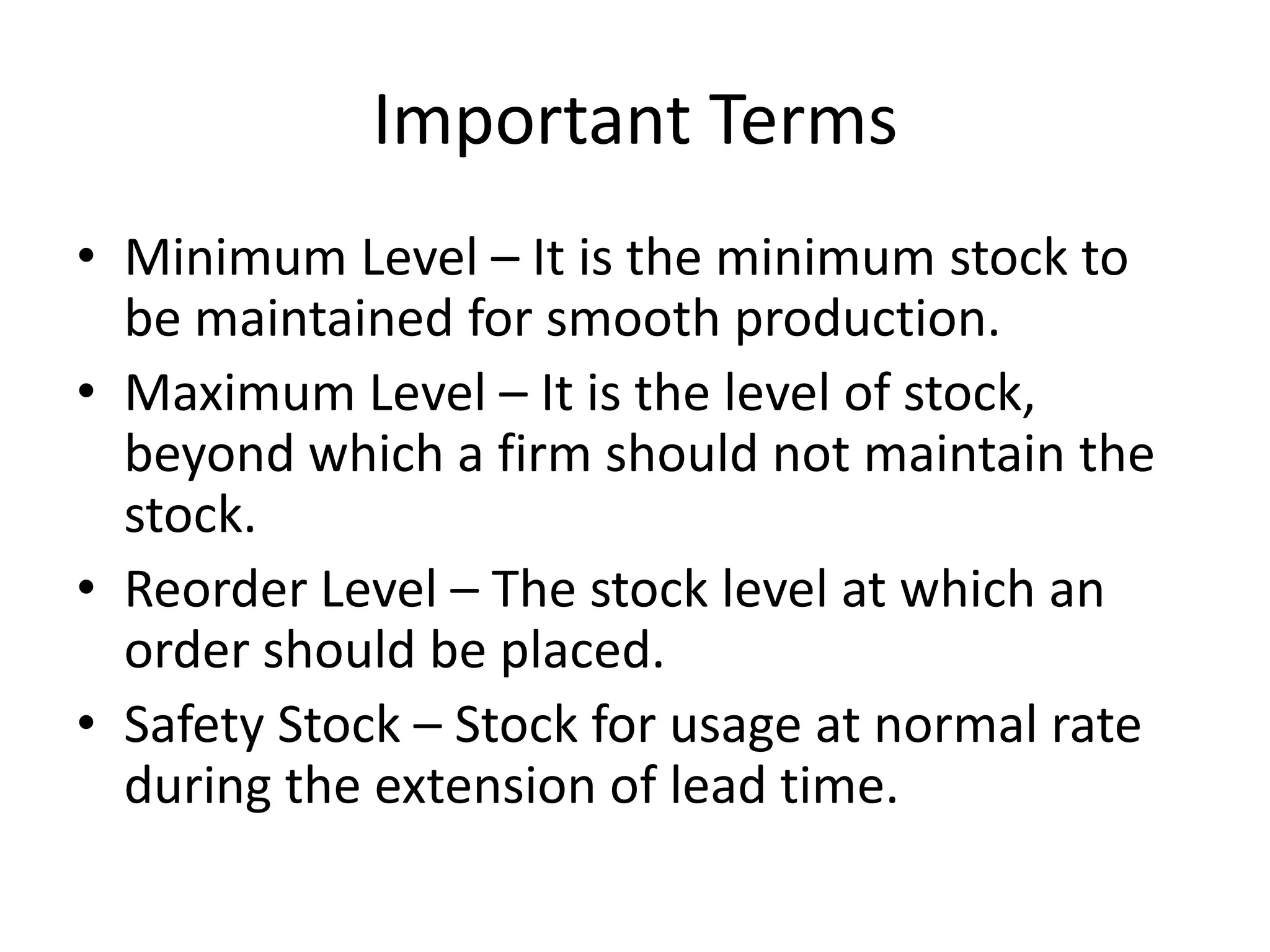

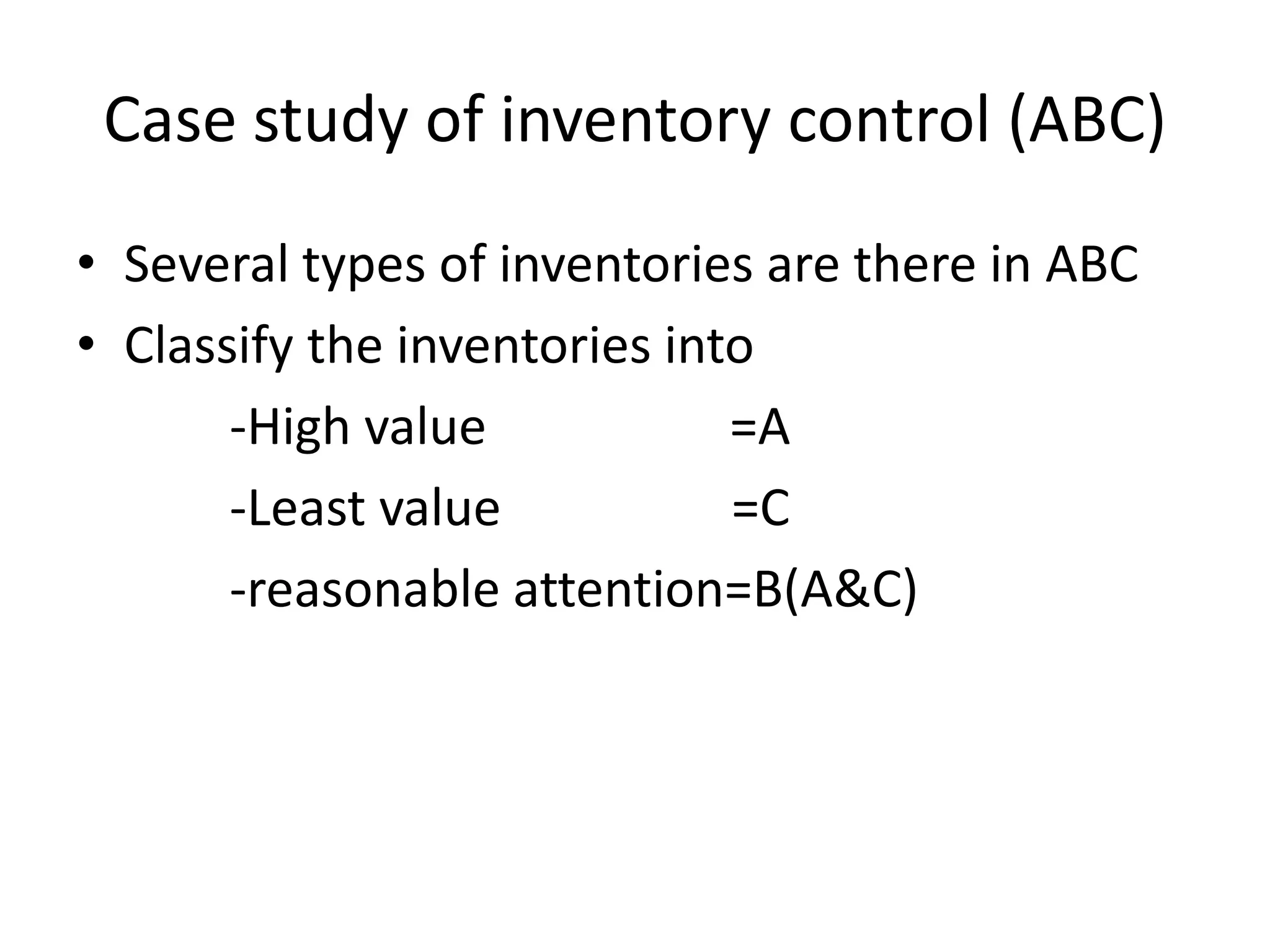

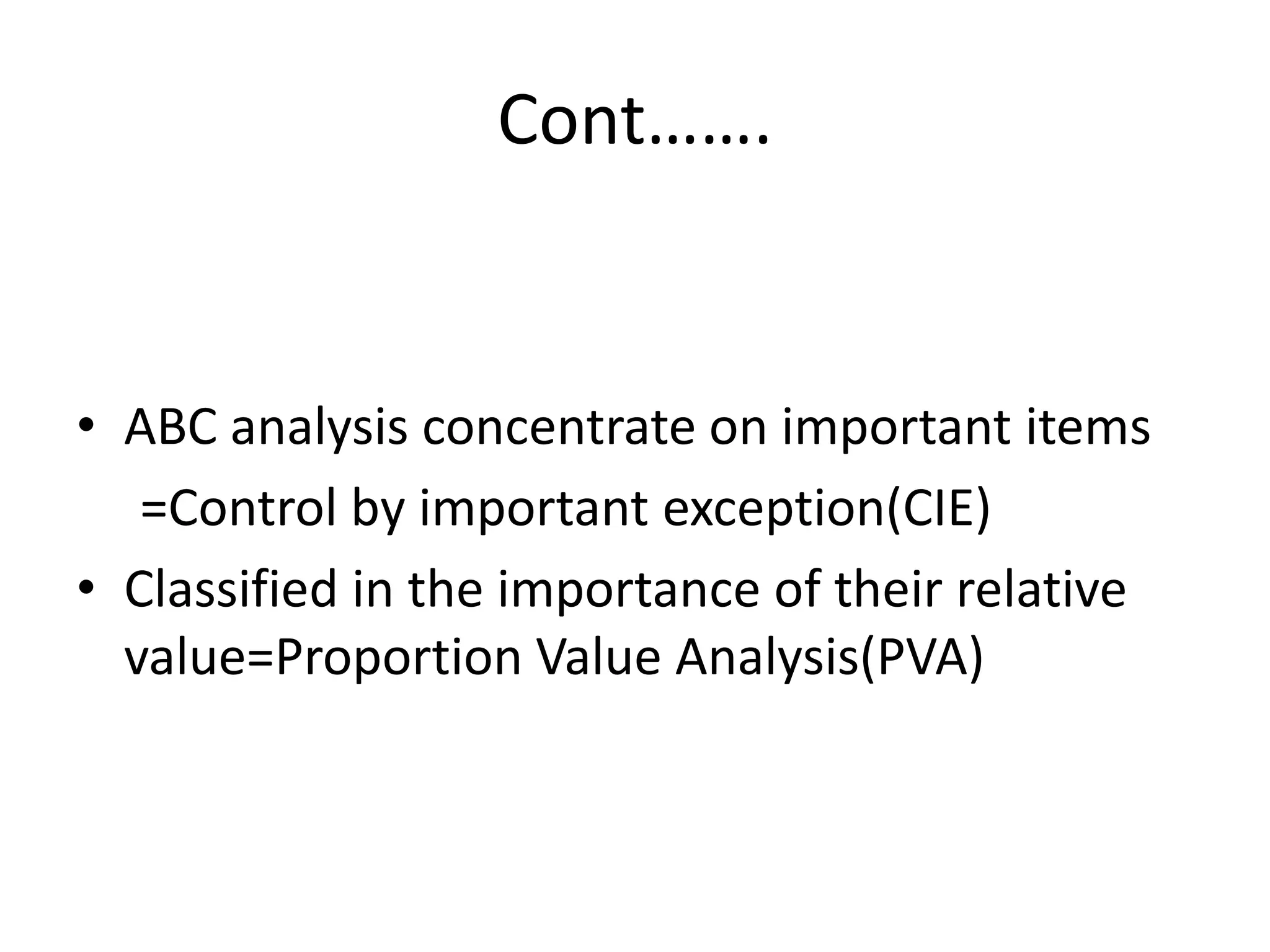

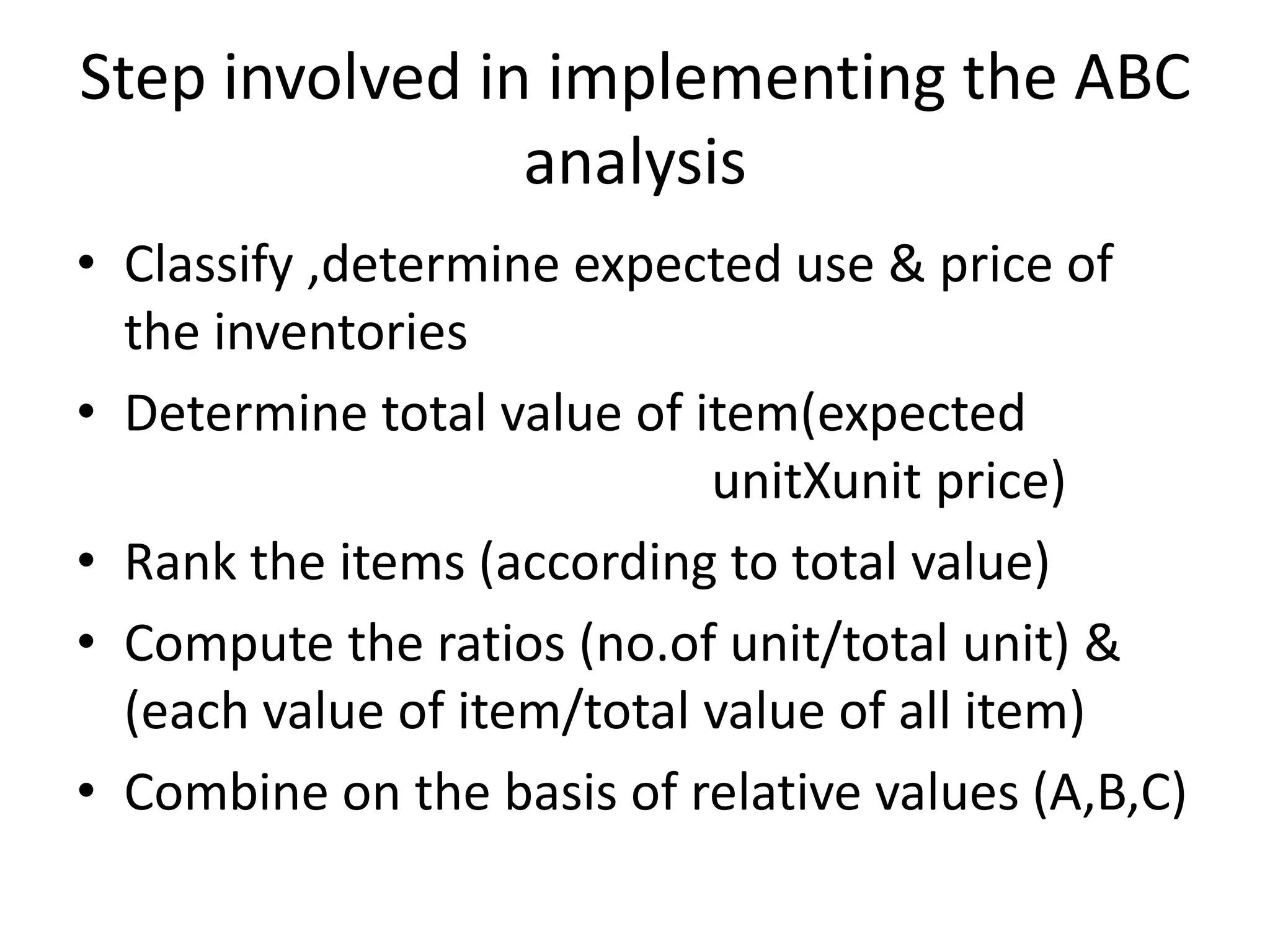

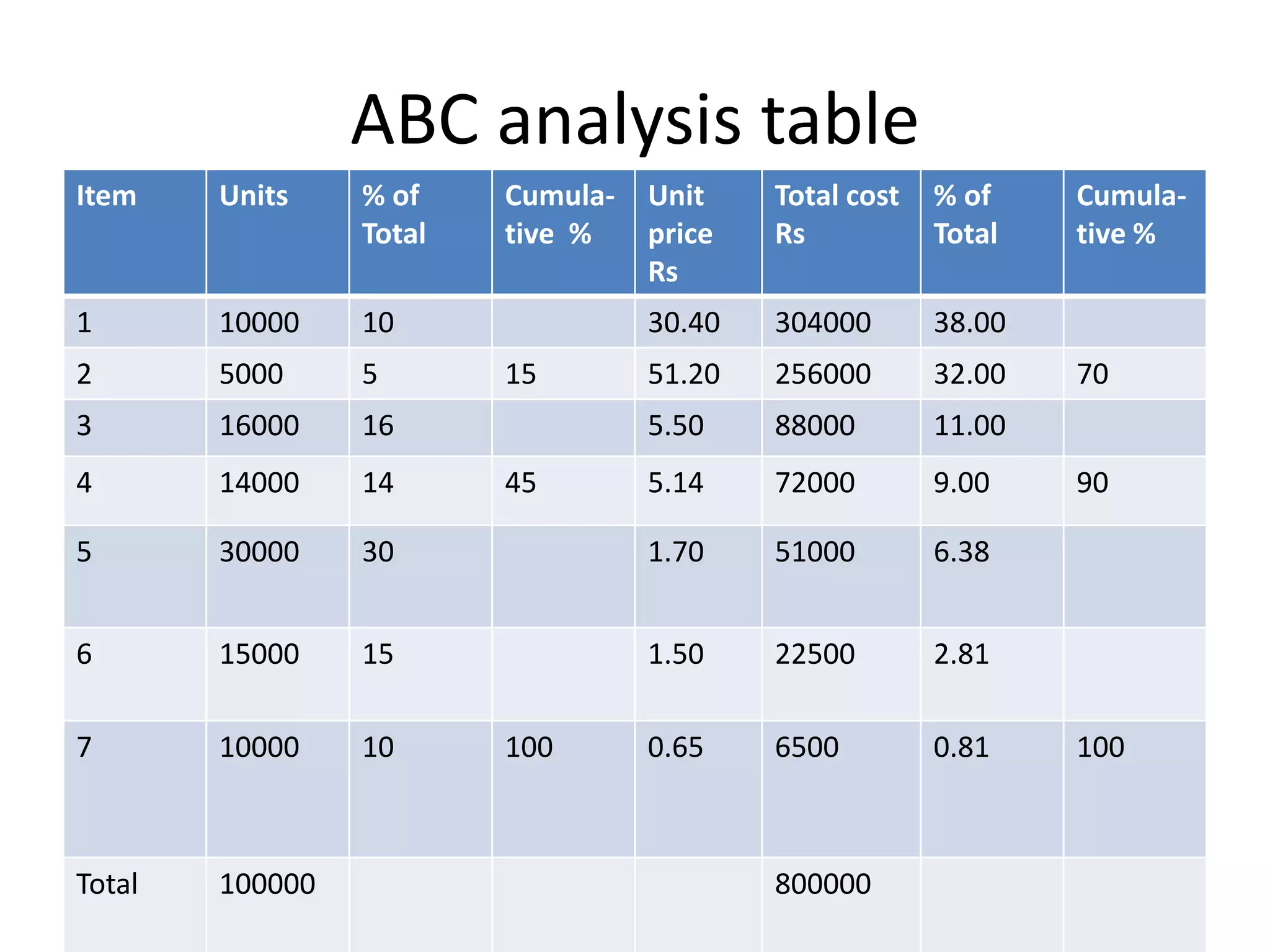

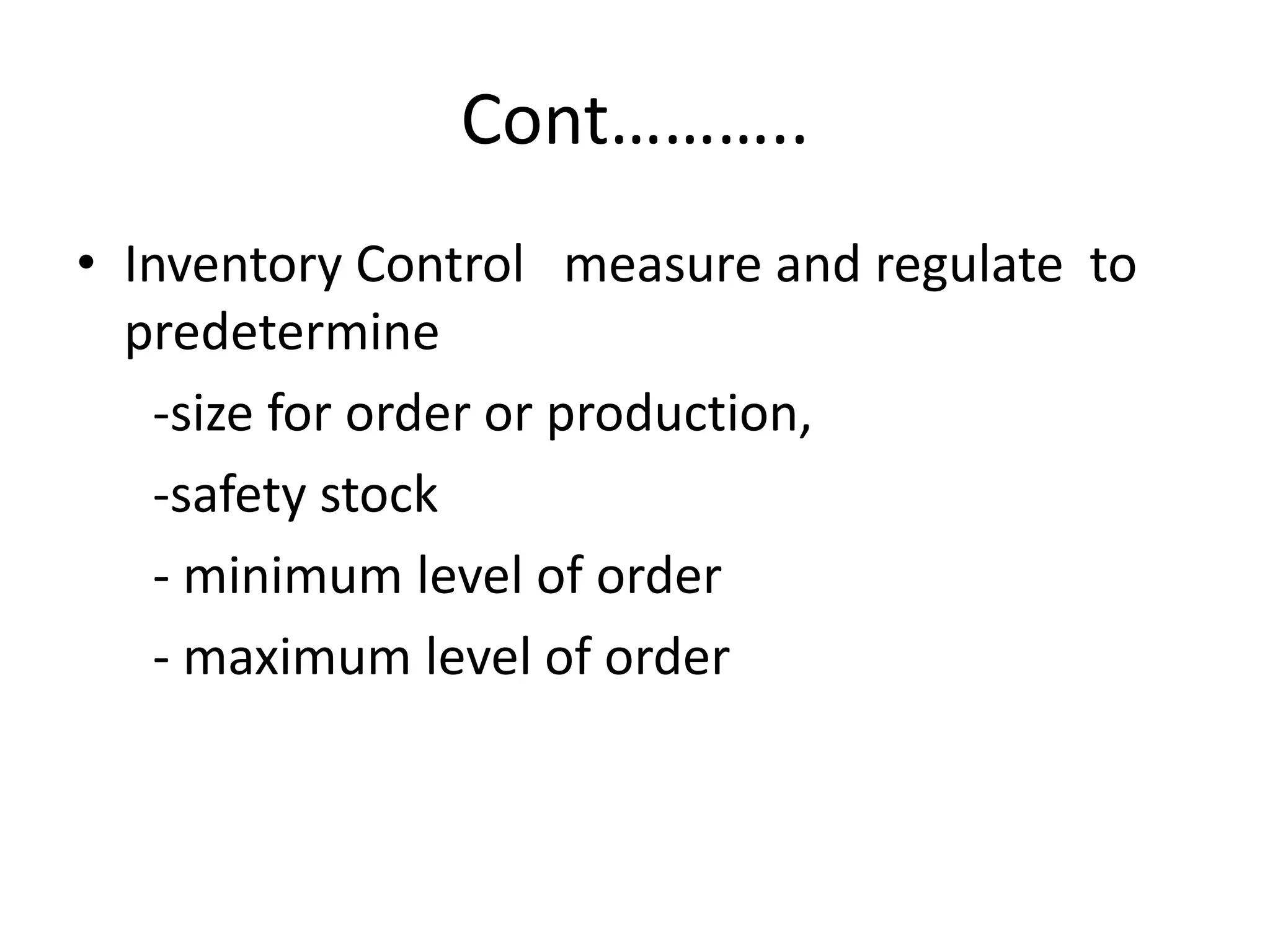

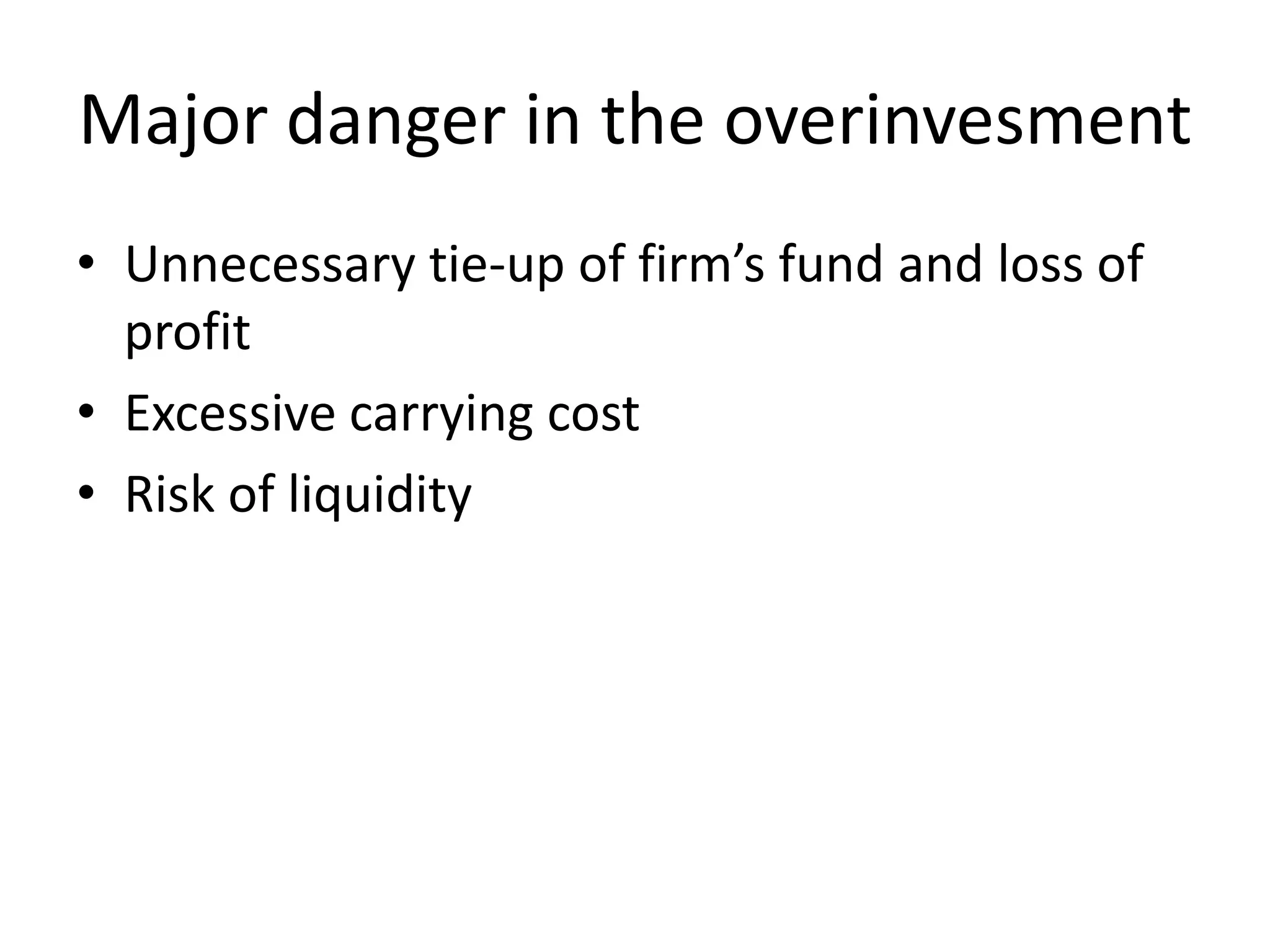

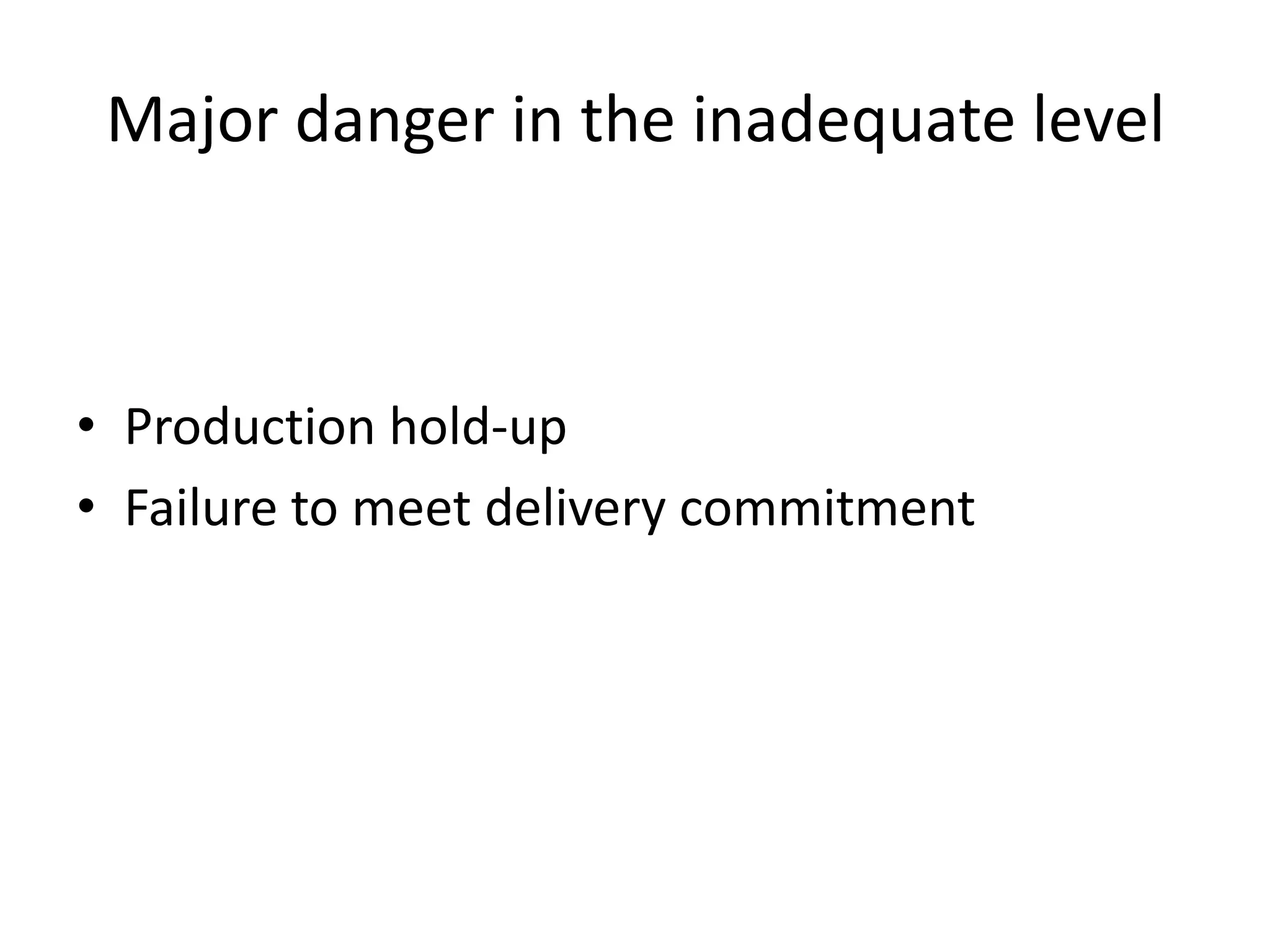

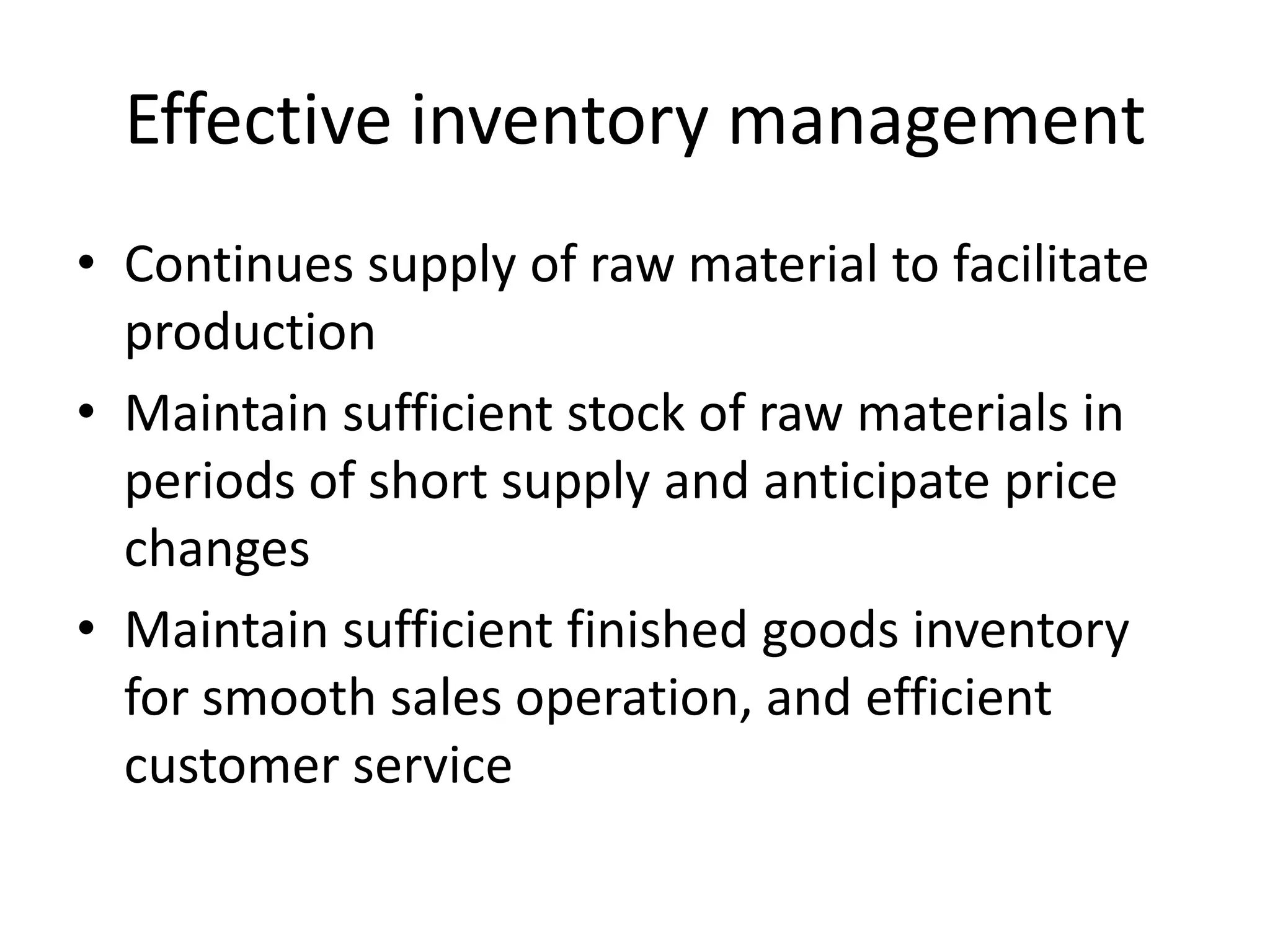

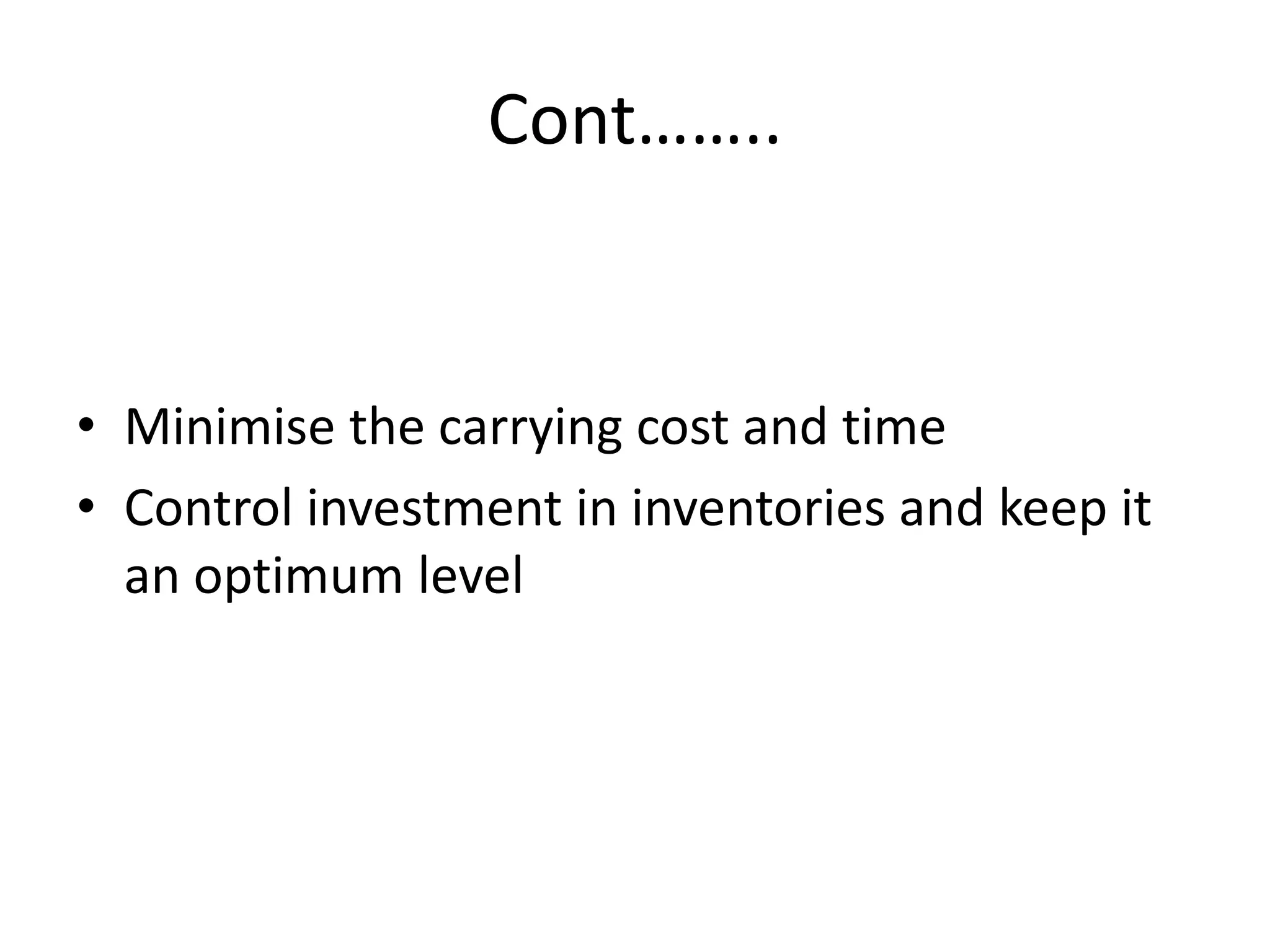

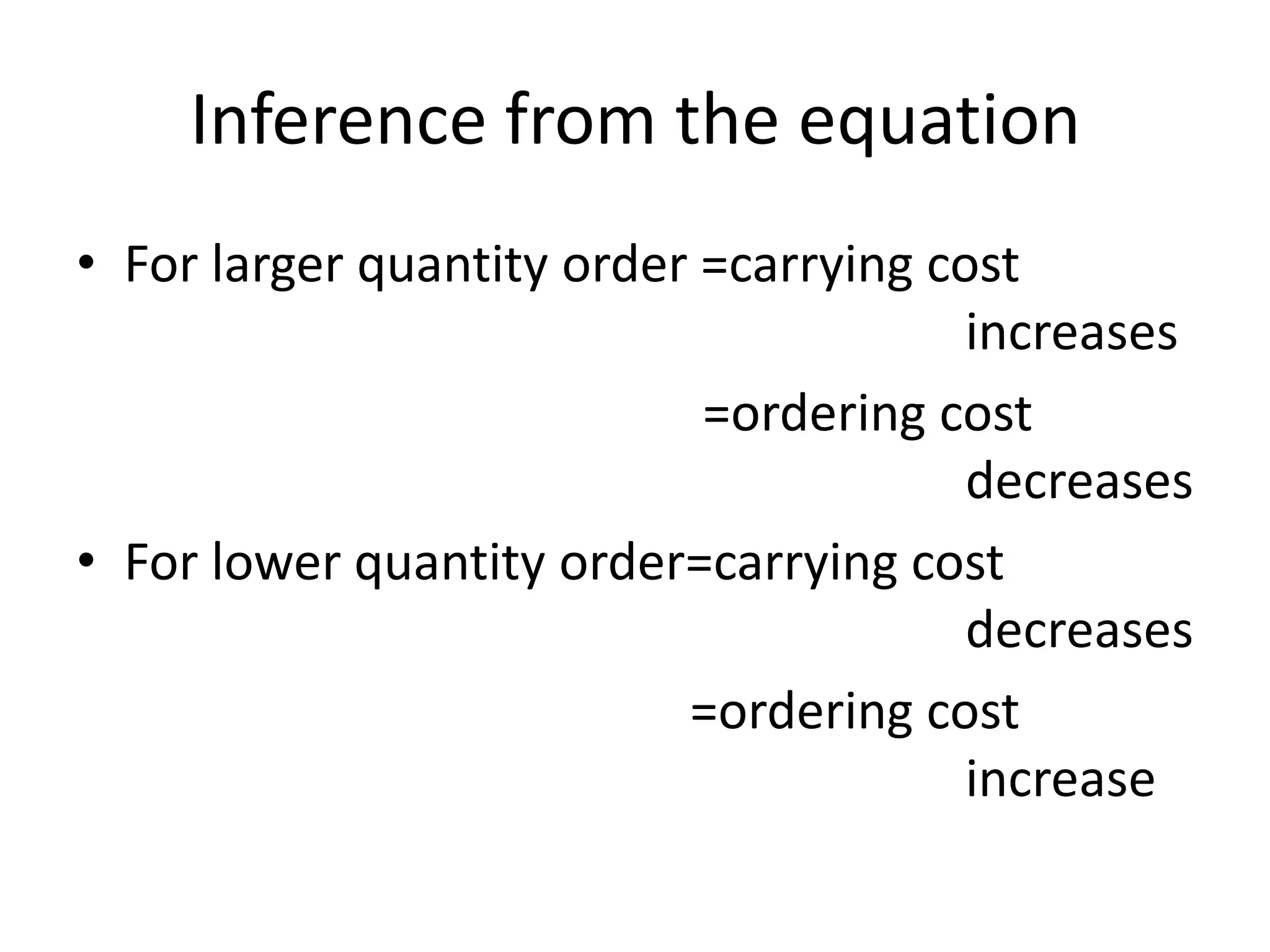

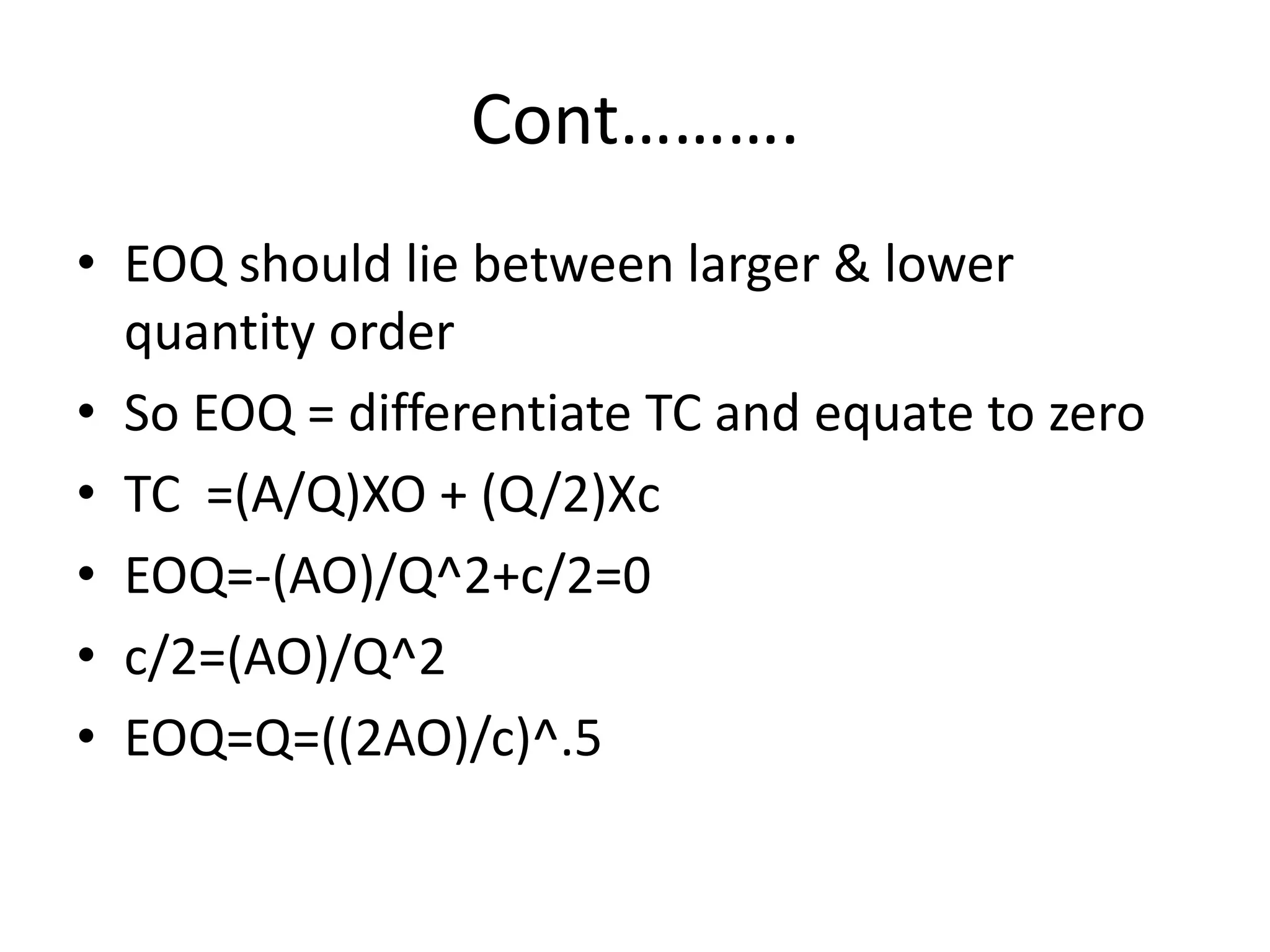

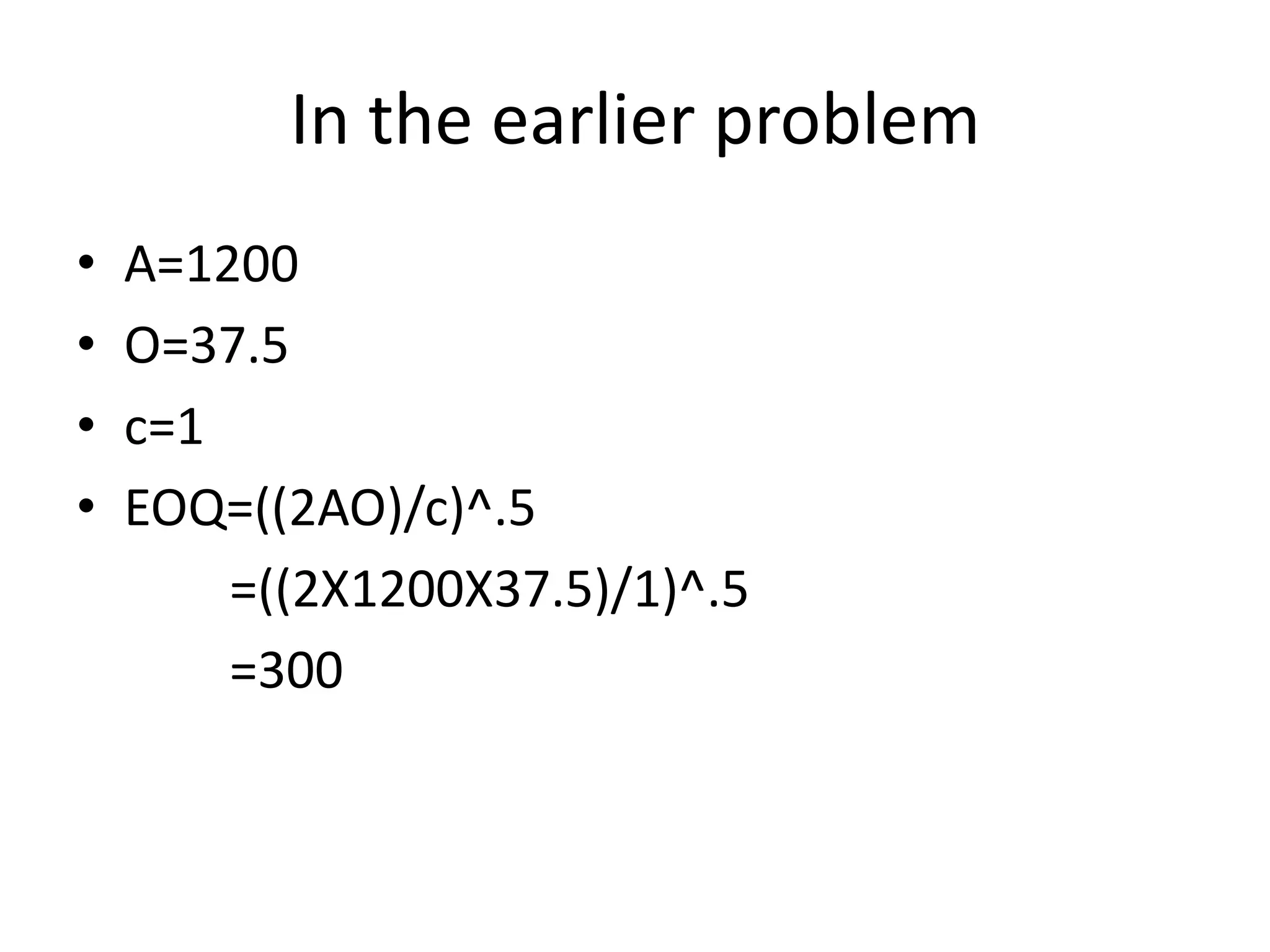

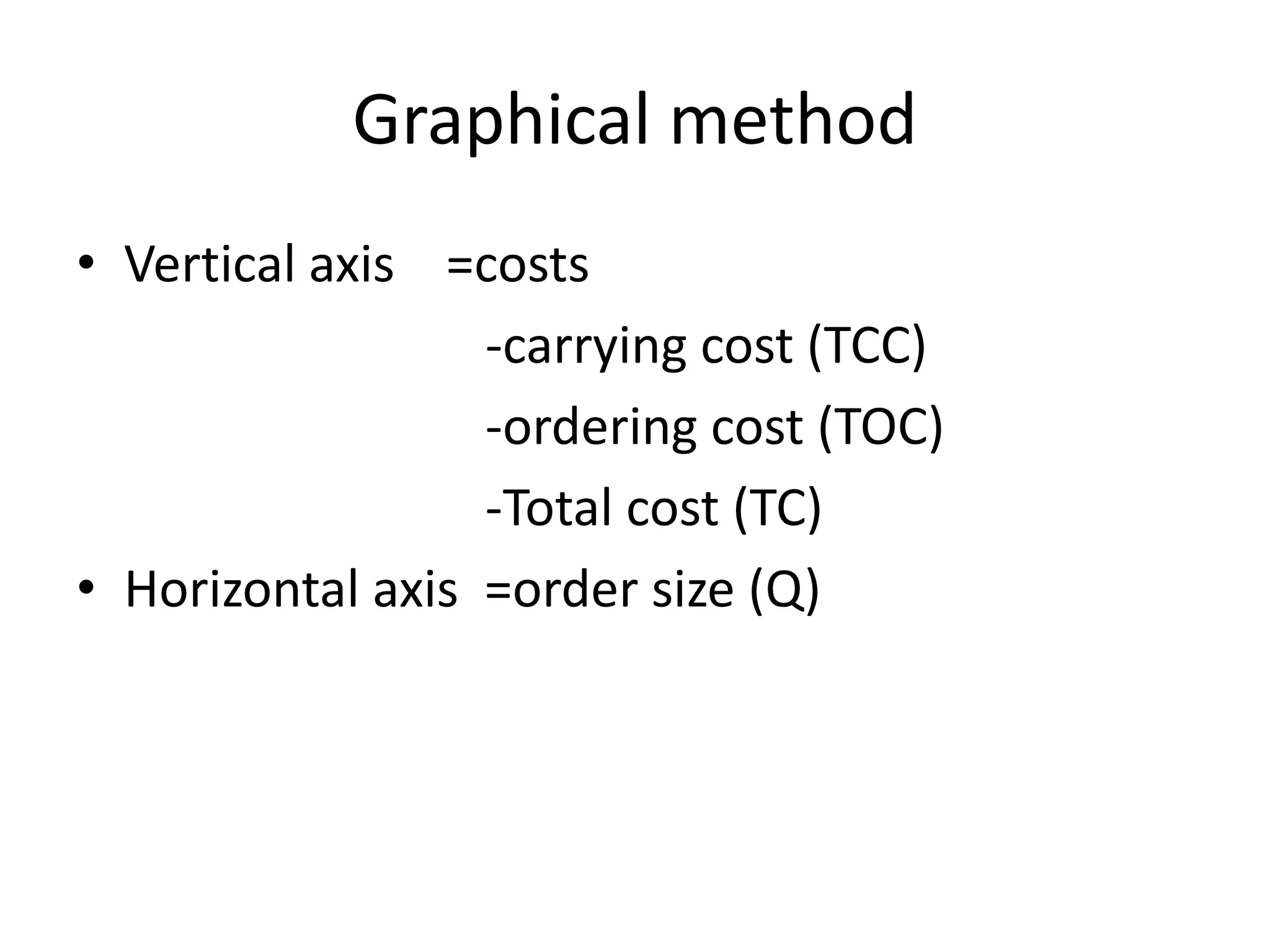

This document discusses inventory management techniques. It begins by explaining that inventory is a significant current asset that requires management to avoid unnecessary investment of funds. It then defines inventory control measures like order size, safety stock, and reorder points. It discusses the different types of inventories and the various reasons companies hold inventory. The objectives and techniques of effective inventory management are outlined, including determining economic order quantity and reorder points. ABC analysis is presented as a case study, classifying inventory into categories based on value to prioritize control efforts.

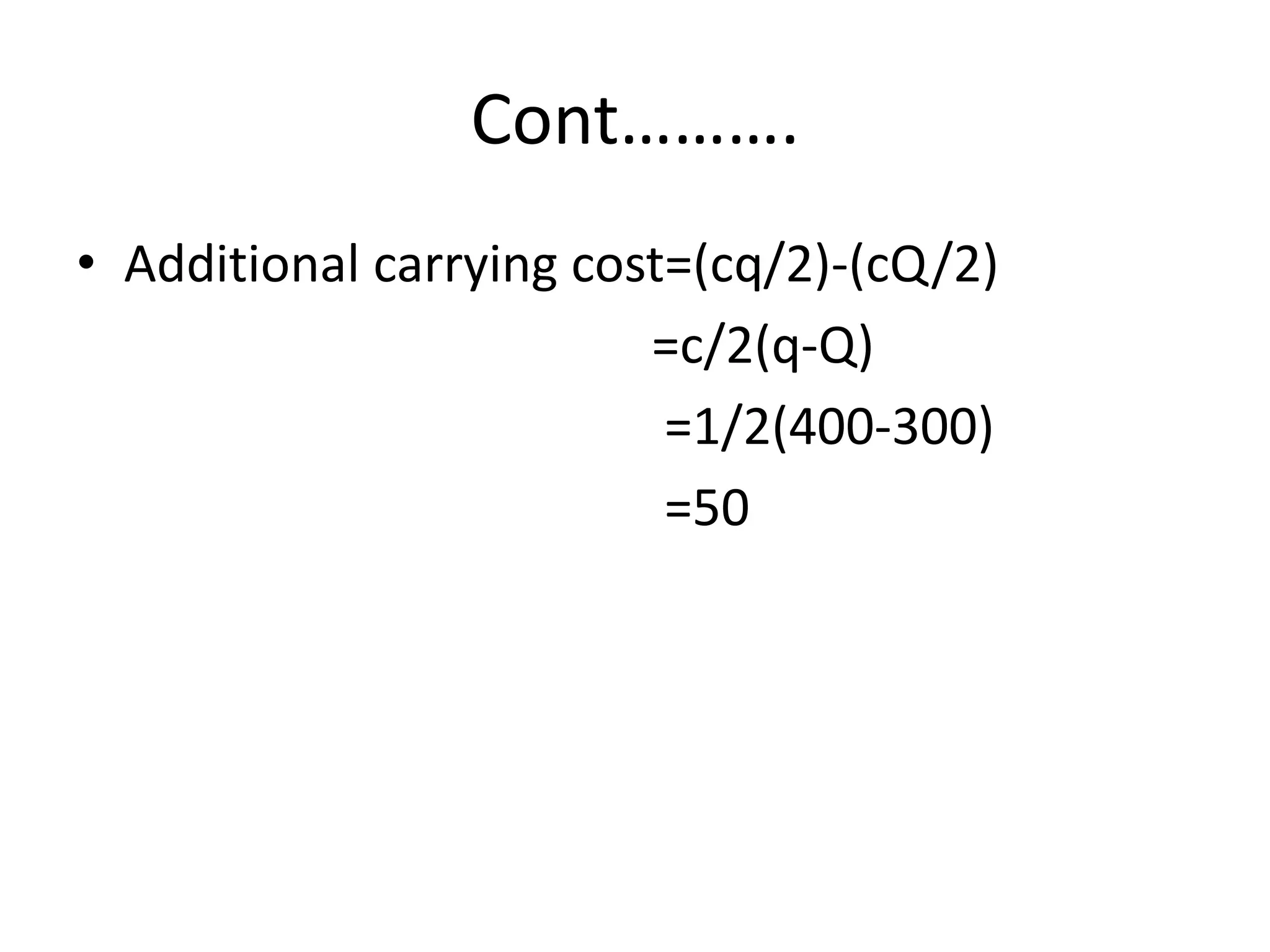

![Exampled=discount rate (.005)Discount on savings=dXPXA=(.005X50X1200) =300Savings on the ordering cost=(OA/Q)-(OA/q)Here Q=EOQ & q=discount quantity(400)=O[A/Q-A/q]=37.5[1200/300-1200/400] =37.5](https://image.slidesharecdn.com/fmppt-110221041250-phpapp02/75/inventory-control-ABC-analysis-ppt-34-2048.jpg)

![Cont……Net return=[dPA+ savings on - additional discount] carrying cost =(300+37.5)-50 =287.5Here net return is +ve= firm should order 400 unit](https://image.slidesharecdn.com/fmppt-110221041250-phpapp02/75/inventory-control-ABC-analysis-ppt-36-2048.jpg)