth, impacted by margin contraction, 178% yoy spike in interest

costs to Rs10.5cr (Rs3.8cr), 62% yoy jump in depreciation to Rs8.4cr (Rs5.2cr) and 254bp

rise in tax rate. However, on a reported basis, earnings registered a growth of 67% yoy to

Rs116cr (Rs70cr) largely aided by Rs40cr exceptional income on account of compensation

received by GHPL from Sara Lee International on termination of manufacturing and

distribution license agreement. At the operating front, GCPL delivered a margin

contraction of 117bp yoy on account of 319bp contraction in gross margins. Nonetheless,

58bp drop in other expenses and 168b drop in staff costs arrested further margin decline.

GCPL has completed consolidation of all its recent acquisitions during the quarter (except

for Argencos which was completed on 8th July, 2010). We estimate the total cost of these

acquisitions at ~Rs2,550cr and the company has funded the same via – 1) US$350mn of

debt, 2) Rs700cr of NCDs , 3) Rs531cr via QIP leading to ~5% dilution (to be used to

repay NCDs) and 4) internal accruals and cash. The management has constantly re-

iterated that all recent acquisitions have been EPS accretive and debt-equity ratio is to be

maintained at comfortable 1:1 level. We believe the acquisitions are in-line with GCPL’s

3x3 strategy and have leapfrogged the company into a truly global presence. We maintain

Accumulate on the stock (Target price under review, to be decided post Concall with the

management today).

July 26, 2010 3

4. Market Outlook | India Research

Hindustan Zinc

Hindustan Zinc’s 1QFY2011 net revenue grew by 29.0% to Rs1,951cr, below our

estimates of Rs2,392cr. Deviation in the top line was on account of 1) low-grade

production at Rampura Agucha mine, 2) production impacted due to water shortage and

3) absence of concentrate sales. Although zinc sales volumes were higher 19.2% yoy to

164,445 tonnes, lead sales volumes were lower by 6.6% yoy to 14,075 tonnes. However,

higher zinc (up 34.3% yoy) and lead (up 28.5%) realizations partially negated the negative

impact of lower production. Despite strong top-line growth, operating margins were flat

yoy at 52.4%, mainly due to higher 1) mining and manufacturing costs (increased

stripping, coal and coke costs), 2) consumption of stores and spares and 3) staff cost

(impact of wage settlement). Consequently, EBITDA came in at Rs1,022cr, higher by 30.6%

yoy. Net profit increased by 23.9% yoy to Rs891cr, below our estimates of Rs1,158cr. At

the CMP of Rs988, the stock is trading at 5.6x FY2011E and 3.5x FY2012E EV/EBITDA. We

maintain a Buy view on the stock with a revised target price of Rs1,227, valuing the stock

at 6x FY2012E EV/EBITDA.

Indian Bank

Indian Bank has announced its results, wherein it has registered net profit growth of 11.0%

on a yoy basis to Rs368cr, which is better than our estimate of Rs342cr mainly on account

of better-than-estimated non-interest income and lower effective tax rate. Operating

performance came on expected lines, but a severe pressure on asset quality was the key

highlight of the result. NII increased 25.6% yoy but was down marginally by 0.8% qoq to

Rs927cr. Non-interest income stood at Rs355cr, up 21.4% yoy. Operating costs declined

2.9% yoy but were up 25.3% qoq to Rs444cr. The cost-to-income ratio stood at 34.7%,

lower than its eight-quarter average of 39.1%. The bank provided Rs8.2cr towards

additional gratuity-related liability.

In line with our view on select PSU banks, Indian Bank’s asset quality deteriorated

substantially during the quarter. Gross NPA increased by 93.8% sequentially to Rs988cr,

while net NPA stood at Rs511cr compared to Rs145cr (a sharp rise of 252.9%) in

4QFY2010. The bank’s gross and net NPA ratios stood at 1.5% (0.8% in 4QFY2010) and

0.8% (0.2% in 4QFY2010), respectively. The provision coverage ratio (without tech write-

offs) declined to 48.3% compared to 71.6% in 4QFY2010 and 56.6% in 1QFY2010. The

bank’s CAR decreased to 12.5% as compared to 12.7% in 4QFY2010 and 14.2% in

1QFY2010.

At the CMP, the stock is trading at 1.2x FY2012E ABV. Since the listing in March 2007, the

stock has traded in the range of 0.9–1.2x P/ABV, with an average multiple of 0.9x. In a

rising interest rate environment, the bank’s NIM is not sustainable at the current high

levels, in our view, given a relatively lower CASA of 32%. We have a Neutral rating on the

stock.

July 26, 2010 4

5. Market Outlook | India Research

JP Associates

JAL reported a robust top-line growth of 51.8% yoy to Rs3,215cr (Rs2,117cr), significantly

ahead of our estimates of ~31.7% growth, aided by a strong 52.0% and 36.8% growth in

cement and construction revenue to Rs1,442cr (Rs948cr) and Rs1,437cr (Rs1051cr),

respectively. JAL’s recurring earnings for the quarter declined by 57.6% to Rs105cr, which

was way below our expectations of Rs229cr. This was mainly on account unexpected

plunge in margins for both the segments (cement and construction). We were expecting

margins to be under pressure for the cement segment but the numbers were way below

our expectations mainly on account competitive pressures due to oversupply in markets.

Further, the house construction segment also faced margin pressure due to stoppage of

work at Baglihar II and Srisailam canal projects. Against this backdrop, we are factoring

margins to be under pressure for the coming quarters. JAL is one of the leading companies

in the infra space spread across verticals of Cement, Construction, Power, Real Estate and

Hospitality and a major beneficiary of the ongoing thrust in infrastructure development. We

believe that JAL would be one of the fastest growing companies and would post a top-line

and bottom-line CAGRs of 33.2% and 43.6%, respectively, over

FY2010-12E. We have valued JAL on an SOTP basis and maintain a buy with a target

price of Rs174.

Maruti Suzuki

For 1QFY2011, Maruti registered 27% yoy growth in net sales to Rs8,232cr (Rs6,493cr),

below our expectations. Volumes for the quarter increased 25% yoy, while realisations

increased by meager 2% for the quarter. Average realisations, however, declined

sequentially (qoq) by 1%, largely owing to currency (Euro) impact coming on export

revenue, which stood at Rs1,130cr (Rs1,283cr in 4QFY2010), while average export

realisation declined by almost 8.4% qoq to Rs2.79lakh (Rs3.05lakh in 4QFY2010).

On the operating front, EBITDA margins came in substantially lower than our expectations

owing to higher raw material costs (increased by 150bp yoy) and a substantial increase in

royalty (up 230bp yoy) to 5.9% of net sales (includes one-time arrears of FY2010

amounting to 0.8% of net sales). Royalty charges increased substantially due to the

increase in sales of K-series engine models and amendments in the various royalty

agreements the company entered with Suzuki Motor Corporation, resulting in additional

royalty expense of Rs188.7cr, including Rs65.2cr for the period: December 16, 2009, to

March 31, 2010. Net profit declined to Rs465cr, a dip of 20% yoy and below our

expectations. Lower export realisations, substantial contraction in EBITDA margins, higher

depreciation and lower-than-expected other operating income led to a substantial decline

in net profit yoy and qoq.

Owing to the lower-than-expected 1QFY2011 performance, we will be revising our

estimates downward by 11–12%, which would consequently lead to about 11–12%

downward revision in our target price. The stock rating is under review.

July 26, 2010 5

6. Market Outlook | India Research

Wipro

Wipro reported strong 1QFY2011 performance by witnessing 3.1% qoq (12.6% yoy) top-

line growth in rupee terms backed by 4.6% qoq (14% yoy) growth in IT services revenue.

The IT services topline was driven by 4.7% qoq growth in volumes despite of decline in

price realisations. In US Dollar terms, the company posted IT services revenue of US$

1204mn as against guidance given in the range of US$1,190mn-1,215mn. The EBIDTA

margins expanded by 92bp qoq (196bp yoy) despite of higher employee cost incurred and

decline in pricing. This was mainly due to a positive impact of 60bp on account of effective

hedges, which contained the adverse currency impact on the EBIDTA margins during the

quarter. Though the other income declined by 26.9% qoq (up 35.8% yoy) and the interest

cost increased by 70% qoq, the effective tax rate was down from 20% in 4QFY10 to 15%

in 1QFY2011. Thus, on net level, the company witnessed 9% qoq (30.5% yoy) increase in

bottom line backed by strong operational efficiency. Despite challenging macro-economic

indicators, the company’s management has given strong revenue guidance for the IT

services segment in 2QFY2011, which is expected to be in the range of US $1,253mn-

1,277mn, sequential growth of 4.1-6.1%. Hence, we maintain Accumulate on the stock.

Result Previews-1QFY2011

Bharat Forge

Bharat Forge is slated to announce its results today. The company is expected to post 59%

yoy growth in revenue to Rs559cr for the quarter. On the operating front, the company is

expected to post a 355bp yoy improvement in operating profit margin to 24.4%. Net profit

is expected to increase substantially by 239% yoy to Rs53.6cr. The stock rating is under

review.

Dabur India

Dabur is slated to announce its numbers. For the quarter, we expect robust consolidated

top-line growth of 16.5% yoy to Rs865cr. The company completed the acquisition of Fem

Care Pharma with itself during the quarter and has allotted Dabur’s shares to Fem Care

Pharma’s shareholders in the ratio of 5:1. Bottom line is expected to register growth of

26.3% yoy to Rs115.4cr, aided by top-line growth and margin expansion of 839bp yoy.

We maintain a Neutral view on the stock.

Dena Bank

Dena Bank is slated to declare its results. The bank is expected to post NII growth of 18.6%

yoy to Rs297cr. NIM is expected to dip by around 25bp on account of change in the

method of calculating interest on savings account balances. Growth in operating income is

expected to be flat at around 4%. Net profit growth is also expected to be muted at 4% yoy

to Rs120cr. We will be closely watching slippages from the bank’s restructured loans,

which stand at Rs1,330cr—forming 3.8% of advances (51.1% of the net worth). At the

CMP, the stock is trading at attractive valuations of 4.6x FY2012E EPS of Rs21.9 and 0.8x

FY2012E adjusted book value of Rs120.6. We have an Accumulate rating on the stock with

a target price of Rs115.

July 26, 2010 6

7. Market Outlook | India Research

Gateway Distriparks

Gateway Distriparks Limited (GDL) is scheduled to announce its results today. We expect

GDL to post strong growth of 14.7% yoy in its top line to Rs143cr for the quarter led by

better volumes from CFS as well as rail segment on account of improving Exim visibility

and low base. OPMs are expected to remain flat with marginal decline of 26bp at 26.5%

as rail business has shown signs of improvement. We expect healthy contribution from

other income on account of unutilised amount from Blackstone deal being invested for a

short duration. Consequently, net profit is estimated to grow by 15.6% yoy to Rs19.2cr. At

the CMP of Rs116, the stock is trading at 9.6x its FY2012E earnings of Rs12.1 per share.

We continue to recommend Buy on the stock with a target price of Rs150.

GlaxoSmithKline Pharmaceuticals-2QCY2010

GlaxoSmithKline Pharmaceuticals (Glaxo) is expected to announce its 2QCY2010 results.

Glaxo is expected to post 15.3% growth on the top-line front to Rs527.5cr (Rs457.4cr). The

company is expected to report flat OPM at 35.8%, with net profit growing 16.9% to

Rs145.3cr (Rs124.4cr). The stock is currently trading at 31.7x CY2010E and 28.0x

CY2011E earnings. We recommend Sell with a target price of Rs1,700.

NTPC

NTPC is expected to announce its results. We expect the company’s top line to grow 9.2%

yoy to Rs13,110cr, aided by 5.0% volume growth. The company's operating profit is

expected to increase by 8.5% yoy to Rs3,445cr. We estimate NTPC's net profit to grow

moderately by 3.9% yoy to Rs2,279cr on account of high depreciation costs. We maintain

Accumulate on the stock with a target price of Rs230.

Union Bank of India

Union Bank of India is scheduled to announce its results. We expect the bank to post

robust growth of 65.7% in NII on a yoy basis to Rs1,329cr and a marginal dip of 4.8% on

a sequential basis. However, the bank’s NIM is expected to decline sequentially by 30bp

during 1QFY2011 on account of interest payment on savings accounts on a daily basis.

The pre-provision profit of the bank is expected to go up by healthy 37.5% on a yoy basis.

Net profit is expected to go up by 22.7% on a yoy basis to Rs542cr. In line with our view

on select PSU banks, where we predicted pressure on asset quality to continue during

1QFY2011, Indian Bank and PNB have actually witnessed asset quality pressure in

1QFY2011. Hence, we will be closely watching Union Bank’s asset quality, though the

bank is relatively less exposed to such risks in our opinion. At the CMP, the stock is trading

at 1.3x FY2012E ABV. We have a Neutral rating on the stock.

United Phosphorus

United Phosphorus is slated to announce its numbers. For the quarter, we expect

consolidated top-line growth of 10% yoy to Rs1801cr. Bottom line is expected to register

growth of 5% yoy to Rs185cr. We maintain our Buy rating on the stock with a target price

of Rs228.

July 26, 2010 7

8. Market Outlook | India Research

Economic and Political News

Indian telecom user base up ~18mn in June 2010

SEZ units cannot avail IT exemption on DTA sale: MOC

Rs2,245cr FDI proposals approved

Corporate News

LSE approves de-admission of Gateway Distripark’s GDR from trading

RPG flagship eyes Rs2,000cr solar project in Rajasthan

SBI raises US $1bn in overseas bonds issue

Wockhardt gets US FDA approval for generic version of ToprolXL

Source: Economic Times, Business Standard, Business Line, Financial Express, Mint

Events for the day

Bharat Forge Results

Dabur India Results

Dena Bank Results

Gateway Distriparks Results

GlaxoSmithKline Pharma Results

KEI Inds Results

NELCO Results

NTPC Results

Sterlite Industries Results

TajGVK Hotels Results

Union Bank Results

United Phos Results

July 26, 2010 8

9. Market Outlook | India Research

Research Team Tel: 022-4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make investment

decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this document are

those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources

believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this document is for

general guidance only. Angel Broking or any of its affiliates/ group companies shall not be in any way responsible for any loss or

damage that may arise to any person from any inadvertent error in the information contained in this report. Angel Broking Limited has

not independently verified all the information contained within this document. Accordingly, we cannot testify, nor make any representation

or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel Broking Limited

endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance, or other

reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or other

advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section).

Address: Acme Plaza, ‘A’ Wing, 3rd Floor, M.V. Road, Opp. Sangam Cinema, Andheri (E), Mumbai - 400 059.

Tel : (022) 3952 4568 / 4040 3800

Angel Broking Ltd: BSE Sebi Regn No : INB 010996539 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / PMS Regn Code: PM/INP000001546

Angel Capital & Debt Market Ltd: INB 231279838 / NSE FNO: INF 231279838 / NSE Member code -12798 Angel Commodities Broking (P) Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM /

CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302

July 26, 2010 9