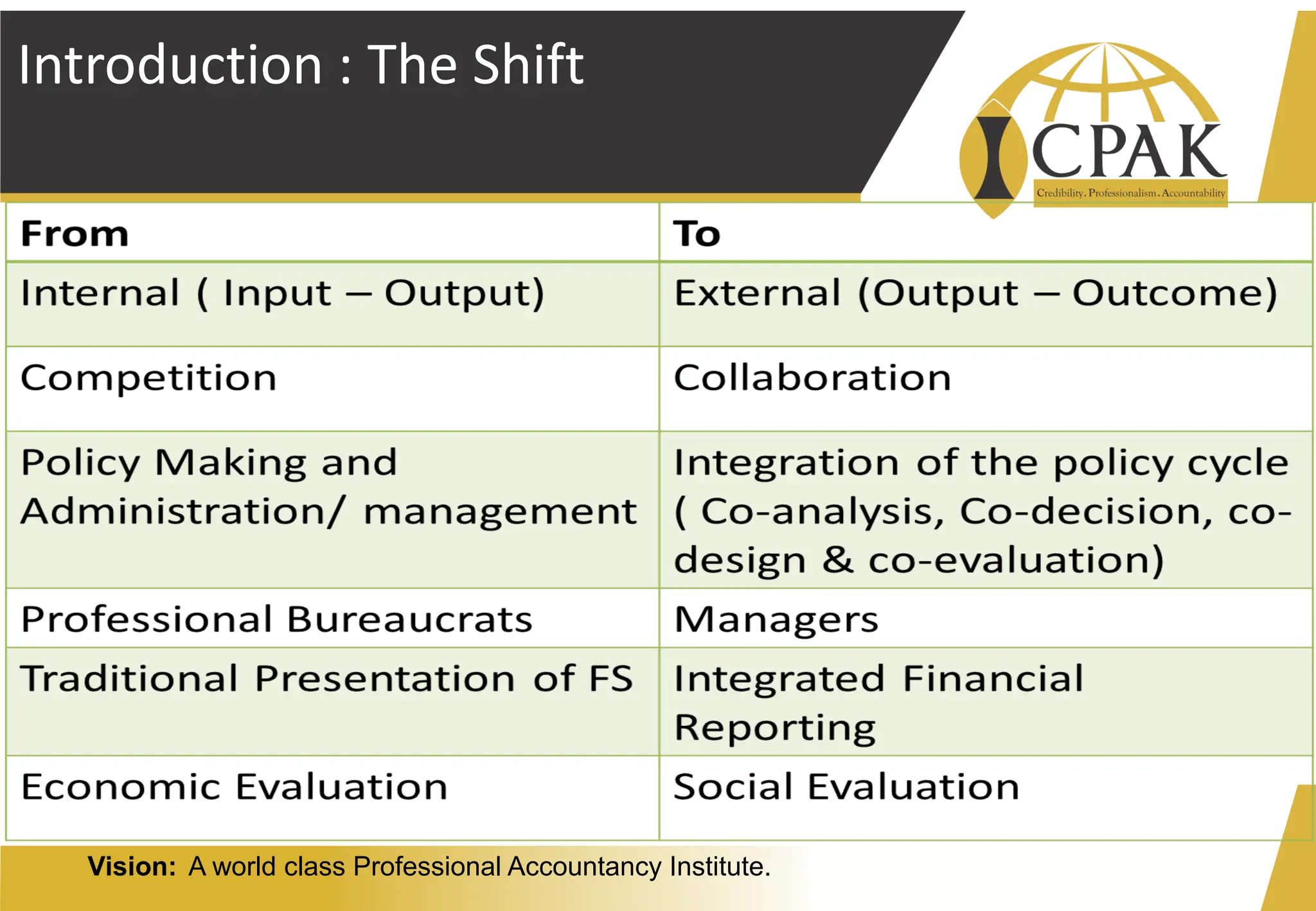

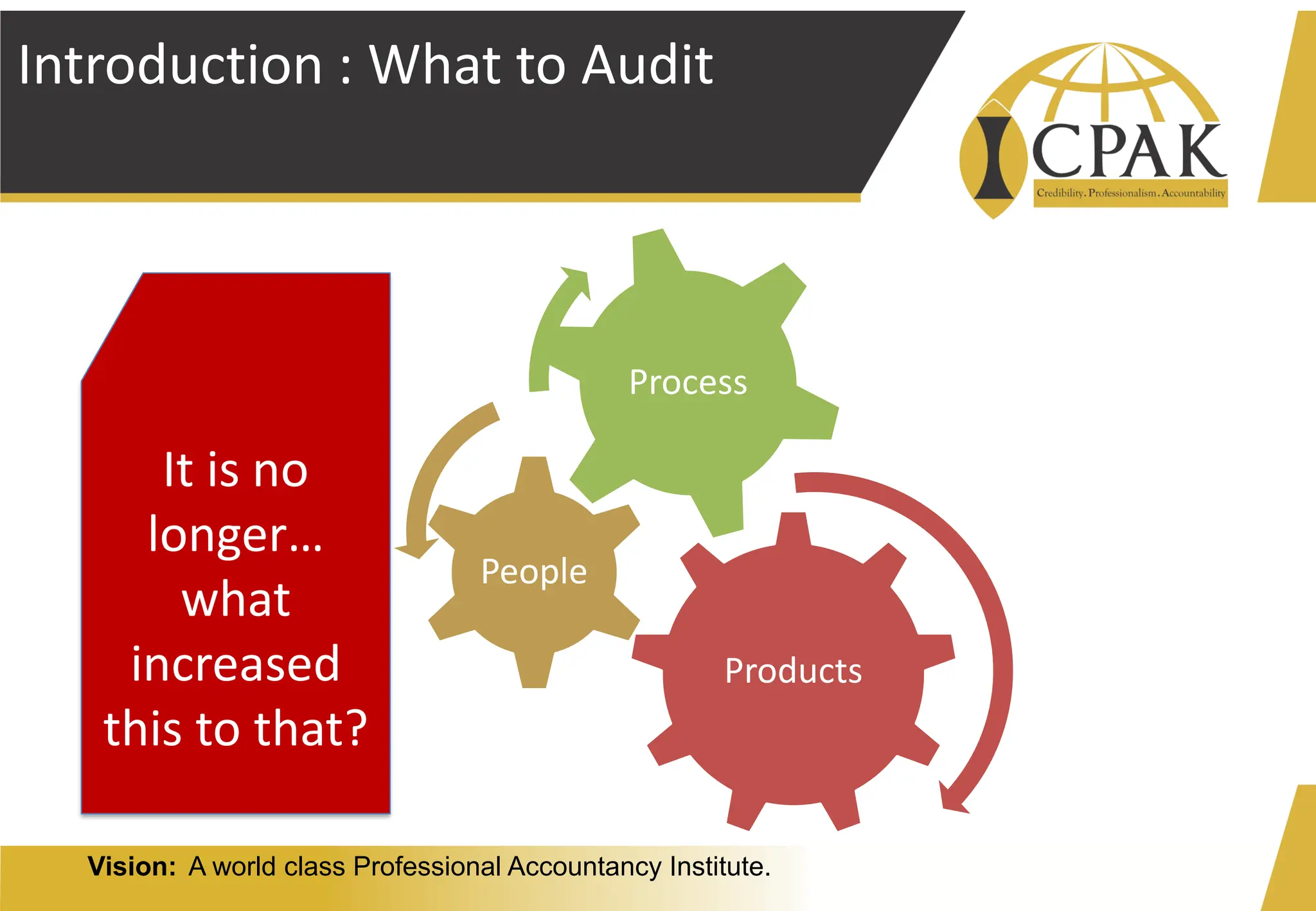

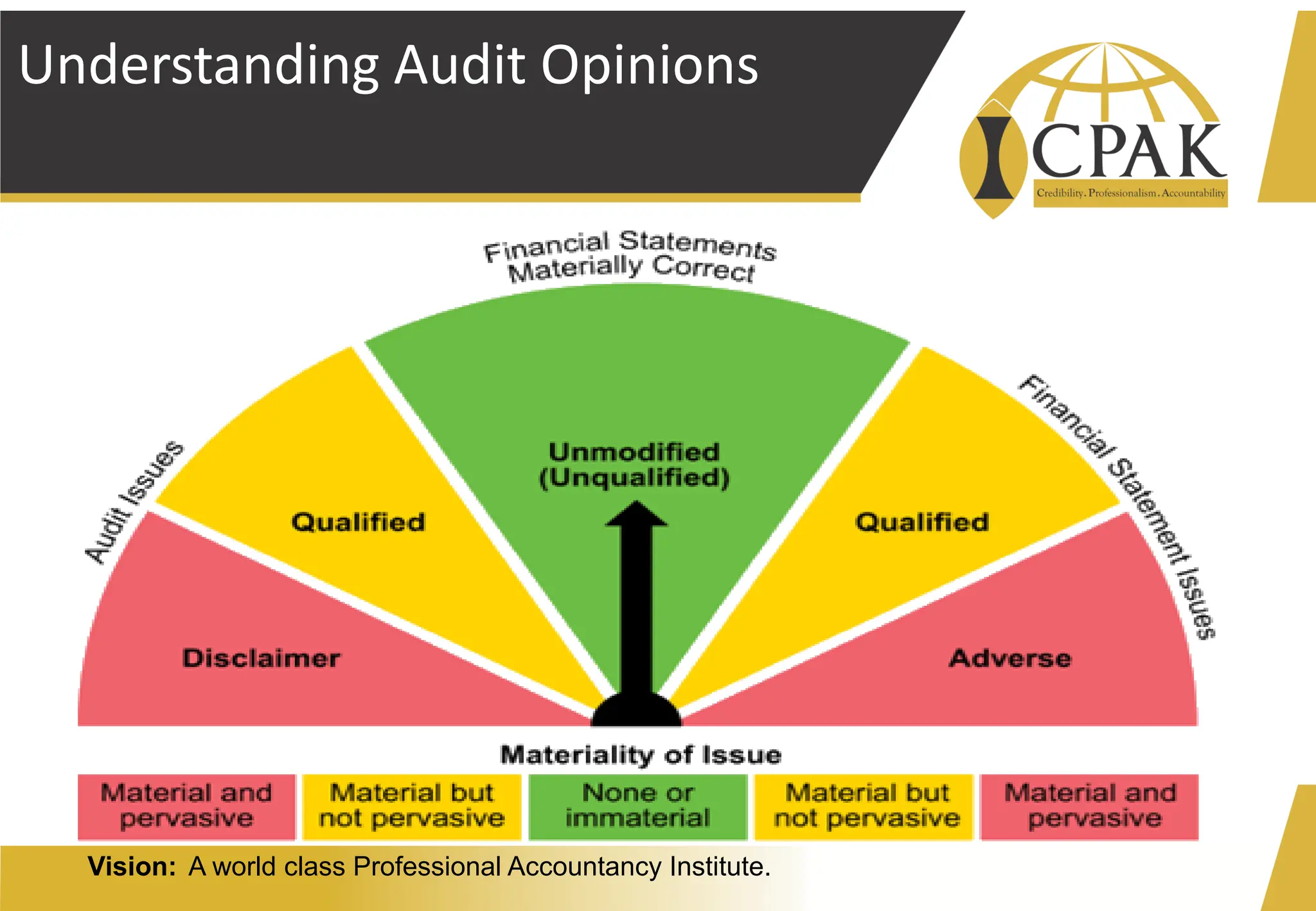

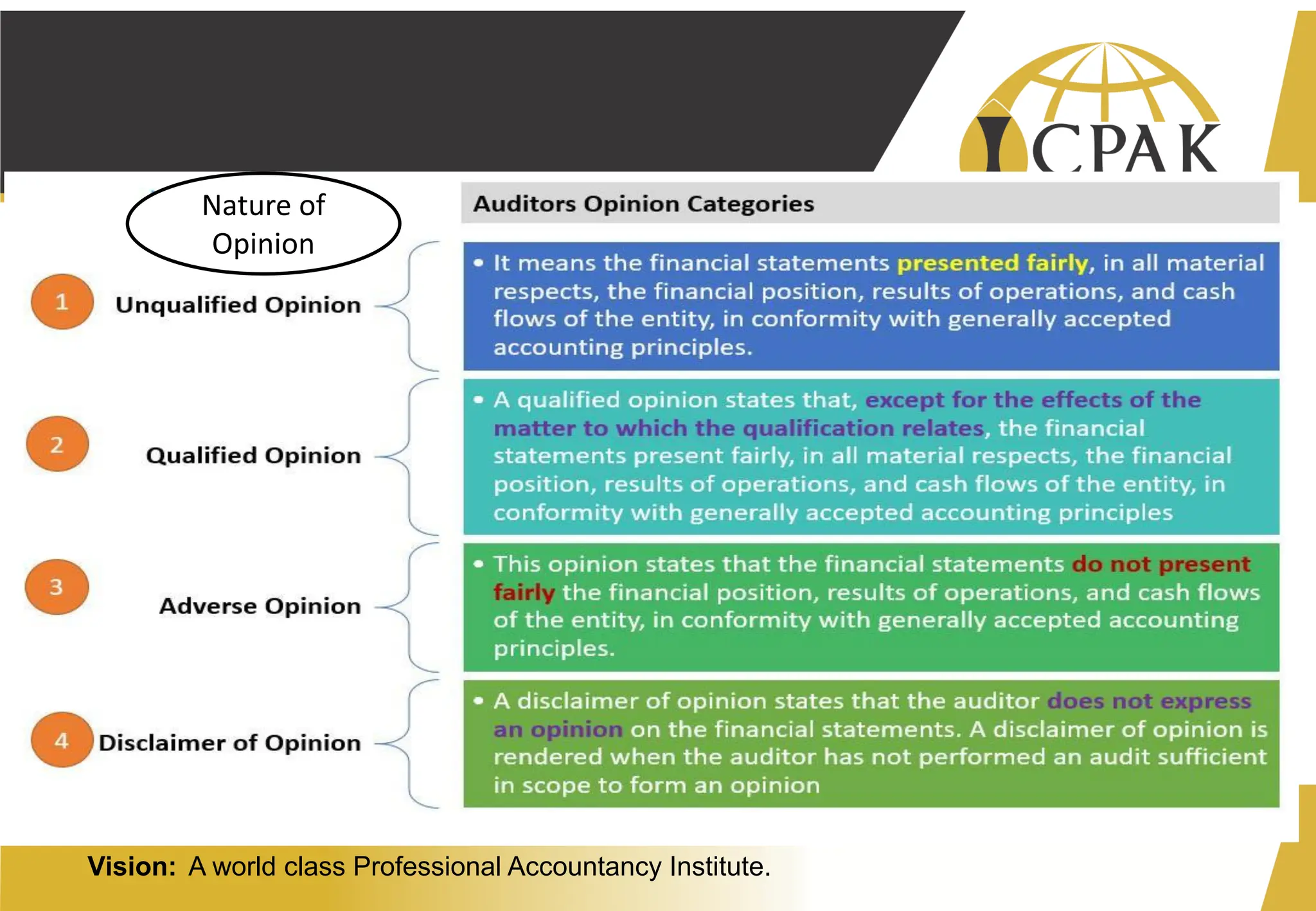

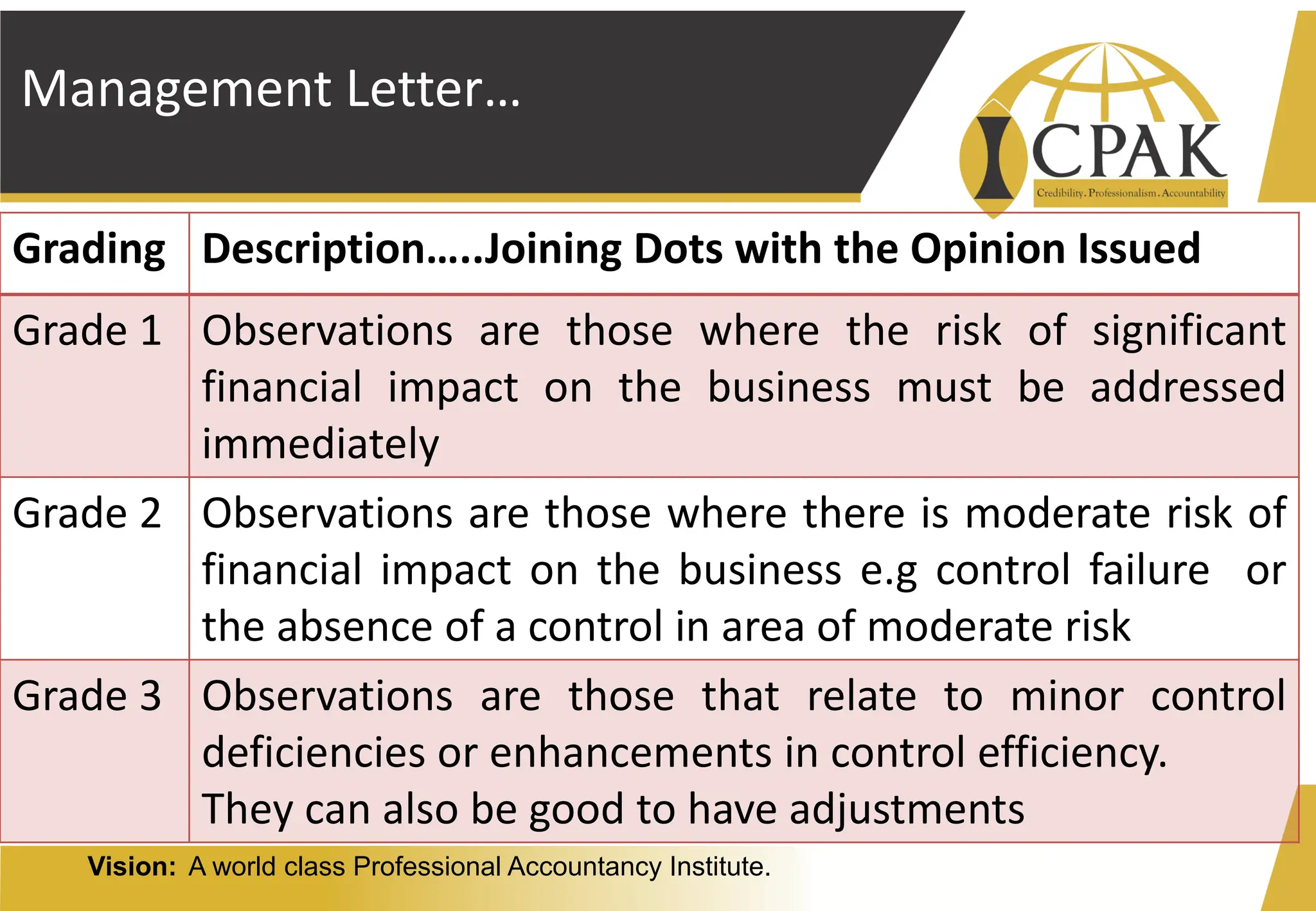

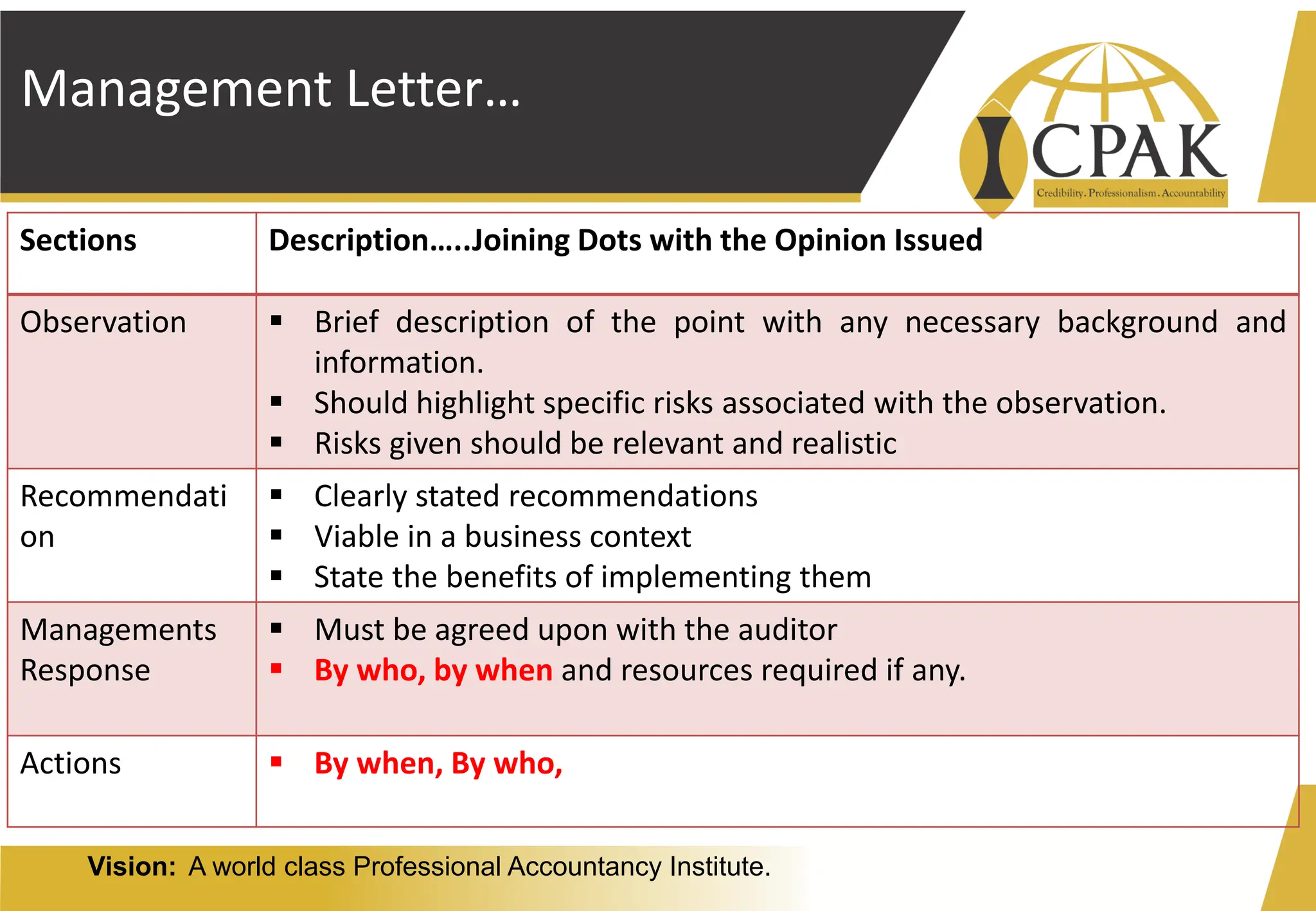

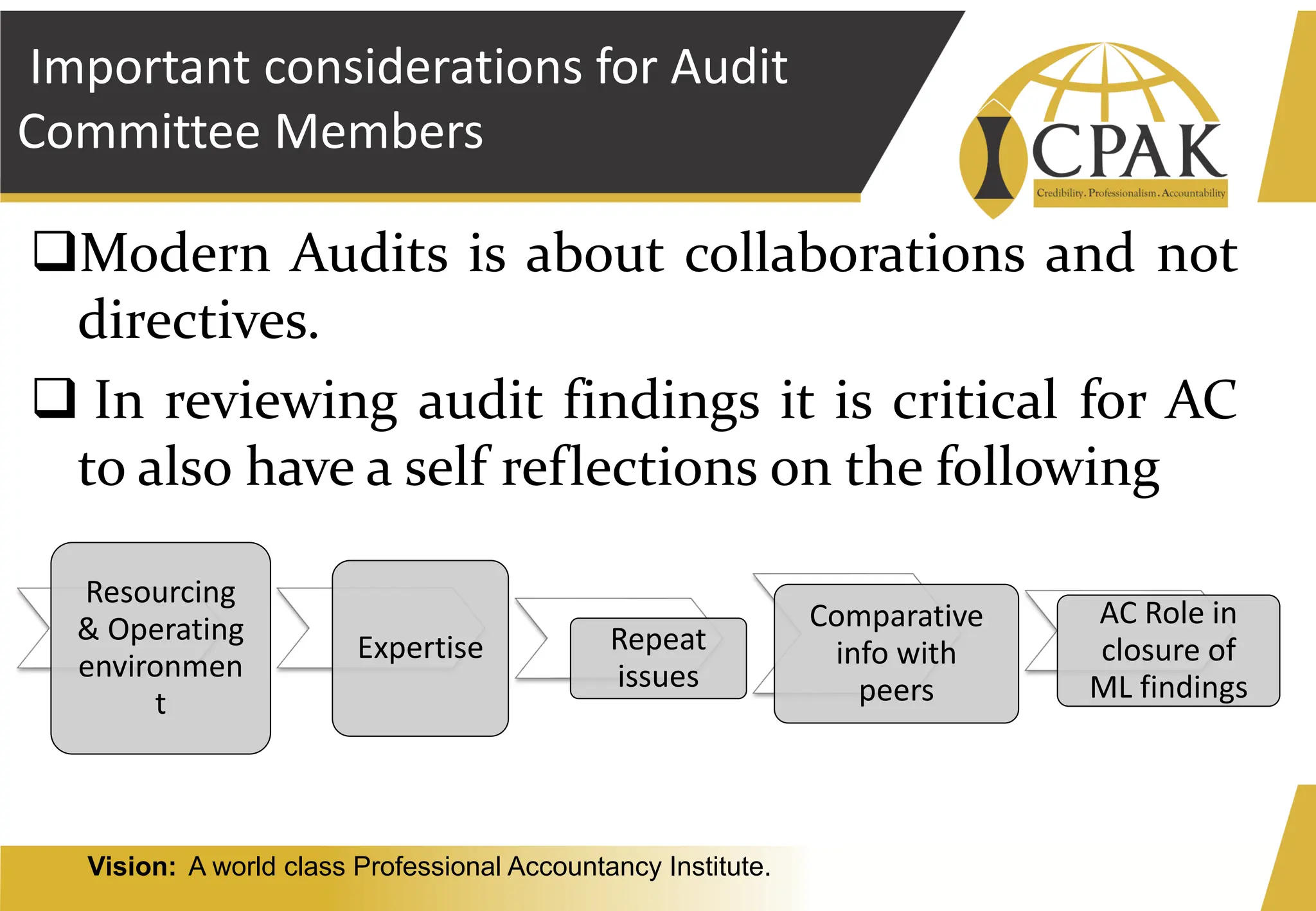

The document presents an overview of audit processes, focusing on internal and external audits, the importance of audit committees, and key audit matters. It discusses various aspects of audits such as products, people, and processes, while emphasizing the significance of management letters and auditor opinions. The conclusion highlights the necessity of trust with verification in auditing practices.

![DND - Cost Reduction Strategies to Enhance Operational Efficiency for SMEs[1]...](https://cdn.slidesharecdn.com/ss_thumbnails/dnd-costreductionstrategiestoenhanceoperationalefficiencyforsmes1-241028085054-45982cc1-thumbnail.jpg?width=640&height=640&fit=bounds)

![DND - Cost Reduction Strategies to Enhance Operational Efficiency for SMEs[1]...](https://cdn.slidesharecdn.com/ss_thumbnails/dnd-costreductionstrategiestoenhanceoperationalefficiencyforsmes1-240922065555-6ee2ed93-thumbnail.jpg?width=640&height=640&fit=bounds)