Tutorial 6 -_company_reconstruction_answer (1)

•Download as DOCX, PDF•

0 likes•1,987 views

This document provides an example solution to a company reconstruction tutorial question. It includes journal entries to record various transactions as part of the reconstruction, including a capital reduction, debt for equity swap, asset sale, and share conversions. It also presents the post-reconstruction statement of financial position, showing the company's assets, liabilities and shareholders' equity after implementing the reconstruction plan.

Report

Share

Report

Share

Recommended

Tutorial 6 a141-_company_reconstruction

FiZy Bhd experienced significant losses in recent years and proposed a capital rearrangement scheme to ensure the company's survival. The scheme involved reducing ordinary share values, exchanging preference shares for new preference and ordinary shares, issuing shares to settle debt with debenture holders and directors, selling investments, paying creditors, writing off losses and revaluing assets.

Topic 9 company_reconstruction_a141

The document discusses various methods of company reconstruction including internal and external reorganization. Internal reorganization involves altering a company's capital structure through actions like changing authorized capital, reducing paid up capital, issuing bonus shares, or redeeming preference shares. External reorganization involves arrangements with outsiders such as disposing of assets/liabilities, debt restructuring schemes, business combinations, or devising a scheme to avoid liquidation. Specific examples and journal entries are provided to illustrate reduction of paid up capital through cancellation of losses or uncalled capital. The overall goal of reconstruction is to help distressed companies adapt, restructure finances, and potentially avoid liquidation.

Taxation 2 : Chapter 1

This document discusses different types of partnerships and how to calculate partnership tax. It defines salaried partners, full partners, limited partners, and sleeping partners. It also provides the steps to calculate a partnership's provisional adjusted income, divisible income, partners' statutory income, aggregate income, total income, and tax due after applying personal reliefs. The document serves as a guide for partnership taxation.

Taxation principles: Dividend, Interest, Rental, Royalty and Other sources of...

1. The document discusses various types of income that are taxable under Section 4 of the Malaysian Income Tax Act 1967, including dividend income, interest income, rental income, royalty income, pension income, and other periodic payments.

2. It provides details on how each type of income is defined, taxed, exempted, and the applicable basis periods. Key changes discussed include Malaysia replacing its imputation system for taxing dividends with a single-tier system from 2008.

3. The document also examines deductions that can be claimed against income and losses from rented property, as well as differences in how income derived in Malaysia is taxed for residents versus non-residents.

Chapter 4 RPGT

This document provides an overview of Real Property Gains Tax (RPGT) in Malaysia. Some key points:

- RPGT is a tax on capital gains from the disposal of real property in Malaysia, including residential/commercial properties and land. The tax is computed based on the difference between the disposal price and acquisition price.

- RPGT rates range from 0-10% depending on the holding period, with longer holding periods subject to lower rates.

- Various exemptions are available, including for gains below RM10,000 and disposal of a private residence.

- The acquisition date generally coincides with the disposal date between parties. Losses can be carried forward indefinitely except for shares in real property companies.

Chapter 3 agriculture allowance studnt

This document discusses the definition and computation of agriculture allowances under Malaysian tax law. It defines qualifying agriculture expenditures that allowances can be claimed on, such as land clearing and preparation, new planting, and construction of roads, buildings, and structures on farms. It provides the rates of allowances for different types of qualifying expenditures. It also addresses the treatment of allowances on the disposal or transfer of assets, including apportioning allowances between the transferor and transferee. Agriculture charges that may arise from government grants are also discussed.

Financial Analysis on Maybank and CIMB (Bank Management)

This document provides an analysis of the financial performance of Maybank and CIMB from 2010-2014. Key metrics analyzed include liquidity, profitability, financial leverage, and asset quality. For liquidity, the analysis found that Maybank's current ratio increased from 2010-2014 while CIMB's decreased, indicating weaker liquidity. For profitability, ratios for both banks fluctuated over the period. Maybank generally had higher ratios except for earnings to assets in 2012. The analysis found CIMB had higher financial leverage than Maybank based on debt to equity ratios, though both lowered leverage in 2014. In terms of asset quality, Maybank's non-performing loan ratio was stable at 1% while CIM

Chapter 4 (b)employment income

This document discusses types of gross employment income that are taxable under Malaysian tax law. It covers various types of monetary income like wages, salary, bonuses, and allowances. It also discusses benefits in kind such as company cars, mobile phones, interest subsidies, and furnished accommodation. Various examples are provided to illustrate how different types of income and benefits are treated, such as share options, reimbursements, leave pay, gratuity, and car benefits including the prescribed value method.

Recommended

Tutorial 6 a141-_company_reconstruction

FiZy Bhd experienced significant losses in recent years and proposed a capital rearrangement scheme to ensure the company's survival. The scheme involved reducing ordinary share values, exchanging preference shares for new preference and ordinary shares, issuing shares to settle debt with debenture holders and directors, selling investments, paying creditors, writing off losses and revaluing assets.

Topic 9 company_reconstruction_a141

The document discusses various methods of company reconstruction including internal and external reorganization. Internal reorganization involves altering a company's capital structure through actions like changing authorized capital, reducing paid up capital, issuing bonus shares, or redeeming preference shares. External reorganization involves arrangements with outsiders such as disposing of assets/liabilities, debt restructuring schemes, business combinations, or devising a scheme to avoid liquidation. Specific examples and journal entries are provided to illustrate reduction of paid up capital through cancellation of losses or uncalled capital. The overall goal of reconstruction is to help distressed companies adapt, restructure finances, and potentially avoid liquidation.

Taxation 2 : Chapter 1

This document discusses different types of partnerships and how to calculate partnership tax. It defines salaried partners, full partners, limited partners, and sleeping partners. It also provides the steps to calculate a partnership's provisional adjusted income, divisible income, partners' statutory income, aggregate income, total income, and tax due after applying personal reliefs. The document serves as a guide for partnership taxation.

Taxation principles: Dividend, Interest, Rental, Royalty and Other sources of...

1. The document discusses various types of income that are taxable under Section 4 of the Malaysian Income Tax Act 1967, including dividend income, interest income, rental income, royalty income, pension income, and other periodic payments.

2. It provides details on how each type of income is defined, taxed, exempted, and the applicable basis periods. Key changes discussed include Malaysia replacing its imputation system for taxing dividends with a single-tier system from 2008.

3. The document also examines deductions that can be claimed against income and losses from rented property, as well as differences in how income derived in Malaysia is taxed for residents versus non-residents.

Chapter 4 RPGT

This document provides an overview of Real Property Gains Tax (RPGT) in Malaysia. Some key points:

- RPGT is a tax on capital gains from the disposal of real property in Malaysia, including residential/commercial properties and land. The tax is computed based on the difference between the disposal price and acquisition price.

- RPGT rates range from 0-10% depending on the holding period, with longer holding periods subject to lower rates.

- Various exemptions are available, including for gains below RM10,000 and disposal of a private residence.

- The acquisition date generally coincides with the disposal date between parties. Losses can be carried forward indefinitely except for shares in real property companies.

Chapter 3 agriculture allowance studnt

This document discusses the definition and computation of agriculture allowances under Malaysian tax law. It defines qualifying agriculture expenditures that allowances can be claimed on, such as land clearing and preparation, new planting, and construction of roads, buildings, and structures on farms. It provides the rates of allowances for different types of qualifying expenditures. It also addresses the treatment of allowances on the disposal or transfer of assets, including apportioning allowances between the transferor and transferee. Agriculture charges that may arise from government grants are also discussed.

Financial Analysis on Maybank and CIMB (Bank Management)

This document provides an analysis of the financial performance of Maybank and CIMB from 2010-2014. Key metrics analyzed include liquidity, profitability, financial leverage, and asset quality. For liquidity, the analysis found that Maybank's current ratio increased from 2010-2014 while CIMB's decreased, indicating weaker liquidity. For profitability, ratios for both banks fluctuated over the period. Maybank generally had higher ratios except for earnings to assets in 2012. The analysis found CIMB had higher financial leverage than Maybank based on debt to equity ratios, though both lowered leverage in 2014. In terms of asset quality, Maybank's non-performing loan ratio was stable at 1% while CIM

Chapter 4 (b)employment income

This document discusses types of gross employment income that are taxable under Malaysian tax law. It covers various types of monetary income like wages, salary, bonuses, and allowances. It also discusses benefits in kind such as company cars, mobile phones, interest subsidies, and furnished accommodation. Various examples are provided to illustrate how different types of income and benefits are treated, such as share options, reimbursements, leave pay, gratuity, and car benefits including the prescribed value method.

The Malaysian Companies Act 2016

The corporate landscape in Malaysia has been shaken up by the passing of the new Companies Act 2016. The Act came into force on 31 January, 2017, effectively repealing the Companies Act 1965. The series of slides provides you with the essential changes brought about by the new Act.

Chapter 2 iba

This document provides an overview of the industrial building allowance under Malaysian tax law. It defines an industrial building and outlines the types of expenditures that qualify for the initial allowance and annual allowance deductions. It also discusses how the allowances apply for constructed versus purchased buildings, temporary disuse of buildings, and the balancing charge or allowance applied when a building is disposed of. Eligible persons, rates for the allowances, and examples are provided to illustrate the key concepts.

Malaysian Private Entities Reporting Standard (MPERS)

Hi everyone!

This is the document on Malaysian Private Entities Reporting Standard (MPERS). Hope it helps!

Sign up for OfficeCentral at http://www.OfficeCentral.com.my

Bab 7 cash and receivables

This document summarizes key accounting concepts related to cash, receivables, and related valuation issues. It defines cash and receivables, discusses how to recognize, measure, and present them in financial statements. Specific topics covered include cash controls, restricted cash, cash equivalents, accounts and notes receivable, allowance for doubtful accounts, present value concepts for long-term notes receivable.

Company tax computation format

This document outlines the format for computing company tax in Malaysia. It lists items that are added and subtracted from net profit before tax to arrive at statutory income, including non-allowable expenses that are added back and special deductions that are subtracted. It then details the steps to calculate aggregate income, chargeable income, tax chargeable, tax credits, and final tax liability.

Corporate Reporting - MFRS116, IAS16 Property Plant and Equipment_PPE

This document discusses MFRS116 - Property, Plant and Equipment. It defines PPE and outlines the standard's scope and exceptions. PPE must meet definitions of an asset to be recognized initially at cost. Subsequent measurement can be under the cost or revaluation model. The document explains initial and subsequent measurement, self-construction, exchanges, derecognition and disclosure requirements under MFRS116 for PPE.

Foreign Currency Transactions and Financial Instruments

This document discusses foreign currency transactions and financial instruments. It begins by explaining foreign exchange rates, including direct and indirect exchange rates. It then provides examples of how exchange rates impact transactions when a currency strengthens or weakens. The document outlines the accounting for foreign currency transactions, including recording transactions at the spot rate on the transaction date and adjusting balances to the current rate on the balance sheet date. It provides an example to illustrate this two-transaction approach. Finally, it introduces how entities can use foreign currency forward exchange contracts to hedge against currency risk from international transactions.

Chapter 5; non business income students

Maria's gross rental income for YA 2012 is RM16,800 (RM2,800 x 6 months).

Allowable deductions are:

- Repainting costs of RM3,300

- Legal costs of RM1,800

- Agent's commission of RM2,800 (1 month's rent)

Total deductions = RM3,300 + RM1,800 + RM2,800 = RM7,900

Net rental income = Gross rental income - Allowable deductions

= RM16,800 - RM7,900 = RM8,900

The built-in cupboards cost of RM5,800 and utility deposit received are not allowable deductions as they are capital in nature.

ALLOWANCES-ADVANCED TAXATION

Andy Lee emailed a lecture outline on various tax allowances under Malaysian law, including agriculture, forest, and mining allowances. The document provides details on qualifying expenditures, eligibility requirements, and calculation of allowance rates for agriculture and forest allowances. It includes examples demonstrating how to calculate agriculture allowances and charges for different scenarios.

Konsep syarikat, konsep tirai perbadanan dan pengecualiannya, jenis-jenis sya...

Please do check Companies Act 2016 yeah :)

P/S : Hi, I am sharing my personal notes of law-related subjects. Some parts of them are explained in a very informal-relaxed way and mix of languages (BM and English). Secondly, as law revolves every day, there will be outdated parts in my notes. Two ways of handling it.. (1) double check with the latest law and keep it to yourself (2) same with No. 1 coupled with your generosity to share with us, the LinkedIn users (hiks ^_^). Till then, have a nice day!

Accounting Principles, 12th Edition Ch16

Corporations invest in debt and stock securities for various reasons such as having excess cash or generating investment income. For debt investments, entries are made to record acquisition, interest revenue, and sale. Interest receivable and revenue are reported in financial statements. For stock investments where influence is less than 20%, the cost method is used where investments are recorded at cost and revenue is recognized on cash dividends. For influence between 20-50%, the equity method is used where the investment is adjusted for the investor's share of earnings and dividends. For over 50% influence, consolidated financial statements are prepared. Investments are classified as trading, available-for-sale, or held-to-maturity and reported differently in financial statements.

Affin Bank Berhad Analysis

Identification of Affin Bank Berhad strengths and weaknesses using PESTLE, SWOT, BCG and Porter's 5 Forces

Chapter 5 corporate tax stds (2)

Malaysian Taxation 2

42

Example (bad debt)

Runny is a building contractor. He has lent a sum without any

security to Lee a family friend who is also a contractor. Lee has

gone bankrupt and the debt has become bad. Can Runny claim

the bad debt as a deduction?

Answer:

No, the debt to Lee cannot be claimed as a bad debt deduction

as the loan was not made in the course of Runny's business as a

building contractor but was a personal/private loan to a friend.

Malaysian Taxation 2

43

Example (stock in trade)

Amal Bhd is a manufacturer of

Financial institutions

This document provides an overview of Malaysia's banking and financial system. It discusses the various types of banking institutions like commercial banks, Islamic banks, finance companies, and merchant banks that are regulated by Bank Negara Malaysia. It also outlines the roles of non-bank financial intermediaries such as insurance companies, provident funds, savings institutions and capital market institutions. Finally, it provides brief descriptions of the functions of these different financial entities in Malaysia.

Revenue cycle (AIS)

All steps that involves in a Revenue cycle are clearly explain with the help of diagrams and description

Dissolution of Partnership

The document discusses dissolution of partnership under Malaysian law. It defines dissolution and outlines ways a partnership can dissolve, either with or without court intervention. Key points include:

- Dissolution is the winding up of partnership affairs and termination of the partnership relationship

- Partnerships dissolve through expiration of term, completion of single undertaking, notice, death, bankruptcy, illegality, or court order

- The Partnership Act 1961 provides for dissolution in various situations and sets out how partnerships are wound up upon dissolution

Evolution of budgeting system in malaysia (10 page)

A group assignment for the subject 'Budget Administration', Master of Public Policy, University Malaya. This subject was taught by Tan Sri Sulaiman Mahbob, former Director-General of Economic Planning Unit, Prime Minister's Department and current Chairman of Felda Global Ventures (FGV).

Chapter 5

This document outlines the scope and content for Chapter 5 of an audit course. It covers understanding audit reports, the types of reports including unmodified and modified, and the elements and situations that result in each type of report. It also discusses the auditor's responsibilities, including maintaining professional skepticism and ensuring financial statements are free from material misstatement. The types of audits are defined as external, internal, and compliance audits.

Assignment3 -a_ranswer

1. The document contains accounting journal entries for receivables and notes receivable. It addresses recognizing bad debt expense using percentage of receivables and gross sales methods, adjusting the allowance account, and discounting notes receivable.

2. Several journal entries are provided for World Wide Finance to record loan origination, interest revenue, and cash receipts.

3. Journal entries record various transactions for an account receivable from SilaHamza including sales, returns, discounting notes receivable, bad debt expense, and assigning receivables to a factor.

12 accountancy notes_ch08_company_accounts_issue_of_debentures_02

The document contains journal entries related to the issue of debentures by a company. It records the receipt of application money from debenture applicants, allotment of debentures, and issue of debentures at par as well as at a discount of 10%. It also contains a balance sheet showing the capital received from debentures as a non-current liability and the cash received as a current asset.

More Related Content

What's hot

The Malaysian Companies Act 2016

The corporate landscape in Malaysia has been shaken up by the passing of the new Companies Act 2016. The Act came into force on 31 January, 2017, effectively repealing the Companies Act 1965. The series of slides provides you with the essential changes brought about by the new Act.

Chapter 2 iba

This document provides an overview of the industrial building allowance under Malaysian tax law. It defines an industrial building and outlines the types of expenditures that qualify for the initial allowance and annual allowance deductions. It also discusses how the allowances apply for constructed versus purchased buildings, temporary disuse of buildings, and the balancing charge or allowance applied when a building is disposed of. Eligible persons, rates for the allowances, and examples are provided to illustrate the key concepts.

Malaysian Private Entities Reporting Standard (MPERS)

Hi everyone!

This is the document on Malaysian Private Entities Reporting Standard (MPERS). Hope it helps!

Sign up for OfficeCentral at http://www.OfficeCentral.com.my

Bab 7 cash and receivables

This document summarizes key accounting concepts related to cash, receivables, and related valuation issues. It defines cash and receivables, discusses how to recognize, measure, and present them in financial statements. Specific topics covered include cash controls, restricted cash, cash equivalents, accounts and notes receivable, allowance for doubtful accounts, present value concepts for long-term notes receivable.

Company tax computation format

This document outlines the format for computing company tax in Malaysia. It lists items that are added and subtracted from net profit before tax to arrive at statutory income, including non-allowable expenses that are added back and special deductions that are subtracted. It then details the steps to calculate aggregate income, chargeable income, tax chargeable, tax credits, and final tax liability.

Corporate Reporting - MFRS116, IAS16 Property Plant and Equipment_PPE

This document discusses MFRS116 - Property, Plant and Equipment. It defines PPE and outlines the standard's scope and exceptions. PPE must meet definitions of an asset to be recognized initially at cost. Subsequent measurement can be under the cost or revaluation model. The document explains initial and subsequent measurement, self-construction, exchanges, derecognition and disclosure requirements under MFRS116 for PPE.

Foreign Currency Transactions and Financial Instruments

This document discusses foreign currency transactions and financial instruments. It begins by explaining foreign exchange rates, including direct and indirect exchange rates. It then provides examples of how exchange rates impact transactions when a currency strengthens or weakens. The document outlines the accounting for foreign currency transactions, including recording transactions at the spot rate on the transaction date and adjusting balances to the current rate on the balance sheet date. It provides an example to illustrate this two-transaction approach. Finally, it introduces how entities can use foreign currency forward exchange contracts to hedge against currency risk from international transactions.

Chapter 5; non business income students

Maria's gross rental income for YA 2012 is RM16,800 (RM2,800 x 6 months).

Allowable deductions are:

- Repainting costs of RM3,300

- Legal costs of RM1,800

- Agent's commission of RM2,800 (1 month's rent)

Total deductions = RM3,300 + RM1,800 + RM2,800 = RM7,900

Net rental income = Gross rental income - Allowable deductions

= RM16,800 - RM7,900 = RM8,900

The built-in cupboards cost of RM5,800 and utility deposit received are not allowable deductions as they are capital in nature.

ALLOWANCES-ADVANCED TAXATION

Andy Lee emailed a lecture outline on various tax allowances under Malaysian law, including agriculture, forest, and mining allowances. The document provides details on qualifying expenditures, eligibility requirements, and calculation of allowance rates for agriculture and forest allowances. It includes examples demonstrating how to calculate agriculture allowances and charges for different scenarios.

Konsep syarikat, konsep tirai perbadanan dan pengecualiannya, jenis-jenis sya...

Please do check Companies Act 2016 yeah :)

P/S : Hi, I am sharing my personal notes of law-related subjects. Some parts of them are explained in a very informal-relaxed way and mix of languages (BM and English). Secondly, as law revolves every day, there will be outdated parts in my notes. Two ways of handling it.. (1) double check with the latest law and keep it to yourself (2) same with No. 1 coupled with your generosity to share with us, the LinkedIn users (hiks ^_^). Till then, have a nice day!

Accounting Principles, 12th Edition Ch16

Corporations invest in debt and stock securities for various reasons such as having excess cash or generating investment income. For debt investments, entries are made to record acquisition, interest revenue, and sale. Interest receivable and revenue are reported in financial statements. For stock investments where influence is less than 20%, the cost method is used where investments are recorded at cost and revenue is recognized on cash dividends. For influence between 20-50%, the equity method is used where the investment is adjusted for the investor's share of earnings and dividends. For over 50% influence, consolidated financial statements are prepared. Investments are classified as trading, available-for-sale, or held-to-maturity and reported differently in financial statements.

Affin Bank Berhad Analysis

Identification of Affin Bank Berhad strengths and weaknesses using PESTLE, SWOT, BCG and Porter's 5 Forces

Chapter 5 corporate tax stds (2)

Malaysian Taxation 2

42

Example (bad debt)

Runny is a building contractor. He has lent a sum without any

security to Lee a family friend who is also a contractor. Lee has

gone bankrupt and the debt has become bad. Can Runny claim

the bad debt as a deduction?

Answer:

No, the debt to Lee cannot be claimed as a bad debt deduction

as the loan was not made in the course of Runny's business as a

building contractor but was a personal/private loan to a friend.

Malaysian Taxation 2

43

Example (stock in trade)

Amal Bhd is a manufacturer of

Financial institutions

This document provides an overview of Malaysia's banking and financial system. It discusses the various types of banking institutions like commercial banks, Islamic banks, finance companies, and merchant banks that are regulated by Bank Negara Malaysia. It also outlines the roles of non-bank financial intermediaries such as insurance companies, provident funds, savings institutions and capital market institutions. Finally, it provides brief descriptions of the functions of these different financial entities in Malaysia.

Revenue cycle (AIS)

All steps that involves in a Revenue cycle are clearly explain with the help of diagrams and description

Dissolution of Partnership

The document discusses dissolution of partnership under Malaysian law. It defines dissolution and outlines ways a partnership can dissolve, either with or without court intervention. Key points include:

- Dissolution is the winding up of partnership affairs and termination of the partnership relationship

- Partnerships dissolve through expiration of term, completion of single undertaking, notice, death, bankruptcy, illegality, or court order

- The Partnership Act 1961 provides for dissolution in various situations and sets out how partnerships are wound up upon dissolution

Evolution of budgeting system in malaysia (10 page)

A group assignment for the subject 'Budget Administration', Master of Public Policy, University Malaya. This subject was taught by Tan Sri Sulaiman Mahbob, former Director-General of Economic Planning Unit, Prime Minister's Department and current Chairman of Felda Global Ventures (FGV).

Chapter 5

This document outlines the scope and content for Chapter 5 of an audit course. It covers understanding audit reports, the types of reports including unmodified and modified, and the elements and situations that result in each type of report. It also discusses the auditor's responsibilities, including maintaining professional skepticism and ensuring financial statements are free from material misstatement. The types of audits are defined as external, internal, and compliance audits.

What's hot (20)

Malaysian Private Entities Reporting Standard (MPERS)

Malaysian Private Entities Reporting Standard (MPERS)

Corporate Reporting - MFRS116, IAS16 Property Plant and Equipment_PPE

Corporate Reporting - MFRS116, IAS16 Property Plant and Equipment_PPE

Foreign Currency Transactions and Financial Instruments

Foreign Currency Transactions and Financial Instruments

Konsep syarikat, konsep tirai perbadanan dan pengecualiannya, jenis-jenis sya...

Konsep syarikat, konsep tirai perbadanan dan pengecualiannya, jenis-jenis sya...

Evolution of budgeting system in malaysia (10 page)

Evolution of budgeting system in malaysia (10 page)

Similar to Tutorial 6 -_company_reconstruction_answer (1)

Assignment3 -a_ranswer

1. The document contains accounting journal entries for receivables and notes receivable. It addresses recognizing bad debt expense using percentage of receivables and gross sales methods, adjusting the allowance account, and discounting notes receivable.

2. Several journal entries are provided for World Wide Finance to record loan origination, interest revenue, and cash receipts.

3. Journal entries record various transactions for an account receivable from SilaHamza including sales, returns, discounting notes receivable, bad debt expense, and assigning receivables to a factor.

12 accountancy notes_ch08_company_accounts_issue_of_debentures_02

The document contains journal entries related to the issue of debentures by a company. It records the receipt of application money from debenture applicants, allotment of debentures, and issue of debentures at par as well as at a discount of 10%. It also contains a balance sheet showing the capital received from debentures as a non-current liability and the cash received as a current asset.

Operations management chapter: capacity management

The document discusses strategic capacity planning and management. It defines capacity and strategic capacity planning as determining overall capacity levels of facilities, equipment, and labor force. It discusses determining a best operating level to maximize output while minimizing costs. It also covers capacity utilization rate calculations, approaches to capacity expansion, determining capacity requirements, and using decision trees to evaluate capacity decisions. Short-term capacity options like overtime, additional shifts, and subcontracting are also summarized.

Financial Assets Management Kpi And Dashboard PowerPoint Presentation Slides

It has PPT slides covering wide range of topics showcasing all the core areas of your business needs. This complete deck focuses on Financial Assets Management Kpi And Dashboard Powerpoint Presentation Slides and consists of professionally designed templates with suitable graphics and appropriate content. This deck has total of twentyfive slides. Our designers have created customizable templates for your convenience. You can make the required changes in the templates like colour, text and font size. Other than this, content can be added or deleted from the slide as per the requirement. Get access to this professionally designed complete deck PPT presentation by clicking the download button below.

capital structure

This document discusses capital structure and various capital structure theories. It begins by defining capital structure and explaining that the objective is to maximize shareholder wealth through an optimal capital structure design. It then covers key considerations in capital structure planning like return, cost, risk and control. Several capital structure theories are explained - the Net Income Approach proposes higher debt increases value, while the Net Operating Income Approach says value is independent of structure. The Modigliani-Miller model supports the latter. The Traditional Approach finds an optimal structure where cost is minimum and value maximum. Formulas and an example are provided.

Management Of Inventories And Accounts Receivables Units 14 And 15

This document discusses various aspects of inventory and accounts receivable management. It defines key terms like economic ordering quantity (EOQ), reorder level, inventory turnover ratio, ABC analysis, and bill of materials. It provides formulas to calculate EOQ and discusses how to determine optimal inventory levels. Examples are given to illustrate calculation of EOQ, analysis of extending credit terms, and classification of inventories using ABC analysis. The document also briefly explains perpetual inventory systems and various committees that have made recommendations around working capital management in India.

Looking for venture capital on iron ore project

Our Client is an engineering, construction and project management company established under the laws of the Republic of Indonesia, established since July 30, 2013.

The main purpose is to provide alternative solutions in managing the turnkey project through delivering engineering, construction and project management team integrated in Client’s organization.

We provide the project management and engineering services throughout the 4 phases of the project life cycle from concept, development, implementations to close-out the Client’s larger, complex, and high risk projects.

working capital ch solution financial management ....mohsin mumtaz

The document discusses solutions to problems related to working capital and current asset management. It addresses topics such as cash conversion cycle, economic order quantity, accounts receivable management, and cash management techniques. The problems calculate financial metrics and evaluate strategies for reducing costs and improving profitability within the constraints of various assumptions provided in the questions.

lec. 2 leverage.pdf

This document summarizes a lecture on leverage, including:

1) Defining leverage and differentiating between operating and financial leverage.

2) Explaining how to calculate the degree of operating leverage and degree of financial leverage.

3) Providing examples to demonstrate how to calculate the degrees of leverage, showing that higher percentages of changes in sales or EBIT result in even higher percentages of changes in EBIT or earnings per share.

4) Noting that greater use of leverage increases business risk, as fixed costs must still be covered regardless of sales volume.

Ch12 bb

The document discusses different types of deposit accounts offered by banks, how banks determine their cost of funding deposits, and methods for pricing deposit services and interest rates on deposits. It examines transaction deposits used for payments versus nontransaction savings deposits, and how technology has impacted deposit account management. The document also explores how banks can ensure they have sufficient deposits to support lending while obtaining funds at the lowest possible cost.

Capital Structure Theories

Capital structure, Net Income approach, Net Operating approach, Modigliani – Miller Model, Traditional Approach

Chapter 14

This document contains solutions to 16 problems related to working capital and current asset management. The problems cover topics such as cash conversion cycle calculation and analysis, economic order quantity modeling, accounts receivable management, cash discounts, and float. For each problem, the relevant calculations and recommendations are shown. An ethics problem at the end questions the practice of banks locating controlled disbursement accounts in very distant locations from the client company.

Traditional theory of capital structure

The document discusses capital structure, which refers to the composition of a company's long-term capital from sources like loans, reserves, shares, and bonds. It also discusses capitalization, which is the total amount of securities issued, and financial structure, which includes all short-term and long-term financial resources. Different approaches to capital structure are described, including the net income approach, which argues the optimal structure is maximum debt financing to reduce costs. The net operating income approach argues structure does not impact value or costs. The traditional approach finds an optimal debt ratio that balances lower debt costs and higher equity costs.

CF 4.1 Capital Structure.pptx

The document discusses capital structure and various capital structure theories:

[1] Capital structure is the mix of long-term financing sources like debt and equity used by a company. It affects the company's risk and value.

[2] There are four main capital structure theories - Net Income Approach, Net Operating Income Approach, Modigliani-Miller Approach, and Traditional Approach. The Traditional Approach suggests an optimal capital structure that maximizes value.

[3] The examples show how a company's value and cost of capital are affected by the debt-equity mix under the different approaches. The optimal mix lowers risk and cost of capital, but excessive debt has the opposite effect.

Running Head FINANCIAL AND OPERATIONAL RISK5F.docx

Running Head: FINANCIAL AND OPERATIONAL RISK 5

Financial and Operational Risk

Rasmussen College

Amanda McCauley

Author Note

This paper is being submitted on January 22, 2017 for William Tipton’s ACG3205 Risk Management for Accountants course.

Module 3 Course Project

Risk Area

Level of Risk

Strategy (Assume, Mitigate, or Transfer)

Medical Errors

High

Medical errors includes wrong dosage, deaths of patients due to poor handling or treatment as well as using wrong method of treating patients that lead to another medical conditions (Highland Risk Services, 2014). The medical errors cannot be mitigated by ensuring that error made by personnel is reduced. It entail employing competent personnel in the healthcare facilities.

Board Composition

Low

The composition of the Board matters since they help to over the operations of the organizations. Therefore, the composition should have personnel from other related industries to help make multi-disciplinary decisions (Sullivan, 2013). Therefore, the risk can be transferred by selecting a competent and qualified board.

Transportation- shortage of ambulances and other emergency vehicles

High

Transportation is cornerstone of the healthcare facilities as it can be a life saver. Therefore, the risks of shortage of emergency vehicles like ambulance should be mitigated as soon as possible to avoid deaths of patients caused by lack of transportations (Sullivan, 2013). Therefore, the strategy would be to mitigate it by buying or leasing enough vehicles for any emergency purposes.

High Inflation Rate

High

Health care facilities are expected to deliver health services regardless of the cost. The norm makes health care services to have high expenses that might outweigh the revenue (Highland Risk Services, 2014). The risk can be transferred by ensuring that there is sufficient revenue from patients, services, grants and donors.

References

Highland Risk Services. (2014). Risk Management for Healthcare Clinics. Retrieved from Highland Risk Services: http://www.highlandrisk.com/index.php?option=com_content&view=article&id=74:risk-management-for-healthcare-clinics&catid=7&Itemid=223

Sullivan, M. (2013). The Top Five Challenges Facing Today’s Hospitals. Retrieved from http://blog.schneider-electric.com/building-management/2013/10/17/top-five-challenges-facing-todays-hospitals/

Running Head: FINANCE

FINANCE 3

Financial Crisis

Walter Frazier

FIN 100

Professor Fatma Ahmad

January 22, 2017

Unfortunately, due to rapidly rising housing prices during the decade prior to 2006, many home buyers needed increasingly larger loans to make their real property purchases. For example, a $200,000 fixed-rate mortgage loan would result in a much higher monthly payment compared to a $100,000 loan. Rework the above financial calculator spread sheet solutions using a PV of – 200000. The resulting doubling of the monthly payment to $1,199.10 means that fewer potential home buyers could qualify for these ...

Business simulation final

The document provides a business report for the Dec. 1, 2012 General Shareholders Meeting of Alexander Islands. It summarizes the company's objectives to maximize cash inflows and minimize cash outflows. It analyzes revenue, costs, inventory levels, and sales and procurement strategies over 11 rounds. While surplus grew overall, inventory levels were too high and unstable demand led to losses in rounds 9 and 11 when inventories ran low. The company needs to better manage inventories and control costs like warehouse expenses to improve profits.

SOC-436 Topic 2 Power in America Worksheet Scoring Guide.docx

This document provides guidelines and a rubric for a final project in a finance course. The project involves conducting a financial analysis of Home Depot Inc. based on provided case study data. Students will analyze topics related to time value of money, stock valuation, bond valuation, and capital budgeting. The project is divided into four milestones to be submitted at various points in the course. Students must address critical elements for each topic, including calculating present and future values, dividend yields, and capital budgeting metrics. They will also discuss how macroeconomic variables may impact the company's financial decisions and strategic objectives. The analysis will demonstrate mastery of learning outcomes involving financial portfolio management, maximizing shareholder value, capital financing and budgeting

session 1

The document discusses cost reduction techniques. It covers topics like the benefits of cost reduction, the 6Ms of cost (machine, manpower, material, methods, money, space), why cost reduction is important at the operational level, and how cost reduction can impact profits. Workshops are proposed to teach tools like Ishikawa diagram and exercises are suggested to maximize utilization and reduce product costs. Feedback is collected at the end to evaluate the workshops.

Tutorial 4 eps_answer

This document contains calculations and explanations for determining basic and diluted earnings per share (EPS) for three questions.

For question 1, basic EPS is calculated as net income divided by weighted average shares outstanding.

Question 2 involves more steps to calculate basic and diluted EPS, accounting for additional shares from options, convertible bonds, and convertible preference shares. Diluted EPS is calculated by ranking the incremental EPS from each potential ordinary share instrument and accumulating the increases.

Question 3 also involves multiple steps to calculate basic and diluted EPS, considering ordinary shares, convertible preference shares, options, and convertible bonds. Diluted EPS is determined by accumulating the increases in earnings and shares from each instrument.

Equity part2

The document discusses issues related to share capital, including repurchases or buybacks of equity shares by a company. It explains two methods for accounting for share buybacks - the share retirement method and treasury share method. It also covers share dividends, share splits, share rights, and the statement of changes in equity. Several illustrations are provided to demonstrate journal entries for share buybacks and subsequent distributions of treasury shares under each method.

Similar to Tutorial 6 -_company_reconstruction_answer (1) (20)

12 accountancy notes_ch08_company_accounts_issue_of_debentures_02

12 accountancy notes_ch08_company_accounts_issue_of_debentures_02

Operations management chapter: capacity management

Operations management chapter: capacity management

Financial Assets Management Kpi And Dashboard PowerPoint Presentation Slides

Financial Assets Management Kpi And Dashboard PowerPoint Presentation Slides

Management Of Inventories And Accounts Receivables Units 14 And 15

Management Of Inventories And Accounts Receivables Units 14 And 15

working capital ch solution financial management ....mohsin mumtaz

working capital ch solution financial management ....mohsin mumtaz

Running Head FINANCIAL AND OPERATIONAL RISK5F.docx

Running Head FINANCIAL AND OPERATIONAL RISK5F.docx

SOC-436 Topic 2 Power in America Worksheet Scoring Guide.docx

SOC-436 Topic 2 Power in America Worksheet Scoring Guide.docx

More from kim rae KI

Bab 5

This document discusses segmentation and decentralization in organizations. It defines different types of responsibility centers such as cost centers, profit centers, and investment centers. It also discusses the benefits and disadvantages of decentralization. Additionally, it explains how to prepare segmented income statements using a contribution format by separating traceable fixed costs from common fixed costs. The document provides examples of how a company can segment its business by geographic regions or customer channels. It emphasizes that traceable costs of one segment can become common costs of another segment.

Bab 4

- Standards are benchmarks used to measure performance in managerial accounting. Quantity standards specify the input amounts, while price standards specify input costs.

- Direct material price and quantity variances are calculated to analyze differences between actual and standard costs. The price variance is the difference due to actual price paid, while the quantity variance is due to using more or less material than standard.

- An example calculates variances for a company that used 210kg of fiberfill costing $1,029 total to make 2,000 parkas. The $21 favorable price variance and $50 unfavorable quantity variance are determined.

Bab 2

This document provides an overview of budgeting and the budgeting process. It discusses why organizations create budgets, the basic framework of budgets including planning and control, and the advantages of budgeting such as defining goals and coordinating activities. The document also covers various types of budgets including operating budgets and continuous budgets. It discusses budgeting approaches like top-down versus bottom-up budgeting and incremental versus zero-based budgeting. Finally, it provides learning objectives about understanding basic budgeting terms and components of master budgets for different industries.

Bab 3

The document discusses flexible budgets and performance analysis. It provides examples to illustrate how to prepare flexible budgets that account for multiple activity levels, as well as calculate variances between flexible budgets and actual results. The key benefits of flexible budgets are that they allow for "apples-to-apples" comparisons of costs when actual activity differs from planned levels. Flexible budgets more accurately reveal whether variances are due to external factors like activity changes or controllable factors like poor cost management. The document outlines how to prepare flexible budgets, calculate variances, and analyze performance using these variance reports.

Bab 13

This document discusses segmentation and decentralization in organizations. It defines different types of responsibility centers such as cost centers, profit centers, and investment centers. It also discusses the benefits and disadvantages of decentralization. Additionally, it explains how to prepare segmented income statements using a contribution format by separating traceable fixed costs from common fixed costs. The document provides examples of how a company can segment its business by geographic regions or customer channels. It emphasizes that traceable costs of one segment can become common costs of another segment.

Bab 12

- Standards are benchmarks used to measure performance in managerial accounting. Quantity standards specify the input amounts, while price standards specify input costs.

- Direct material price and quantity variances are calculated to analyze differences between actual and standard costs. The price variance is the difference due to actual price paid, while the quantity variance is due to using more or less material than standard.

- An example calculates variances for a company that used 210kg of fiberfill costing $1,029 total to make 2,000 parkas. The $21 favorable price variance and $50 unfavorable quantity variance are determined.

Bab 11

This document outlines how to prepare flexible budgets that can be used to evaluate performance. It discusses the deficiencies of static budgets and how flexible budgets address them by adjusting for different activity levels. It provides an example of Larry's Lawn Service to demonstrate how to prepare a flexible budget with multiple cost drivers. Key steps include preparing flexible budgets, calculating activity variances between the static and flexible budgets, calculating revenue and spending variances between the flexible budget and actual results, and combining these variances into a single performance report. The document suggests flexible budgets can also be used for non-profits and cost centers.

Bab 10

This document provides an overview of budgeting concepts and processes. It discusses why organizations create budgets, the basic framework of budgets including planning and control, and the advantages of budgeting such as defining goals and allocating resources. It also covers budgeting terms and methods, including bottom-up versus top-down budgeting, incremental versus zero-based budgets, and the roles of management and budget committees. Finally, it discusses the key components of master budgets for different types of industries, including budgets for production, sales, materials, labor, and cash for manufacturing companies.

Bab 1 (p3)

This document discusses cost behavior analysis. It explains that costs can be variable, fixed, or mixed. Variable costs change proportionally with activity level, while fixed costs remain constant. Mixed costs have both fixed and variable components. The document provides examples like cell phone bills and utility costs to illustrate different types of costs. It also discusses using scattergraph plots to diagnose whether a cost is variable or fixed based on its behavior over different activity levels. The overall purpose is to understand how to classify and analyze costs to predict how they will change with activity.

Bab 1 (p2)

The document discusses managerial accounting concepts including the work of management (planning, controlling, directing and motivating), manufacturing costs (direct materials, direct labor, manufacturing overhead), and cost flows. It provides learning objectives on the differences between financial and managerial accounting, manufacturing cost categories, distinguishing product and period costs, and preparing income statements and schedules of manufacturing costs. Key points include defining direct materials, direct labor, manufacturing overhead, and period costs. Formulas are given for calculating cost of goods sold and manufacturing costs.

Bab 1 (p1)

This document contains slides from a McGraw-Hill textbook on managerial and cost accounting. It covers several topics:

- The definitions and roles of management accounting and cost accounting in helping companies make better decisions.

- Global trade trends from 1950-2009 showing increasing trade in manufactures and declines in fuels and agriculture.

- Regional shares of world exports in 2009 led by North America, Europe and Asia.

- The distribution of Fortune Global 500 companies by region from 2005-2010, with increases from China, India and Asia Pacific.

Equity part1

The document discusses various aspects of owners' equity, including:

- Owners' equity represents the investment made by owners in a business.

- Statements of owners' equity track the capital contributed and any profits/losses of a business over time.

- Different types of business organizations (sole proprietorships, partnerships, companies) have different structures for owners' equity and liability.

- Companies establish authorized, issued, and paid-up share capital through the issuance of ordinary and preference shares. Reserves are also part of owners' equity.

Current liabilities ppt

This document discusses current liabilities, provisions, and contingencies. It begins by outlining the learning objectives, which are to describe various types of current liabilities, explain classification issues related to short-term debt expected to be refinanced, identify types of employee-related liabilities, explain accounting for provisions, and identify criteria for contingent liabilities and assets. It then defines key terms like liability, current liability, and contingencies. Specific types of current liabilities are explained, such as accounts payable, notes payable, current maturities of long-term debt, and unearned revenue. The accounting treatment and examples of these items are provided.

Chapter4

This document discusses the characteristics and accounting treatment of short term investments. Short term investments must be capable of prompt liquidation and there must be management intent to convert them to cash within one year. They include equity and debt securities carried at cost or at the lower of cost or market value. Gains or losses from sales and reclassifications are recognized in income. Disclosure in financial statements includes policies, income amounts, and market values of investments carried at cost.

Chapter3

The document discusses inventory valuation methods, including:

1) Perpetual and periodic inventory systems, with the perpetual system providing continuous inventory records and the periodic system using physical counts.

2) Cost flow assumptions like FIFO, average cost, and specific identification, which can impact ending inventory balances and cost of goods sold.

3) Effects of inventory errors, which may misstate the financial statements in a given year but offset in later years.

4) Items included in inventory costs, such as product costs directly connected to goods, and treatment of purchase discounts.

Chapter2 receivable edited2013

The document discusses accounts receivable and notes receivable. It defines receivables as amounts due from individuals and companies. It identifies the main types of receivables as accounts receivable, notes receivable, and other receivables. It then covers accounting issues related to recognition, valuation, and estimation of uncollectibles for accounts receivable. Finally, it discusses the processes of assigning or factoring accounts receivable, including examples of journal entries for assigning receivables as collateral for a loan.

Sqqs1013 ch6-a122

The document discusses population distributions, sampling distributions, and key concepts related to sampling. Some main points:

- A population distribution shows the probability of each possible value in the entire population. A sampling distribution shows the probability of getting each sample statistic value, such as the mean, from random samples of a given size.

- The mean of the sampling distribution of the sample mean is always equal to the population mean. The standard deviation of the sampling distribution decreases as sample size increases.

- For large samples from a normally distributed population, the sampling distribution of the mean will be normally distributed. For large samples from non-normal populations, the central limit theorem implies the sampling distribution will be approximately normal.

-

Sqqs1013 ch5-a122

This document discusses discrete probability distributions, specifically the binomial and Poisson distributions. It provides information on calculating probabilities using the binomial and Poisson probability formulas and tables. It defines key characteristics of binomial experiments and conditions for applying the binomial and Poisson distributions. Examples are given to demonstrate calculating probabilities for each distribution, including finding the mean, variance and standard deviation for binomial distributions.

Sqqs1013 ch4-a112

The document provides information about discrete and continuous random variables:

- It defines discrete and continuous random variables and gives examples of each. A discrete random variable can take countable values while a continuous random variable can take any value in an interval.

- It discusses probability distributions for discrete random variables, including defining the probability distribution and giving examples of how to construct probability distributions from data in tables. It also covers concepts like mean, standard deviation, and cumulative distribution functions.

- Various examples are provided to illustrate how to calculate probabilities, means, standard deviations, and construct probability distributions and cumulative distribution functions from data about discrete random variables. Continuous random variables are also briefly introduced.

Sqqs1013 ch3-a112

The document provides an introduction to probability concepts including:

1) Definitions of probability, sample space, outcomes, events, and interpretations of probability including classical, empirical, and subjective.

2) Examples of sample spaces for experiments like coin tosses and dice rolls.

3) Explanations of tree diagrams, Venn diagrams, and the addition rules for determining probabilities of mutually exclusive and non-mutually exclusive events.

4) Descriptions of joint, marginal, and conditional probabilities and examples of calculating each from contingency tables.

More from kim rae KI (20)

Recently uploaded

Community pharmacy- Social and preventive pharmacy UNIT 5

Covered community pharmacy topic of the subject Social and preventive pharmacy for Diploma and Bachelor of pharmacy

Pollock and Snow "DEIA in the Scholarly Landscape, Session One: Setting Expec...

Pollock and Snow "DEIA in the Scholarly Landscape, Session One: Setting Expec...National Information Standards Organization (NISO)

This presentation was provided by Steph Pollock of The American Psychological Association’s Journals Program, and Damita Snow, of The American Society of Civil Engineers (ASCE), for the initial session of NISO's 2024 Training Series "DEIA in the Scholarly Landscape." Session One: 'Setting Expectations: a DEIA Primer,' was held June 6, 2024.PCOS corelations and management through Ayurveda.

This presentation includes basic of PCOS their pathology and treatment and also Ayurveda correlation of PCOS and Ayurvedic line of treatment mentioned in classics.

Executive Directors Chat Leveraging AI for Diversity, Equity, and Inclusion

Let’s explore the intersection of technology and equity in the final session of our DEI series. Discover how AI tools, like ChatGPT, can be used to support and enhance your nonprofit's DEI initiatives. Participants will gain insights into practical AI applications and get tips for leveraging technology to advance their DEI goals.

Digital Artifact 1 - 10VCD Environments Unit

Digital Artifact 1 - 10VCD Environments Unit - NGV Pavilion Concept Design

Main Java[All of the Base Concepts}.docx

This is part 1 of my Java Learning Journey. This Contains Custom methods, classes, constructors, packages, multithreading , try- catch block, finally block and more.

The History of Stoke Newington Street Names

Presented at the Stoke Newington Literary Festival on 9th June 2024

www.StokeNewingtonHistory.com

How to Manage Your Lost Opportunities in Odoo 17 CRM

Odoo 17 CRM allows us to track why we lose sales opportunities with "Lost Reasons." This helps analyze our sales process and identify areas for improvement. Here's how to configure lost reasons in Odoo 17 CRM

How to Setup Warehouse & Location in Odoo 17 Inventory

In this slide, we'll explore how to set up warehouses and locations in Odoo 17 Inventory. This will help us manage our stock effectively, track inventory levels, and streamline warehouse operations.

LAND USE LAND COVER AND NDVI OF MIRZAPUR DISTRICT, UP

This Dissertation explores the particular circumstances of Mirzapur, a region located in the

core of India. Mirzapur, with its varied terrains and abundant biodiversity, offers an optimal

environment for investigating the changes in vegetation cover dynamics. Our study utilizes

advanced technologies such as GIS (Geographic Information Systems) and Remote sensing to

analyze the transformations that have taken place over the course of a decade.

The complex relationship between human activities and the environment has been the focus

of extensive research and worry. As the global community grapples with swift urbanization,

population expansion, and economic progress, the effects on natural ecosystems are becoming

more evident. A crucial element of this impact is the alteration of vegetation cover, which plays a

significant role in maintaining the ecological equilibrium of our planet.Land serves as the foundation for all human activities and provides the necessary materials for

these activities. As the most crucial natural resource, its utilization by humans results in different

'Land uses,' which are determined by both human activities and the physical characteristics of the

land.

The utilization of land is impacted by human needs and environmental factors. In countries

like India, rapid population growth and the emphasis on extensive resource exploitation can lead

to significant land degradation, adversely affecting the region's land cover.

Therefore, human intervention has significantly influenced land use patterns over many

centuries, evolving its structure over time and space. In the present era, these changes have

accelerated due to factors such as agriculture and urbanization. Information regarding land use and

cover is essential for various planning and management tasks related to the Earth's surface,

providing crucial environmental data for scientific, resource management, policy purposes, and

diverse human activities.

Accurate understanding of land use and cover is imperative for the development planning

of any area. Consequently, a wide range of professionals, including earth system scientists, land

and water managers, and urban planners, are interested in obtaining data on land use and cover

changes, conversion trends, and other related patterns. The spatial dimensions of land use and

cover support policymakers and scientists in making well-informed decisions, as alterations in

these patterns indicate shifts in economic and social conditions. Monitoring such changes with the

help of Advanced technologies like Remote Sensing and Geographic Information Systems is

crucial for coordinated efforts across different administrative levels. Advanced technologies like

Remote Sensing and Geographic Information Systems

9

Changes in vegetation cover refer to variations in the distribution, composition, and overall

structure of plant communities across different temporal and spatial scales. These changes can

occur natural.

The simplified electron and muon model, Oscillating Spacetime: The Foundation...

Discover the Simplified Electron and Muon Model: A New Wave-Based Approach to Understanding Particles delves into a groundbreaking theory that presents electrons and muons as rotating soliton waves within oscillating spacetime. Geared towards students, researchers, and science buffs, this book breaks down complex ideas into simple explanations. It covers topics such as electron waves, temporal dynamics, and the implications of this model on particle physics. With clear illustrations and easy-to-follow explanations, readers will gain a new outlook on the universe's fundamental nature.

Azure Interview Questions and Answers PDF By ScholarHat

Azure Interview Questions and Answers PDF By ScholarHat

Chapter 4 - Islamic Financial Institutions in Malaysia.pptx

Chapter 4 - Islamic Financial Institutions in Malaysia.pptxMohd Adib Abd Muin, Senior Lecturer at Universiti Utara Malaysia

This slide is special for master students (MIBS & MIFB) in UUM. Also useful for readers who are interested in the topic of contemporary Islamic banking.

Recently uploaded (20)

Digital Artefact 1 - Tiny Home Environmental Design

Digital Artefact 1 - Tiny Home Environmental Design

Community pharmacy- Social and preventive pharmacy UNIT 5

Community pharmacy- Social and preventive pharmacy UNIT 5

Pollock and Snow "DEIA in the Scholarly Landscape, Session One: Setting Expec...

Pollock and Snow "DEIA in the Scholarly Landscape, Session One: Setting Expec...

Executive Directors Chat Leveraging AI for Diversity, Equity, and Inclusion

Executive Directors Chat Leveraging AI for Diversity, Equity, and Inclusion

How to Manage Your Lost Opportunities in Odoo 17 CRM

How to Manage Your Lost Opportunities in Odoo 17 CRM

How to Setup Warehouse & Location in Odoo 17 Inventory

How to Setup Warehouse & Location in Odoo 17 Inventory

LAND USE LAND COVER AND NDVI OF MIRZAPUR DISTRICT, UP

LAND USE LAND COVER AND NDVI OF MIRZAPUR DISTRICT, UP

The simplified electron and muon model, Oscillating Spacetime: The Foundation...

The simplified electron and muon model, Oscillating Spacetime: The Foundation...

Azure Interview Questions and Answers PDF By ScholarHat

Azure Interview Questions and Answers PDF By ScholarHat

Chapter 4 - Islamic Financial Institutions in Malaysia.pptx

Chapter 4 - Islamic Financial Institutions in Malaysia.pptx

Tutorial 6 -_company_reconstruction_answer (1)

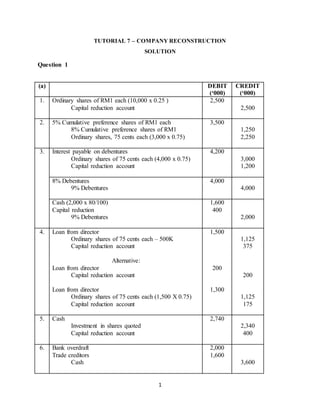

- 1. 1 TUTORIAL 7 – COMPANY RECONSTRUCTION SOLUTION Question 1 (a) DEBIT (‘000) CREDIT (‘000) 1. Ordinary shares of RM1 each (10,000 x 0.25 ) Capital reduction account 2,500 2,500 2. 5% Cumulative preference shares of RM1 each 8% Cumulative preference shares of RM1 Ordinary shares, 75 cents each (3,000 x 0.75) 3,500 1,250 2,250 3. Interest payable on debentures Ordinary shares of 75 cents each (4,000 x 0.75) Capital reduction account 4,200 3,000 1,200 8% Debentures 9% Debentures 4,000 4,000 Cash (2,000 x 80/100) Capital reduction 9% Debentures 1,600 400 2,000 4. Loan from director Ordinary shares of 75 cents each – 500K Capital reduction account Alternative: Loan from director Capital reduction account Loan from director Ordinary shares of 75 cents each (1,500 X 0.75) Capital reduction account 1,500 200 1,300 1,125 375 200 1,125 175 5. Cash Investment in shares quoted Capital reduction account 2,740 2,340 400 6. Bank overdraft Trade creditors Cash 2,000 1,600 3,600

- 2. 2 7. Capital reduction account Debtors(3,540 x 10%) Retained earnings 3,744 354 3,390 8. Land Capital reduction account Building Equipment Inventories 1,500 620 800 820 500 9. Capital reduction account Cash 200 200 10. Reserve Capital Reduction 489 489 CR 400 2500 3744 1200 620 375 200 400 4964 4475 489 (b) FiZy Bhd Statement of Financial Position as at 31 December 2013 RM'000 Assets Non Current Assets Land 7,000 Building (net) 2,560 Equipment (net) 2,000 11,560 Current Assets Inventory 7,500 Trade receivables 3,186 Cash 540 11,226 Total Assets 22,786 Liabilities And Equity Current Liabilities Trade Creditors 1,200 Non Current Liabilities 9% Debentures 6,000 Total Liabilities 7,200

- 3. 3 Equity Share capital Authorised, issued and fully paid: 18,500,000 Ordinary shares, RM0.75 each 13,875 8% RM1.00 Cumulative preference shares 1250 Reserve 461 Retained earnings - Total Equity 15,586 Total Liabilities and Equity 22,786 WORKINGS: OS CASH 2500 10000 2000 2250 1,600 1600 3000 2,740 200 1125 4,340 3800 16375 540 13875 c) Situation that allows company to reduce capital 1. To reduce or to write off the uncalled capital on its shares 2. To refund any surplus capital (in excess of need of the company) 3. To cancel paid up capital not represented by assets.

- 4. 4 QUESTION 2 a) RM’000 RM’000 1. Dr Ordinary Shares 57,000 Cr. Capital Reduction 57,000 (New par value - (150m-57mil)/150mil = RM0.62) Dr Capital Reduction 57,000 Cr. Accumulated loss 57,000 2. Dr. Creditors 12,500 Cr. Ordinary Shares 12,500 (1/4 x 50mill) Dr. Interest payable 50 Cr. Capital reduction 50 3. Dr. Cash 18,700 Cr. Equipment 17,000 Cr. Capital reduction ac -Gain on disp. 1,700 4. Dr. Convertible preference shares 4,000 Cr. Ordinary Shares 4,000 (8 milllion/2) 5. Dr. Redeemable preference shares 500 Cr. Cash 500 Dr. Cash 500 Cr. Ordinary Shares 500 6. Dr. Capital reduction ac - cost of cap. Reorg. 250 Cr. Cash 250 7. Dr. Cash 62.000 Cr. Ordinary shares 62,000 (100 mil X RM0.62) 8. Dr. Capital reduction ac - cost of cap. Reorg. 1,500 Cr. Reserves 1,500 (1,700 + 50 - 250)

- 5. 5 (b) Statement of Financial Position (post of the scheme) RM'000 2007 NON CURRENT ASSET Plant, properties and equipments(167,850-17,000) 150,850 CURRENT ASSET Cash and bank balances (42,386k+18.7mil+0.5mil- 0.5mil-250k+62mil) 122,836 Account receivables 57,879 Inventory 2,835 183,550 CURRENT LIABILITIES Trade creditors (85mil-12.5mil) 72,500 Interest payable (5.95mil-50k) 5,900 78,400 NET CURRENT ASSETS 105,150 NET TOTAL ASSETS 256,000 FINANCED BY: Share capital Authorized, issued and full paid: RM0.62 Ordinary shares 172,000 4% RM1.00 Convertible Preference Shares 4,000 7% RM1.00 Redeemable preference shares 0 176,000 Share premium 11,000 Reserves (8.5mill+1.5mill) 10,000 Beginning retained earnings 0 Current year net profit/(loss) 0 Shareholders’ fund 197,000 Long term loan 29,000 8% Bond payable 30,000 TOTAL EQUITY & LONG TERM LIABILITIES 256,000 Ordinary shares = 150mil-57mil+12.5mill+8mill+1mill+62mill Preference share = 8mill-4mill