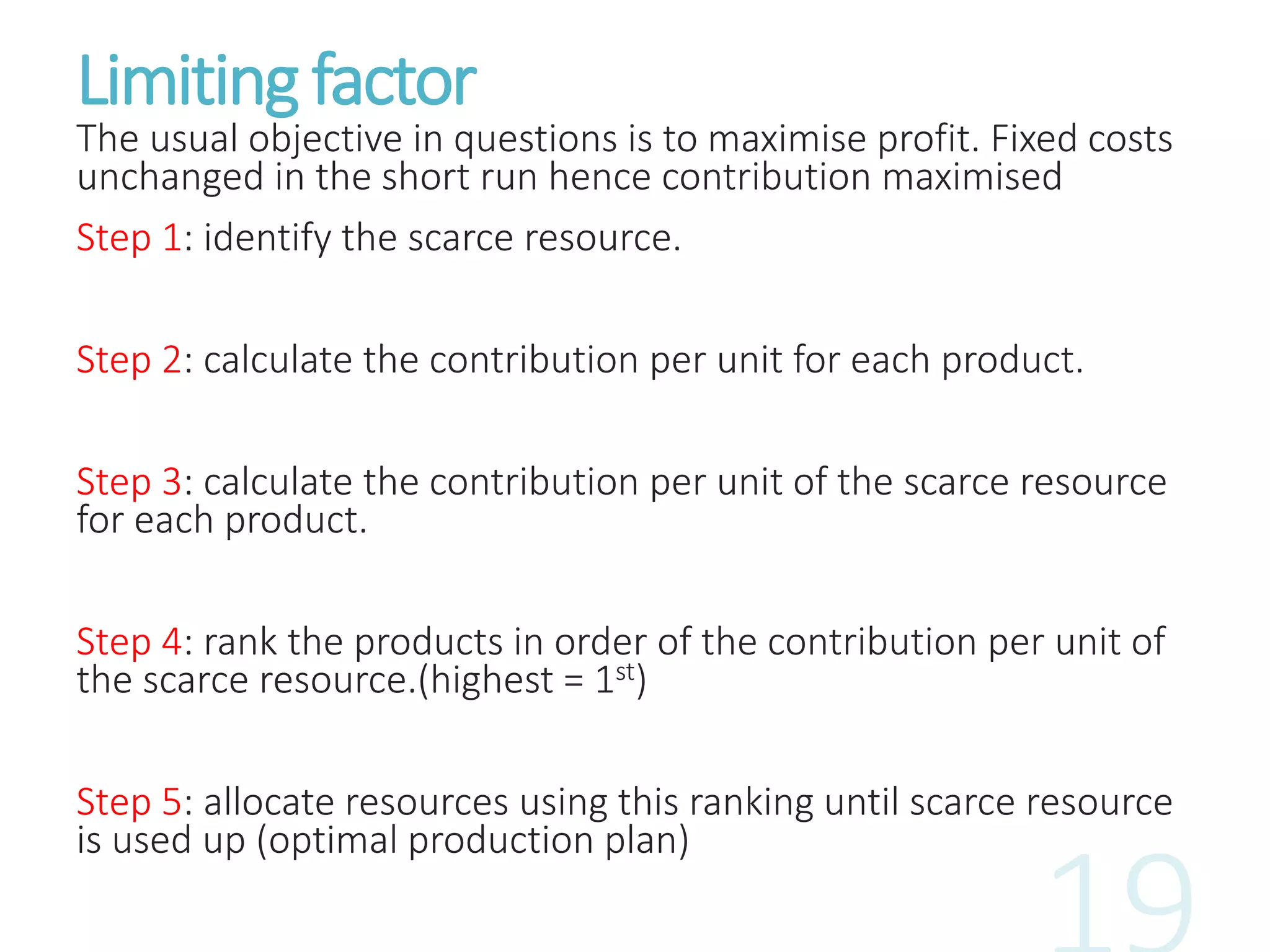

This document discusses marginal costing and its use in short-term decision making. It provides examples of how marginal costing can be used to make make-or-buy decisions by considering only variable costs, one-off order decisions by evaluating contribution, product discontinuation decisions by analyzing contribution per product, and limiting factor analysis to determine optimal production levels when there are resource constraints. Fixed costs are generally ignored in short-term decision making unless they are incremental to the decision being considered. Marginal costing allows managers to focus on costs and revenues that change with different short-term business decisions.

![Lesson 9--production[1]](https://cdn.slidesharecdn.com/ss_thumbnails/lesson-9-production1-130409195935-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)