Overview

1. Introduction

2. TwoConceptual Formats of Income Statements

3. General Approach to Absorption and Variable Costing

4. Comparing Absorption and Variable Costing

5. Advantages and Disadvantages of Absorption and

Variable Costing

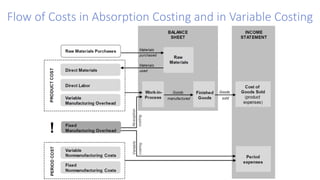

Absorption Costing vs.Variable Costing

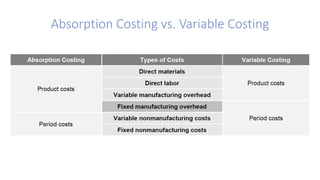

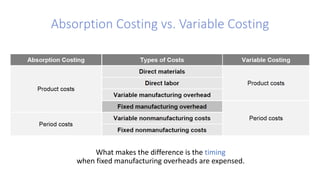

• Absorption costing assigns all (variable and fixed) manufacturing costs to

products. Consequently, under absorption costing, inventories are valued

at all manufacturing costs – direct materials, direct labor, variable

manufacturing overhead and fixed manufacturing overhead.

• Variable costing assigns only the variable manufacturing costs to products.

That is, under variable costing, inventories are valued at variable

manufacturing costs – direct materials, direct labor, and variable

manufacturing overhead. Fixed manufacturing overhead (● e.g., factory

depreciation and insurance, supervisory salaries, and so on) is not included in

the inventory valuation and is treated as a period cost, like all

nonmanufacturing costs.

6.

Absorption Costing vs.Variable Costing

• Absorption costing assigns all (variable and fixed) manufacturing costs to

products. Consequently, under absorption costing, inventories are valued

at all manufacturing costs – direct materials, direct labor, variable

manufacturing overhead and fixed manufacturing overhead.

• Variable costing assigns only the variable manufacturing costs to products.

That is, under variable costing, inventories are valued

at variable manufacturing costs – direct materials, direct labor, and variable

manufacturing overhead. Fixed manufacturing overhead (● e.g., factory

depreciation and insurance, supervisory salaries, and so on) is not included in

the inventory valuation and is treated as a period cost, like all

nonmanufacturing costs.

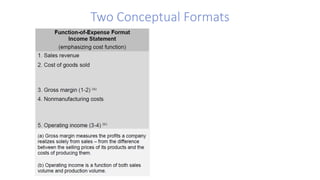

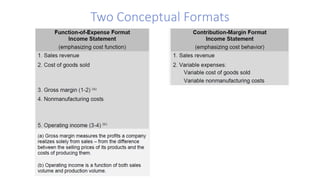

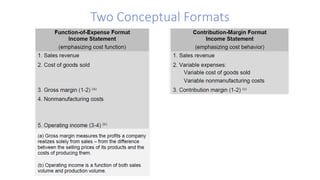

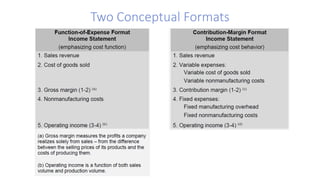

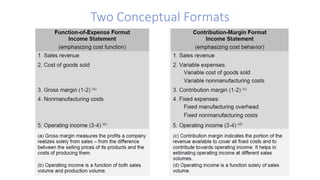

• The function-of-expenseformat income statement classifies costs only by

business functions of production, sales, and administration – generally, into

manufacturing costs, selling costs, administrative costs.

• It emphasizes the distinction between manufacturing and nonmanufacturing

costs.

The Function-Of-Expense Format

18.

In his famous“Accounting Theory”, Hendriksen (1982, pp. 189–190) makes interesting

suggestions regarding the classification of expenses on the income statement. He points

out:

The classification of expenses as “selling”, “administrative", or “cost of goods sold” may be useful for …

establishing functional responsibilities. However, for external reporting purposes, it serves no particular useful

function. The reader of financial reports is neither better able to make predictions by using this classification nor

able to evaluate the contributions of the several functions… The “cost of goods sold” is an expense just as much

as sales representatives’ salaries. Care should be taken to avoid the assignment of priorities to expenses; all are

equal in the determination of income. Expenses are not recovered in preferential order…

Hendriksen gives two suggestions. First, this is the classification “that describes the

behavioral nature” of the costs – whether they are variable or fixed. Second, this is the

disclosure of the relationship between costs and cash outflows.

The Function-Of-Expense Format

19.

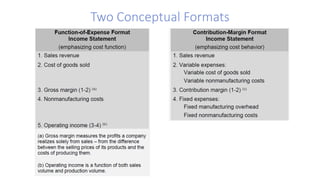

The Contribution-Margin Format

•The contribution-margin format income statement classifies costs, first, by

cost behavior (into variable and fixed costs) and, second, by business

function.

• It highlights the crucial distinction between variable and fixed costs.

• Variable costs are presented together, but in two separate sections:

− The first section presents the variable manufacturing costs under the heading variable cost of

goods sold. It includes the variable manufacturing costs.

− The second section includes all variable nonmanufacturing expenses. Note that these costs are

period expenses and are not inventoried.

• Fixed costs are also presented together as period expenses.

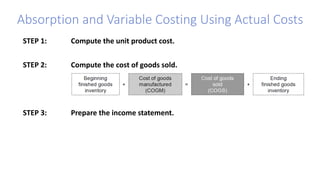

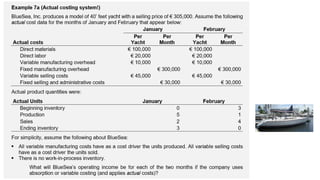

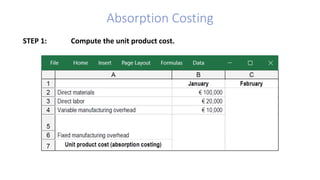

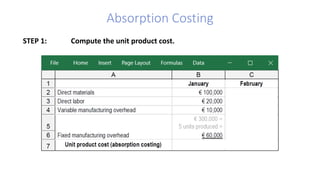

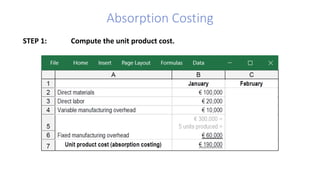

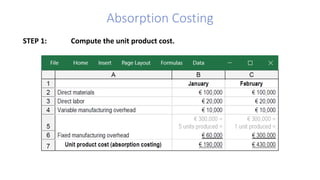

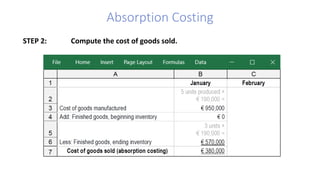

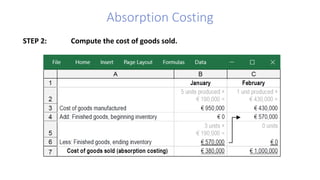

Absorption and VariableCosting Using Actual Costs

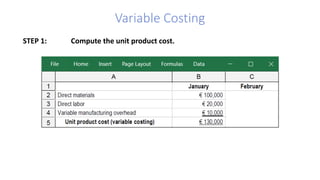

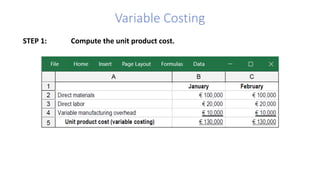

STEP 1: Compute the unit product cost.

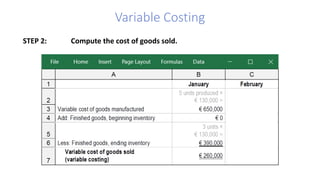

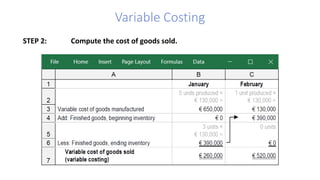

STEP 2: Compute the cost of goods sold.

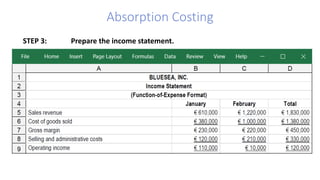

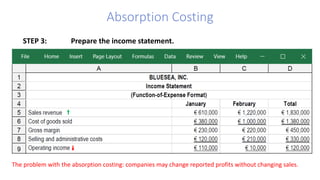

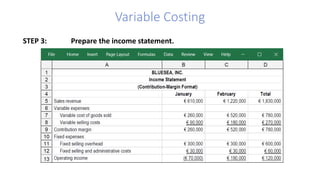

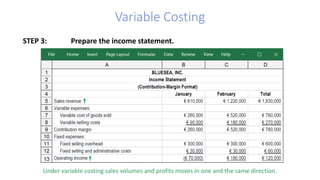

STEP 3: Prepare the income statement.

Absorption Costing

STEP 3:Prepare the income statement.

The problem with the absorption costing: companies may change reported profits without changing sales.

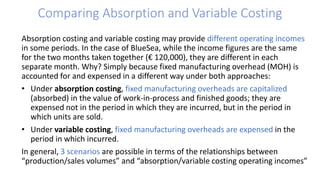

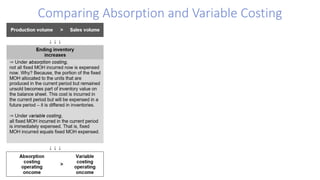

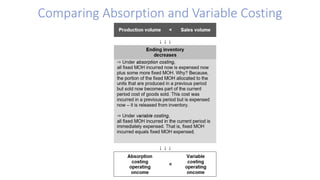

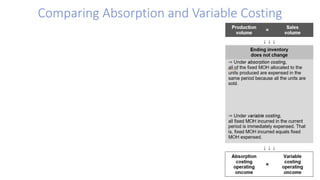

Comparing Absorption andVariable Costing

Absorption costing and variable costing may provide different operating incomes

in some periods. In the case of BlueSea, while the income figures are the same

for the two months taken together (€ 120,000), they are different in each

separate month. Why? Simply because fixed manufacturing overhead (MOH) is

accounted for and expensed in a different way under both approaches:

• Under absorption costing, fixed manufacturing overheads are capitalized

(absorbed) in the value of work-in-process and finished goods; they are

expensed not in the period in which they are incurred, but in the period in

which units are sold.

• Under variable costing, fixed manufacturing overheads are expensed in the

period in which incurred.

In general, 3 scenarios are possible in terms of the relationships between

“production/sales volumes” and “absorption/variable costing operating incomes”

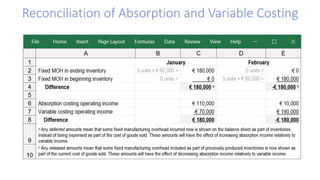

Reconciliation of Absorptionand Variable Costing

To reconcile the absorption costing and variable costing operating incomes for an

individual period it is needed to determine the amount of fixed manufacturing

overhead that was deferred in, or released from, inventories during this period.

For example, in January, the absorption costing income exceeds the variable

costing income by € 180,000 [= €110,000 – (–€70,000)].

Such kind of differences is referred to as phantom profits. They are caused solely

by building up inventories, i.e., by the fixed manufacturing overhead assigned

under absorption costing to the 3 units produced but not sold in January

[=€ 60,000 × 3 units unsold]. These fictitious profits are temporary. They

disappear in a future period when the inventories will be sold.

Advantages and Disadvantagesof Absorption and Variable Costing

In Defense of Absorption Costing. It better matches costs with revenues: the fixed

manufacturing overhead incurred in converting materials into finished goods is as

essential as all variable manufacturing costs.

In Defense of Variable (Marginal)Costing. It better matches costs with revenues: fixed

manufacturing overhead is not incurred for any particular unit produced, but for

ensuring the production capacity for a particular period of time.

• simpler for application and more straightforward for understanding and

interpretation

• unit product cost includes only variable manufacturing costs and thus

it depicts the costs of producing another unit of the product

• emphasizing the distinction between variable and fixed costs – key for decision

making and performance management

![Reconciliation of Absorption and Variable Costing

To reconcile the absorption costing and variable costing operating incomes for an

individual period it is needed to determine the amount of fixed manufacturing

overhead that was deferred in, or released from, inventories during this period.

For example, in January, the absorption costing income exceeds the variable

costing income by € 180,000 [= €110,000 – (–€70,000)].

Such kind of differences is referred to as phantom profits. They are caused solely

by building up inventories, i.e., by the fixed manufacturing overhead assigned

under absorption costing to the 3 units produced but not sold in January

[=€ 60,000 × 3 units unsold]. These fictitious profits are temporary. They

disappear in a future period when the inventories will be sold.](https://image.slidesharecdn.com/ch07variablecostinglecture-250506105302-f5bcfcdf/85/Ch07_VariableCosting_LECTUREEEEEEEEE-pdf-42-320.jpg)