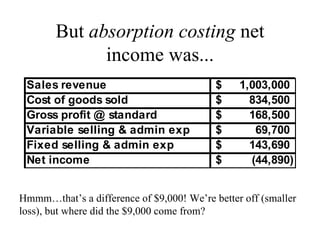

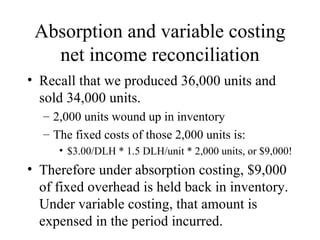

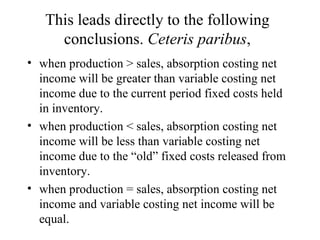

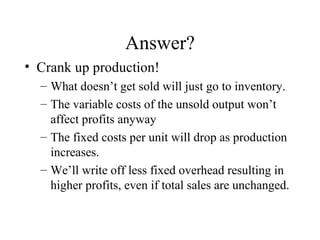

Absorption costing charges fixed overhead costs to inventory and cost of goods sold, while variable costing expenses all fixed costs in the period incurred. When production exceeds sales, absorption costing reports higher net income than variable costing due to fixed costs held in inventory. When sales exceed production, absorption costing reports lower net income due to release of fixed costs from inventory. When production equals sales, the net incomes are the same under both methods.