Downloaded 98 times

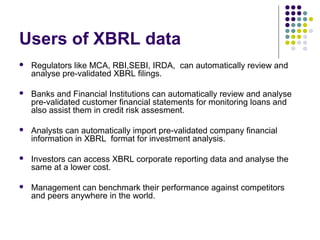

XBRL provides opportunities for accountants by allowing automated processing of business information. It saves time and reduces errors by avoiding manual data entry. Regulators, banks, analysts and others can use XBRL to more efficiently analyze validated financial statements. ICAI formed a group to promote XBRL in India, developing taxonomies and training professionals. The MCA now mandates some companies to file financial statements in XBRL format. This creates opportunities for accountants to help companies with regulatory filings and prepare XBRL financial statements.