India Market Outlook and Research Report

•

1 like•96 views

The key Indian stock market indices opened lower taking cues from weak global markets but recovered later in the day. The Sensex and Nifty ended the session up 0.3% each. Several companies are scheduled to announce quarterly results today including Aventis Pharma, Container Corp, Crompton Greaves, HDFC Bank, and Sesa Goa. The report provides expectations for the results and stock price forecasts for some of these companies. It also summarizes recent corporate deals and economic news in India.

Recommended

More Related Content

What's hot

What's hot (15)

Viewers also liked

Viewers also liked (17)

Similar to India Market Outlook and Research Report

Similar to India Market Outlook and Research Report (20)

More from Angel Broking

More from Angel Broking (20)

Recently uploaded

Recently uploaded (20)

India Market Outlook and Research Report

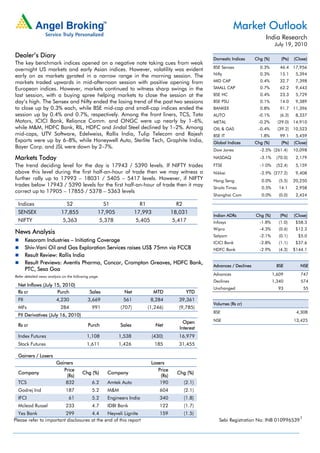

- 1. Market Outlook India Research July 19, 2010 Dealer’s Diary Domestic Indices Chg (%) (Pts) (Close) The key benchmark indices opened on a negative note taking cues from weak BSE Sensex 0.3% 46.4 17,956 overnight US markets and early Asian indices. However, volatility was evident early on as markets gyrated in a narrow range in the morning session. The Nifty 0.3% 15.1 5,394 markets traded upwards in mid-afternoon session with positive opening from MID CAP 0.4% 32.7 7,398 European indices. However, markets continued to witness sharp swings in the SMALL CAP 0.7% 62.2 9,443 last session, with a buying spree helping markets to close the session at the BSE HC 0.4% 23.3 5,729 day’s high. The Sensex and Nifty ended the losing trend of the past two sessions BSE PSU 0.1% 14.0 9,389 to close up by 0.3% each, while BSE mid-cap and small-cap indices ended the BANKEX 0.8% 91.7 11,396 session up by 0.4% and 0.7%, respectively. Among the front liners, TCS, Tata AUTO -0.1% (6.3) 8,337 Motors, ICICI Bank, Reliance Comm. and ONGC were up nearly by 1–6%, METAL -0.2% (29.0) 14,910 while M&M, HDFC Bank, RIL, HDFC and Jindal Steel declined by 1–2%. Among OIL & GAS -0.4% (39.2) 10,523 mid-caps, UTV Software, Edelweiss, Rallis India, Tulip Telecom and Rajesh BSE IT 1.8% 99.1 5,459 Exports were up by 6–8%, while Honeywell Auto, Sterlite Tech, Graphite India, Global Indices Chg (%) (Pts) (Close) Bayer Corp. and JSL were down by 2–7%. Dow Jones -2.5% (261.4) 10,098 Markets Today NASDAQ -3.1% (70.0) 2,179 The trend deciding level for the day is 17943 / 5390 levels. If NIFTY trades FTSE -1.0% (52.4) 5,159 above this level during the first half-an-hour of trade then we may witness a Nikkei -2.9% (277.2) 9,408 further rally up to 17993 – 18031 / 5405 – 5417 levels. However, if NIFTY Hang Seng 0.0% (5.5) 20,250 trades below 17943 / 5390 levels for the first half-an-hour of trade then it may Straits Times 0.5% 14.1 2,958 correct up to 17905 – 17855 / 5378 – 5363 levels Shanghai Com 0.0% (0.0) 2,424 Indices S2 S1 R1 R2 SENSEX 17,855 17,905 17,993 18,031 Indian ADRs Chg (%) (Pts) (Close) NIFTY 5,363 5,378 5,405 5,417 Infosys -1.8% (1.0) $58.3 Wipro -4.3% (0.6) $12.3 News Analysis Satyam -2.1% (0.1) $5.0 Kesoram Industries – Initiating Coverage ICICI Bank -2.8% (1.1) $37.6 Shiv-Vani Oil and Gas Exploration Services raises US$ 75mn via FCCB HDFC Bank -2.9% (4.3) $144.1 Result Review: Rallis India Result Previews: Aventis Pharma, Concor, Crompton Greaves, HDFC Bank, Advances / Declines BSE NSE PTC, Sesa Goa Refer detailed news analysis on the following page. Advances 1,609 747 Declines 1,340 574 Net Inflows (July 15, 2010) Unchanged 93 55 Rs cr Purch Sales Net MTD YTD FII 4,230 3,669 561 8,284 39,361 Volumes (Rs cr) MFs 284 991 (707) (1,246) (9,785) BSE 4,308 FII Derivatives (July 16, 2010) Open NSE 13,425 Rs cr Purch Sales Net Interest Index Futures 1,108 1,538 (430) 16,979 Stock Futures 1,611 1,426 185 31,455 Gainers / Losers Gainers Losers Price Price Company Chg (%) Company Chg (%) (Rs) (Rs) TCS 832 6.2 Amtek Auto 190 (2.1) Godrej Ind 187 5.2 M&M 604 (2.1) IFCI 61 5.2 Engineers India 340 (1.8) Mcleod Russel 233 4.7 IDBI Bank 122 (1.7) Yes Bank 299 4.4 Neyveli Lignite 159 (1.5) Please refer to important disclosures at the end of this report Sebi Registration No: INB 0109965391

- 2. Market Outlook | India Research Kesoram Industries – Initiating Coverage Kesoram Industries (Kesoram) is a diversified player with presence in cement and tyre manufacturing. The company has a total cement capacity of 7.3mtpa at two locations, viz. Sedam (5.7mtpa) in Karnataka and Karimnagar (1.6mtpa) in Andhra Pradesh. In tyres, the company currently has a total installed capacity of 823tpd, which is expected to increase to 988tpd in FY2011E. The company’s cement and tyre businesses are currently trading at attractive valuations coupled with being at a substantial discount to their peers and replacement costs. The cement business is valued at EV/tonne of US $65, which is at a considerable discount to the replacement costs of US$80/tonne. This gives an implied enterprise valuation of Rs1.4cr/tpd to the tyre business, which is at 35–63% discount to the peers such as Apollo Tyres (Rs3.8cr/tpd) and Ceat (Rs2.3cr/tpd). We Initiate Coverage on the stock with a Buy recommendation and an SOTP Target Price of Rs437, implying an upside of 46% from current levels. Shiv-Vani Oil and Gas Exploration Services raises US $75mn via FCCB Shiv Vani Oil & Gas Exploration Services (SOGES) has raised US $75mn through an FCCB issue. The FCCB has a maturity period exceeding 5 years, i.e. August, 17, 2015, and has a coupon-rate of 5% p.a. The conversion price of the FCCB is fixed at a price of Rs515.6/share, around 9.3% higher than the current stock price. The FCCB issues follow the placement made to Franklin Templeton in March this year. The funds raised will be used for international expansion, in R&D and for working capital needs. SOGES is trying to develop capabilities in specialised services, which companies like Schlumberger Ltd. possess. The recent news reports have indicated that SOGES is likely to buy a US-based company to get the required technology to further consolidate its presence in the oil and gas exploration services businesses and the ticket size for the same could be around US $50mn. SOGES lacks expertise in the offshore oil and gas services and is an onshore service provider. Thus, an acquisition to get the offshore technological know-how would strength the business model and will open up new growth avenues for the company. FCCB could result in dilution of 14.8% of the current equity base. The issuance is likely to adversely impact the EPS by around Rs2.7/share; however, the same is likely to be offset via the increase in revenue and profitability via the overseas acquisition. However, ascertaining the impact of the same is not possible at the current juncture as we await more information on the likely overseas acquisition and its exact impact on the company's financials. Awaiting more clarity on the impending overseas acquisition, we keep the stock under review. July 19, 2010 2

- 3. Market Outlook | India Research Result Reviews Rallis India Rallis India declared its 1QFY2011 results, with revenue growth of 22% to Rs203cr, which was ahead of our estimate of Rs193cr. However, EBITDA margins at 11.6% were below our estimates of 13%, hence overall profit came in at lower than the estimate. Total reported PAT for the quarter came in at Rs14.8cr against Rs9cr (1QFY2010), growth of 57.5% yoy. We currently have a Neutral rating on the stock, which would be revised post the management meet. Result Previews Aventis Pharma Aventis Pharma is slated to announce its 2QCY2010 results. Net sales are expected to increase by 10.3% to Rs275.7cr (Rs249.9cr) with OPM estimated to contract to 18.3% (21.2%). As a result, net profit is expected to remain flat at Rs48.2cr (Rs47.1cr) on the back of lower OPM. The stock is currently trading at 24.8x CY2010E and 21.7x CY2011E earnings. We recommend Sell on the stock with a target price of Rs1,658. Container Corporation of India Concor is scheduled to announce its 1QFY2011 results today. The rail container operator is expected to report top-line growth of 7.7% yoy to Rs977cr, on account of low base and improvement in container volumes in the Exim segment. We expect Concor’s OPM to decline by 2,731bp yoy to 25.5%, driven by the continued trend of higher empties and inability to pass on rail freight expenses. Consequently, we expect net profit to decline marginally by 1.9% to Rs197.0cr. At the CMP, the stock is trading at 19.4x its FY2012E EPS of Rs72.6. We maintain our Reduce rating on the stock with a target price of Rs1,194. Crompton Greaves Crompton Greaves is scheduled to announce its 1QFY2011 results. Net sales are expected to increase by 10% yoy to Rs2,416cr (Rs2,198cr) with OPM estimated to expand to 12.6% (11.2%). Net profit is expected to increase by 20.6% yoy to Rs193cr (Rs160cr) on the back of improved operating margin. The stock is currently trading at 19.8x FY2011E and 17.63x FY2012E earnings. We maintain a Buy view on the stock with a target price of Rs307. HDFC Bank HDFC Bank is scheduled to announce its 1QFY2011 results. We expect the bank to report healthy NII growth of 26% yoy. However, NIMs of the bank are expected to decline sequentially by 25bp during 1QFY2011 on account of interest payment on savings accounts on a daily basis. The operating profit of the bank is expected to register 5% yoy growth. Net profit is expected to increase by 33% on a yoy basis to Rs806cr. At the CMP, the stock is trading at valuations of 3.3x FY2012E ABV of Rs629.6. We have an Accumulate rating on the stock, valuing it at 3.5x FY2012E ABV (at the higher end of its five-year range) to arrive at a 12-month target price of Rs2,204. July 19, 2010 3

- 4. Market Outlook | India Research PTC PTC is slated to announce its 1QFY2011 results. We expect the company to record a 44.9% yoy decline in its standalone top line to Rs1,307cr. We expect the company to trade 3,350MU of power during the quarter, resulting in a decrease of 20.3% yoy. We have assumed an average realisation of Rs3.9/unit. We expect the company's net profit to decline by 48.1% yoy to Rs17.3cr. We maintain a Buy rating on the stock with a target price of Rs136. Sesa Goa Sesa Goa is slated to announce its 1QFY2011 results today. We expect the company’s top line to grow by 141.7% yoy to Rs2,445cr on account of higher realisations. Consequently, on the operating front, EBITDA margin is expected to expand by 1,521bp yoy to 60.0%. Hence, the bottom line is expected to grow by 183.4% yoy to Rs1,197cr. We maintain a Neutral rating on the stock. July 19, 2010 4

- 5. Market Outlook | India Research Economic and Political News 12.3mn new GSM subscribers added in June: COAI Delhi government slashes VAT on diesel from 20.0% to 12.5% IRDA backs FM panel on regulatory tiffs Corporate News Reliance Infra inks pact with NHAI for Rs30bn Delhi-Agra highway Diamond Power secures order worth Rs332cr Tata Steel arm sells 27% stake in Malaysian firm for US $72mn Om Metals Infraprojects bags Rs300cr road order from the Government of Rajasthan Source: Economic Times, Business Standard, Business Line, Financial Express, Mint Events for the day Aventis Pharma Dividend, Results Bayer Crop Results Container Corp Dividend, Results Crompton Greaves Results HDFC Bank Results Jindal Saw Dividend, Results Midday Multi-media Results PTC India Results Sesa Goa Results Whirlpool Results July 19, 2010 5

- 6. Market Outlook | India Research Research Team Tel: 022-4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com DISCLAIMER This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and risks of such an investment. Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this document are those of the analyst, and the company may or may not subscribe to all the views expressed within. Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's fundamentals. The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this document is for general guidance only. Angel Broking or any of its affiliates/ group companies shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance, or other reasons that prevent us from doing so. This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced, redistributed or passed on, directly or indirectly. Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in the past. Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in connection with the use of this information. Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Address: Acme Plaza, ‘A’ Wing, 3rd Floor, M.V. Road, Opp. Sangam Cinema, Andheri (E), Mumbai - 400 059. Tel : (022) 3952 4568 / 4040 3800 Angel Broking Ltd: BSE Sebi Regn No : INB 010996539 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / PMS Regn Code: PM/INP000001546 Angel Capital & Debt Market Ltd: INB 231279838 / NSE FNO: INF 231279838 / NSE Member code -12798 Angel Commodities Broking (P) Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM / CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302 July 19, 2010 6