The audit report summarizes an internal audit training session on report writing. The training covered objectives of client reporting, types of reporting engagements, intended users, key reporting standards, the process of developing reports from initial queries to final reporting, examples of reporting improvements, and general tips. The document provided details on standards and guidelines for different types of reports, the basic elements and structure of reports, communication best practices, and how to analyze audiences and assess risks and impacts. The training aimed to provide guidance and practical exercises for developing clear, concise, constructive audit reports.

![Page 20

Insert Organization Logo

Here

Internal Audit Report

[Name of Entity]

[Name of Audit Area / Location / Period Covered]

Date:

Distribution

For action For information

Insert name or business unit/group [Insert title] Insert name or business unit/group [Insert title]

[Insert name] [Insert title] [Insert name] [Insert title]

[Insert name] [Insert title] [Insert name] [Insert title]](https://image.slidesharecdn.com/veritaauditreportwritingtrainingv1-130527141802-phpapp01/85/Verita-audit-report-writing-training-v1-20-320.jpg)

![SCOPE OVERVIEW

Summary of objective and scope

[Sample text: An internal audit of [insert organization name] [insert process name] was performed in [insert month and year] and covered [insert business unit(s)].

The overall objective of the internal audit was to determine the effectiveness of key controls as identified with Management and compliance with current policies and

procedures relating to [insert process name], and to identify any improvement opportunities. The internal audit did not cover [insert any specific areas not covered and

any significant limitations].

The specific objectives, scope and approach of the internal audit were agreed with [insert organization name] Management.

Responsibilities of the Management and Internal Auditors

The internal audit procedures rely on information and representations made available to the internal auditor by the management of the Company and comprise

inquiries and observations and limited tests of transactions on a sample basis, covering the detailed assessment objectives. Accordingly, the internal audit procedures

may not detect fraud, defalcations and irregularities.

Internal auditors work does not in any way diminish the responsibilities of the Company’s management. The design, development, implementation and operation of

internal control systems are the responsibility of the respective Company’s managers. They are accountable for ensuring that adequate controls exist in the areas of

their responsibility and should not rely solely on periodic visits as a means of monitoring the adequacy and integrity of controls.

Linkage to your risk assessment study

[Sample text – option 1: This report delivery is planned in the Internal Audit Plan of [year] as approved by the Audit Committee. The scope areas have been risk

assessed in the Risk Assessment Plan [insert title/reference] provided to our team during the internal audit planning stage, however, it is important to note that this

linkage does not indicate full coverage of enterprise risks which are managed through a number of business processes and control procedures.]

[Sample text – option 2: This internal audit has been performed at the request of the [insert title e.g. Audit Committee/CEO/CFO] of [insert organization name]. This

ad hoc internal audit is in addition to the internal audits set out in the 201X/201X Internal Audit Plan.]](https://image.slidesharecdn.com/veritaauditreportwritingtrainingv1-130527141802-phpapp01/85/Verita-audit-report-writing-training-v1-22-320.jpg)

![METHODOLOGY:

INTERNAL AUDIT APPROACH

APPROACH

[Sample text: The internal audit of [insert organization name] [insert process name]

was performed using the following approach:

•[insert nature of specific procedures and testing performed to meet the

objectives of the internal audit, for example:

• names and titles of organization management/personnel interviewed

• details of information and documentation provided

• processes/systems documented

• areas and time period of walk-throughs, and observation and enquiry

performed

• areas, extent (i.e. sample sizes) and time period of items selected for testing

• the use of any third party subcontractors, where agreed with the

organization].]

INTERNAL AUDIT TEAM

Prepared by:

Name: Signature:

Reviewed by:

Name: Signature:](https://image.slidesharecdn.com/veritaauditreportwritingtrainingv1-130527141802-phpapp01/85/Verita-audit-report-writing-training-v1-23-320.jpg)

![Key findings and recommendations

[Sample text: The findings identified during the course of this internal audit are illustrated in the summary below. A full list of the findings identified and the

recommendations made is included in this report. Classifications of internal audit findings are detailed in Appendix X to this report.

These findings and recommendations were discussed with [insert organization name] Management responsible for the operations of [insert process name].

Management has accepted the findings and has agreed action plans to address the recommendations. This report also includes any findings and recommendations

where Management has implemented the action plans to date.

The management action plans will be included in the tracking of internal audit recommendations maintained by [insert name of the function responsible for internal

audit]

Executive Summary (Contd.)

Sr. No. Risk Rating Observation Headline / Title Observation Summary Recommendation Summary Detailed

Observation #

1. High

2. Medium

3. Low

Sr.

No.

Report Number of

Observations

Number of High rated

Observations

Implemented Direct Financial Benefits

1.

2.

3.](https://image.slidesharecdn.com/veritaauditreportwritingtrainingv1-130527141802-phpapp01/85/Verita-audit-report-writing-training-v1-27-320.jpg)

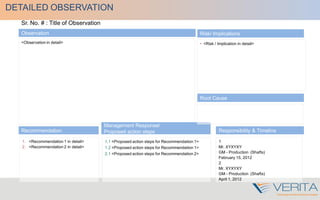

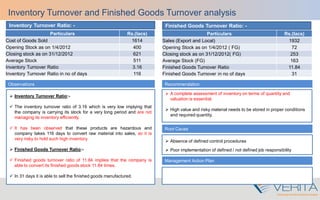

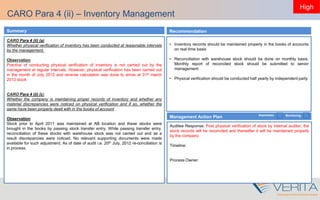

![Storage Facility

On verifying the storage facility, it was observed that bins and pallets were allocated

without proper spacing and stacking of products. Many of the bins were kept empty and

some bins & pallets were not utilized fully.

• As per the agreement with Aramex, Inward Process Point no.5.2 - Di representative

to be present during barcode pasting when no barcode are there on the products on

receipt, however on discussion it was learned that Aramex staff did bar code pasting

on their own and they were never accompanied by Di staff during this process.

• It was observed that practice of affixing preprinted system generated barcodes on

the material boxes is not in place and handwritten codes are affixed on the same

which are highly susceptible to errors. Also if any box has got empty and new

material is store in it, previous label code is not removed and new label code is affix

on the same. Thus 2 codes are reflected on the same box.

• 27 cases have been observed where location is incorrectly defined in the Optilog.

This makes tracking of materials difficult in case of emergency. [Refer Annexure VII

for details]

• As per agreement with Aramex, all rusted/corroded fittings to be isolated from

saleable inventory, however it was observed that many of the rusted materials were

still stored along with good quality materials and this can affect the quality of non-

rusted materials.

• Also as per agreement, rubber hose should be securely stretch-wrapped and stored

in warehouse, however during verification it was observed that some hose were lying

unwrapped.

• Cameras and smoke detectors at bin storage area on 2nd floor were not in working

condition.

All the operational gaps to be filled in by taking utmost care and using due diligence

for a better and smooth functioning business operation. Detailed list of

recommendation as per next slide.

Recommendation

• Auditee Response:

• Timeline:

• Process Owner:

Observation

Management Action Plan Awareness Monitoring

• Operation ineffectiveness

Root cause

Operational

Ineffectiveness

System

Deficiency

External

Design

Deficiency

High

Risk Implication Operational Control Compliance

• Financial loss to Dixon due to overcharging by Aramex.

• Handwritten codes are susceptible to errors

• Incorrect geographical mapping may lead to unfulfilled sales order due to misplaced items.

• Rusted/corroded items to be separated to avoid damage to other good products.

• Rubber hoses to be covered to avoid getting it dirty and its appealing looks may get diminished.

• Non-functioning Cameras, no audit trail in case of theft. Insurance claim may be denied.

Root cause](https://image.slidesharecdn.com/veritaauditreportwritingtrainingv1-130527141802-phpapp01/85/Verita-audit-report-writing-training-v1-36-320.jpg)