Downloaded 248 times

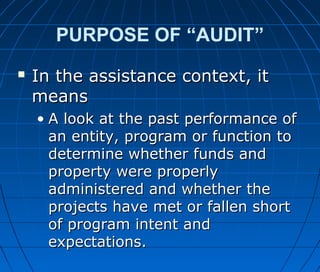

![CASE - It can’t be done!CASE - It can’t be done!

““Management wants us to add onManagement wants us to add on

these quality activities to ourthese quality activities to our

regular duties without giving usregular duties without giving us

the additional time [to accomplishthe additional time [to accomplish

them] -- it can’t be done!”them] -- it can’t be done!”

Discussion - How can it be done?Discussion - How can it be done?

Has your employer implementedHas your employer implemented

any quality improvementany quality improvement

programs?programs?

How was it done?How was it done?](https://image.slidesharecdn.com/complianceaudit-140806173710-phpapp01/85/Compliance-audit-44-320.jpg)

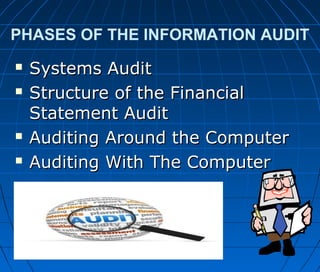

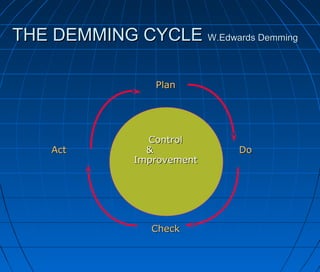

This document discusses understanding audits, reviews, and continuous improvement. It defines an audit as an independent examination of records and activities to assess controls and ensure compliance. The purpose is to evaluate operations, compliance, economy, and effectiveness in achieving goals. Effective audits involve early involvement, informal assessments, knowledge sharing, and self-assessments. Audits can be internal or external. Internal audits independently appraise operations, while external audits are conducted by independent firms. Risk assessment, monitoring, and the Deming cycle of plan-do-check-act are important for continuous improvement.

![AUDIT REPORT [ AUDITING ]](https://cdn.slidesharecdn.com/ss_thumbnails/auditingtypesofauditreport-210303052610-thumbnail.jpg?width=640&height=640&fit=bounds)