Downloaded 2,013 times

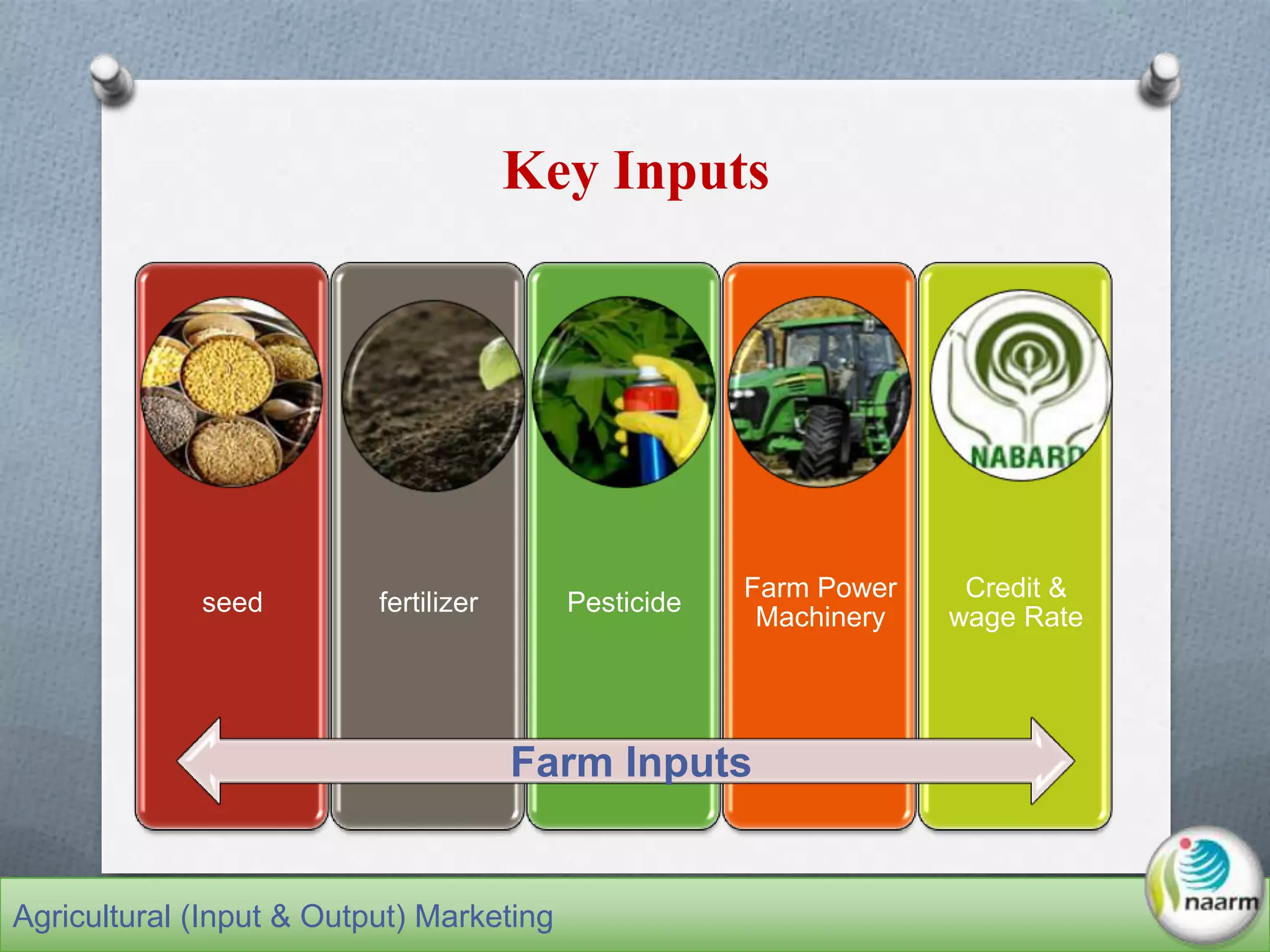

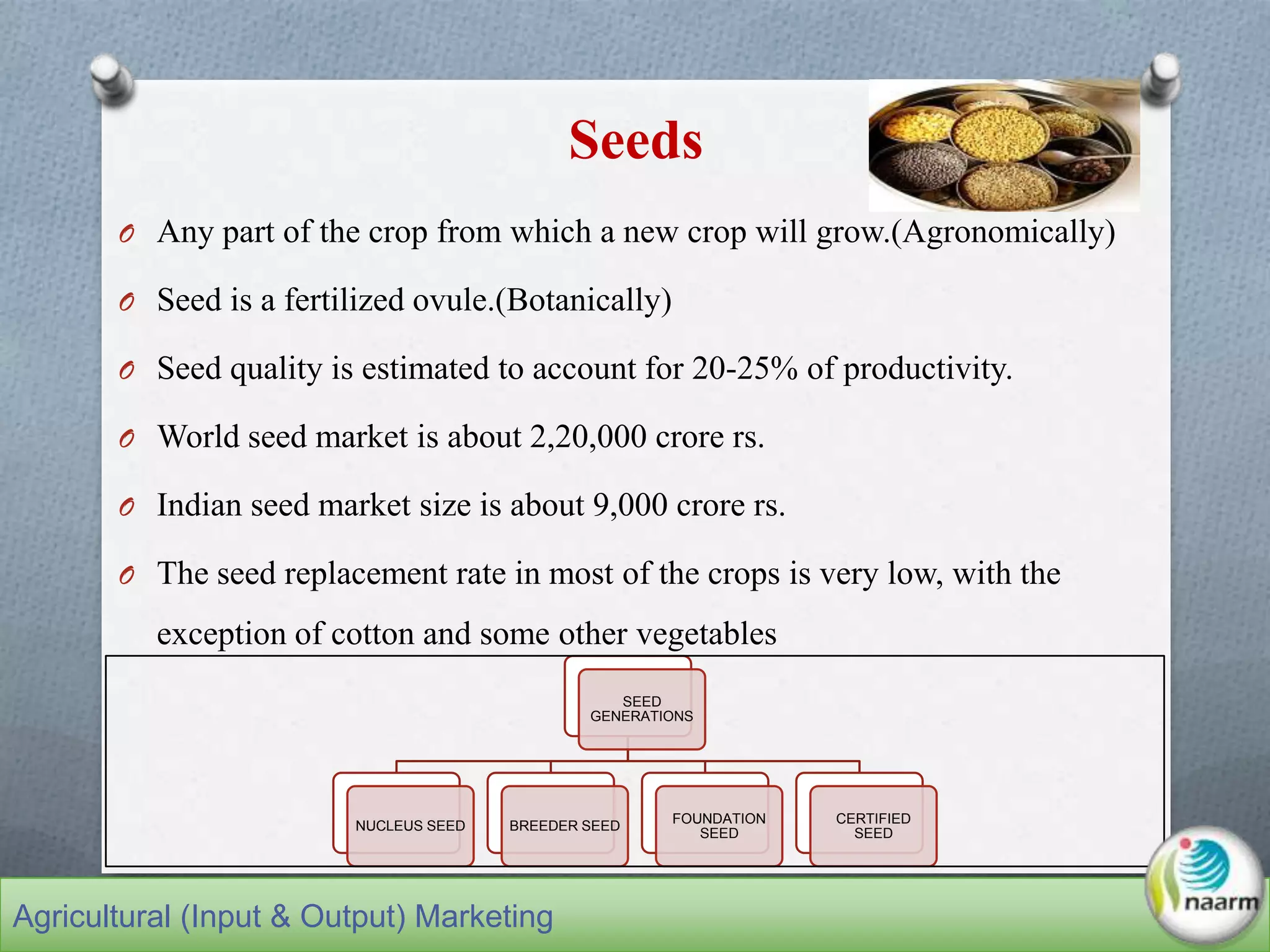

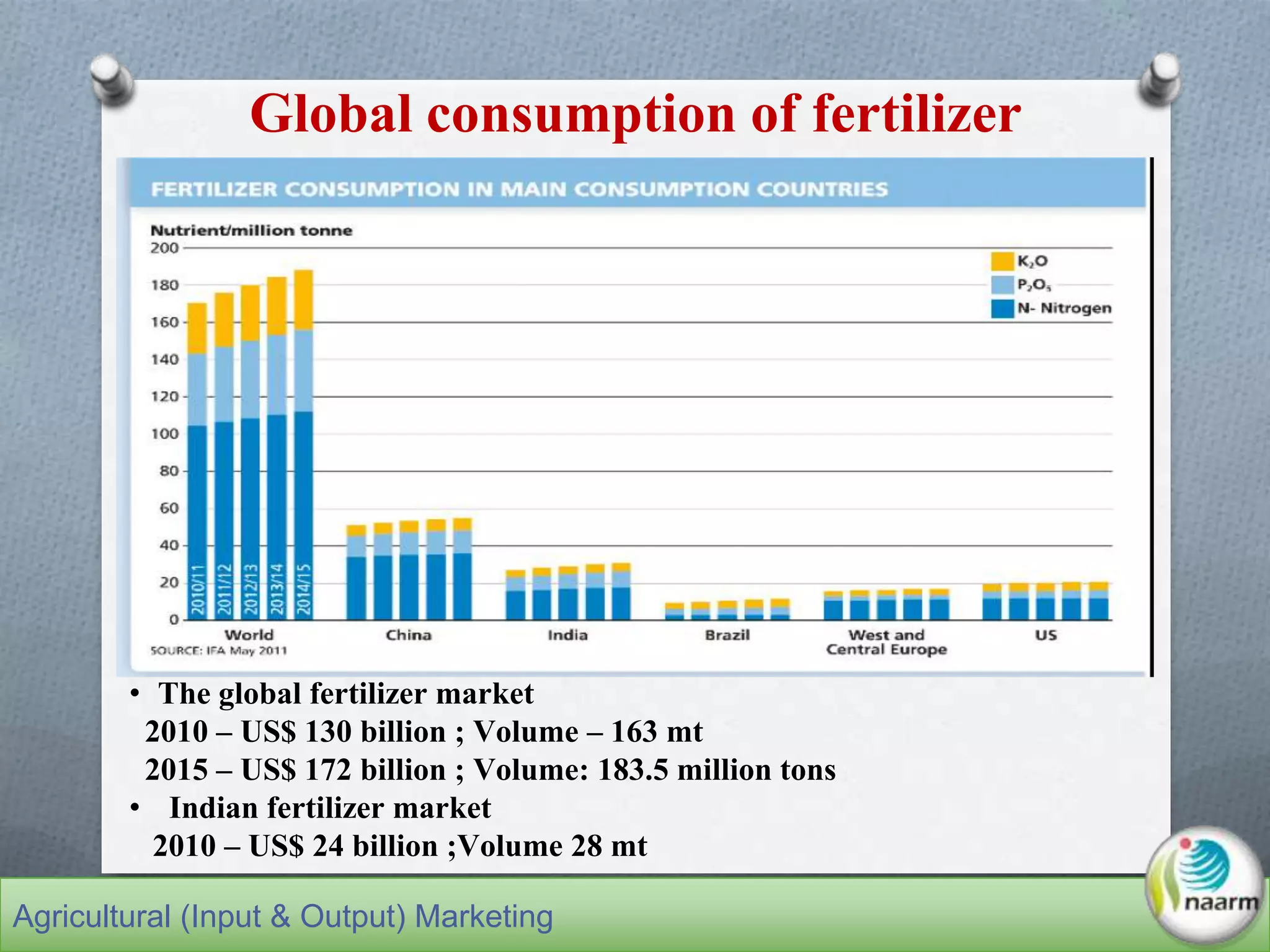

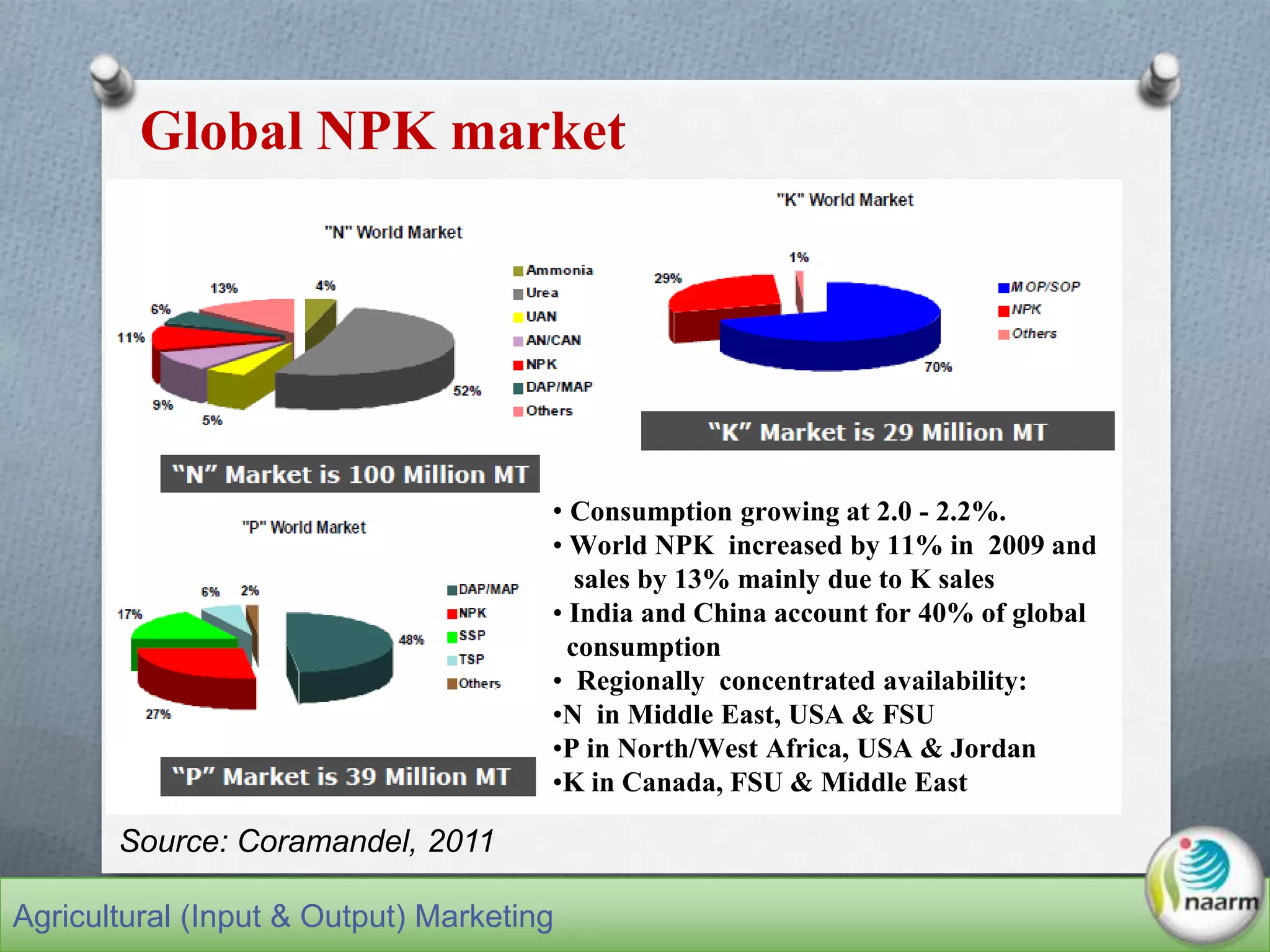

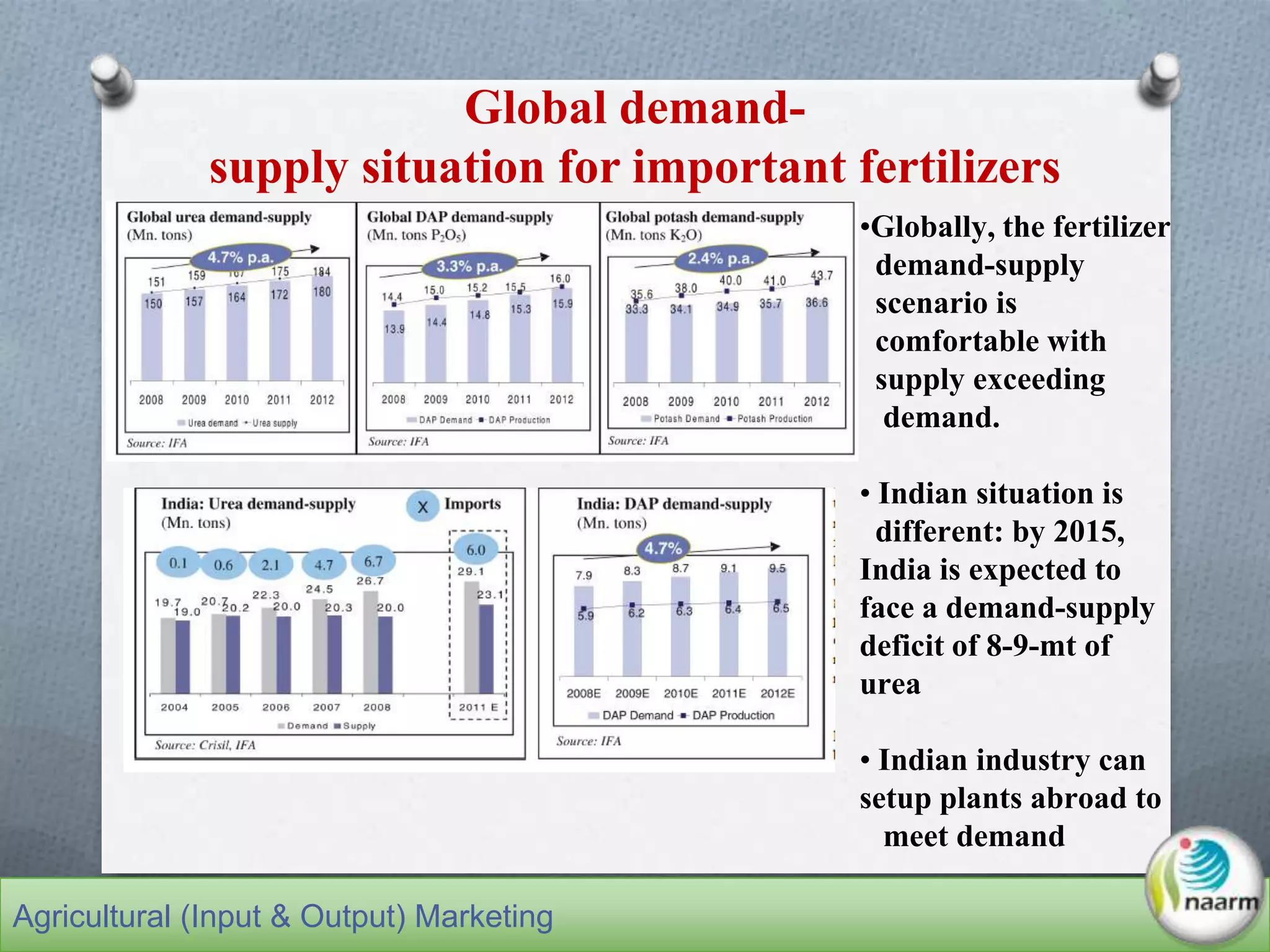

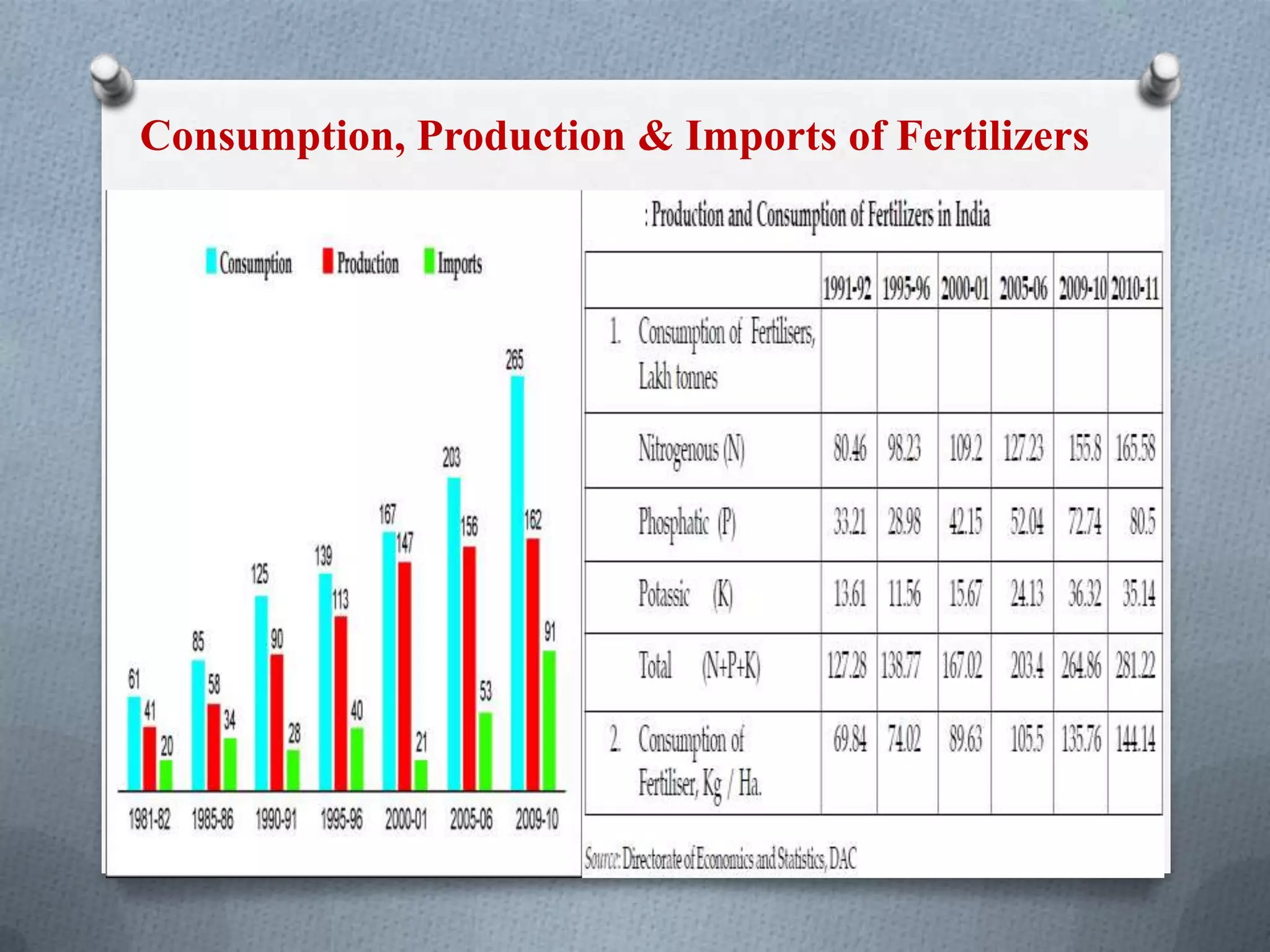

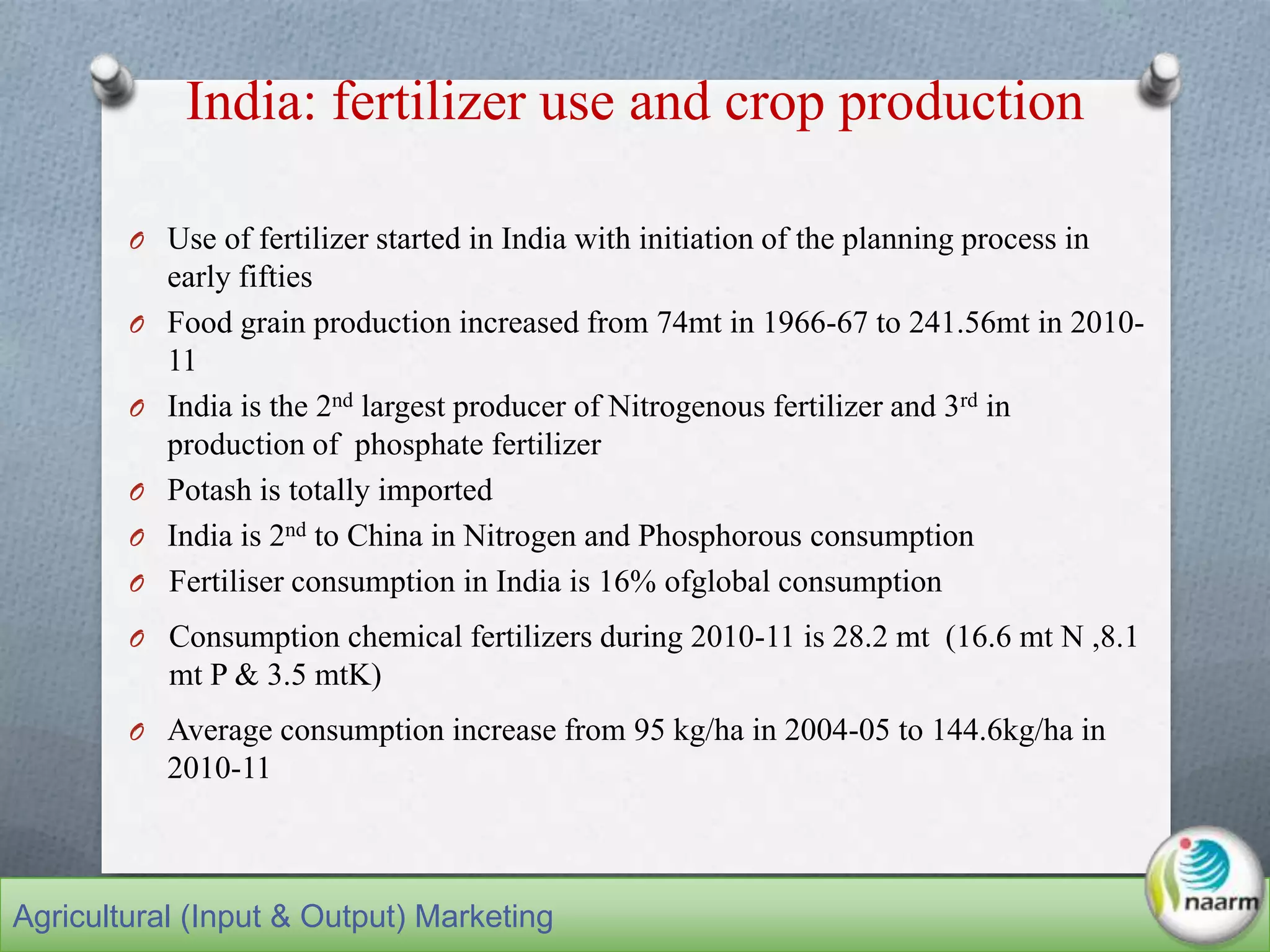

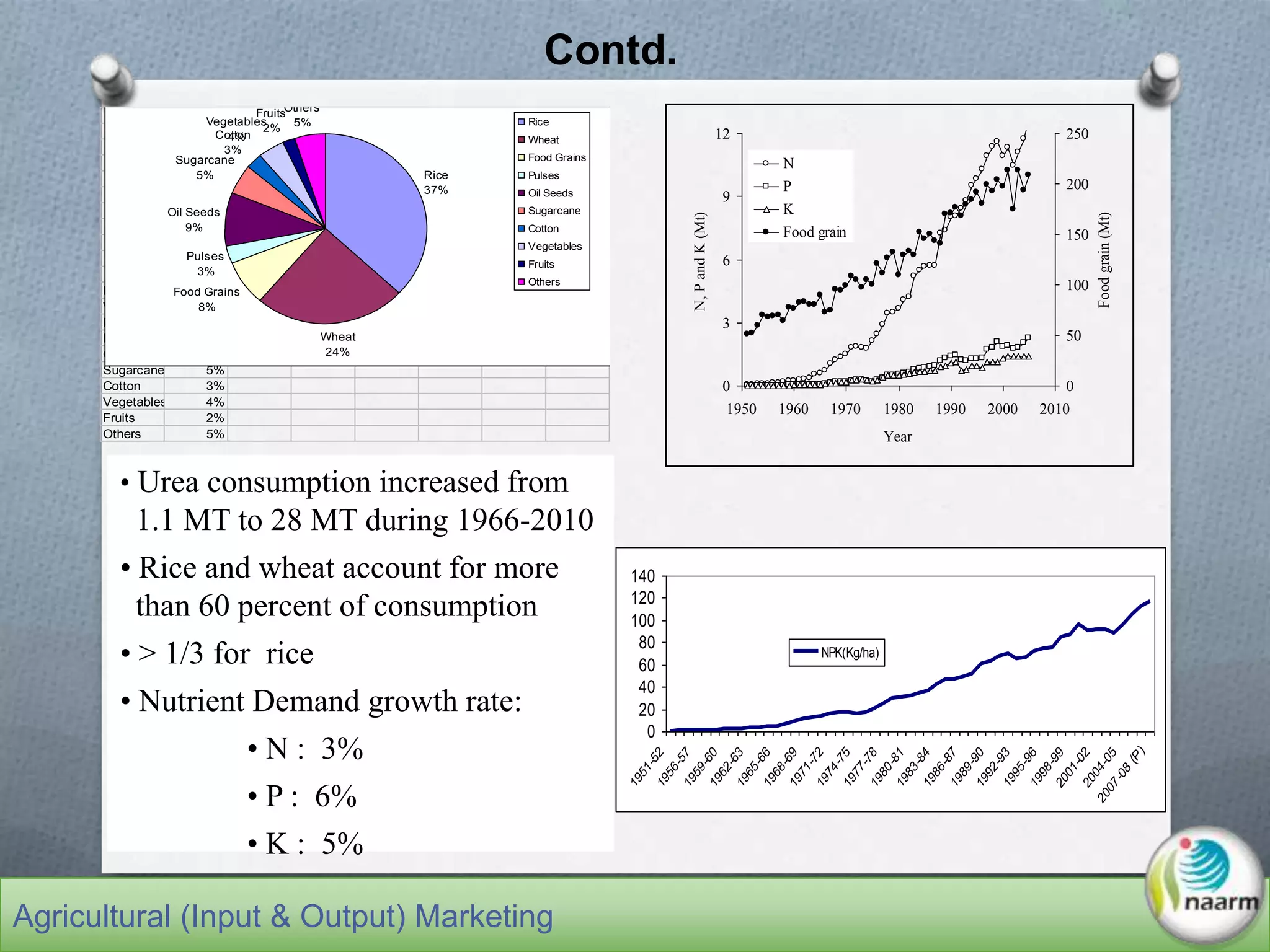

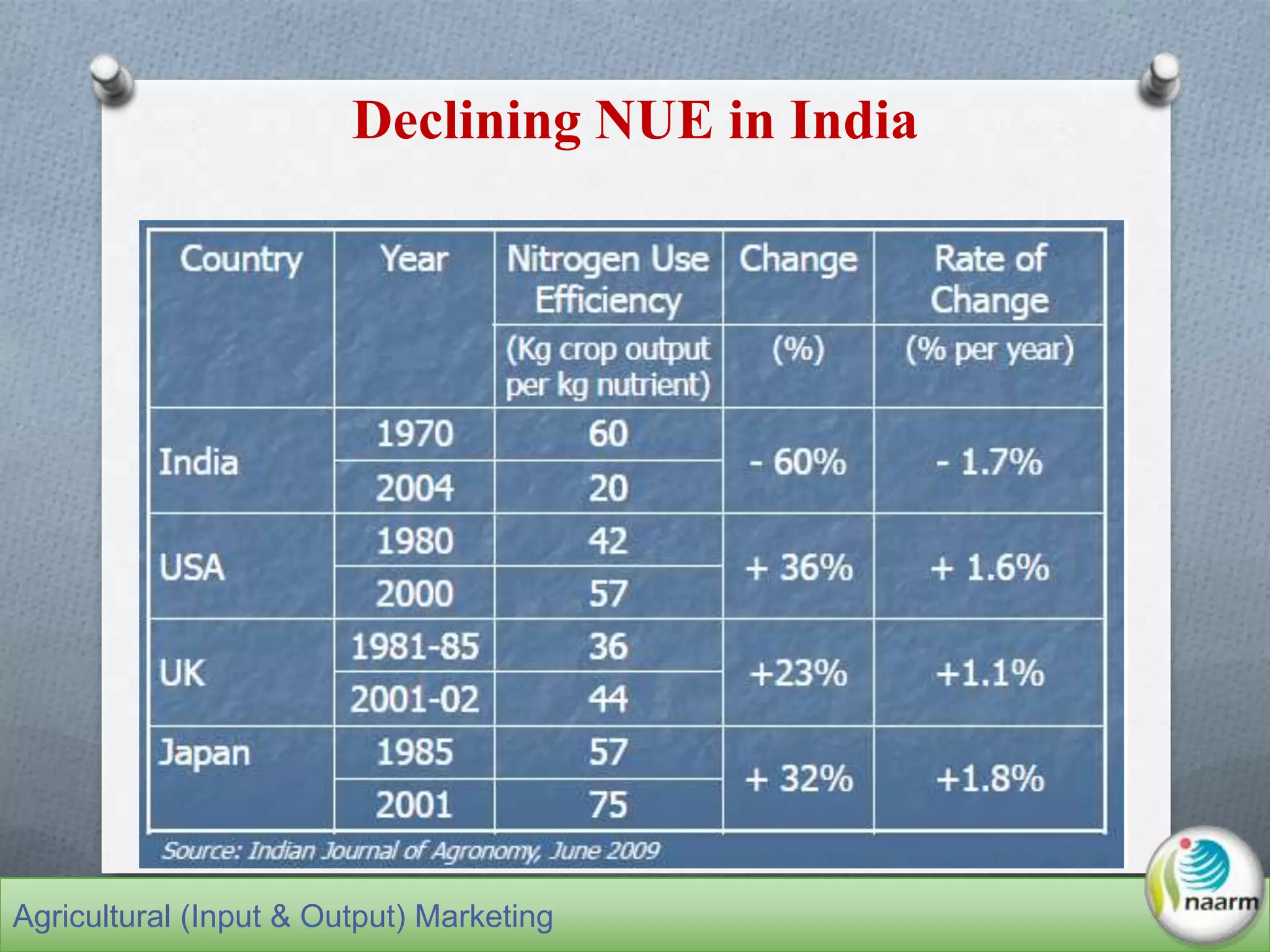

This document provides an overview of farm inputs and management in India. It discusses key agricultural inputs such as seeds, fertilizers, and pesticides. For seeds, it summarizes India's seed industry size, key players, seed replacement rates, export and import policies. For fertilizers, it outlines consumption trends, production, the role of subsidies, and challenges around nutrient use efficiency. For pesticides, it briefly discusses India's pesticide industry and market distribution by product categories. The document aims to educate about the various agricultural inputs and management practices important for Indian agriculture.