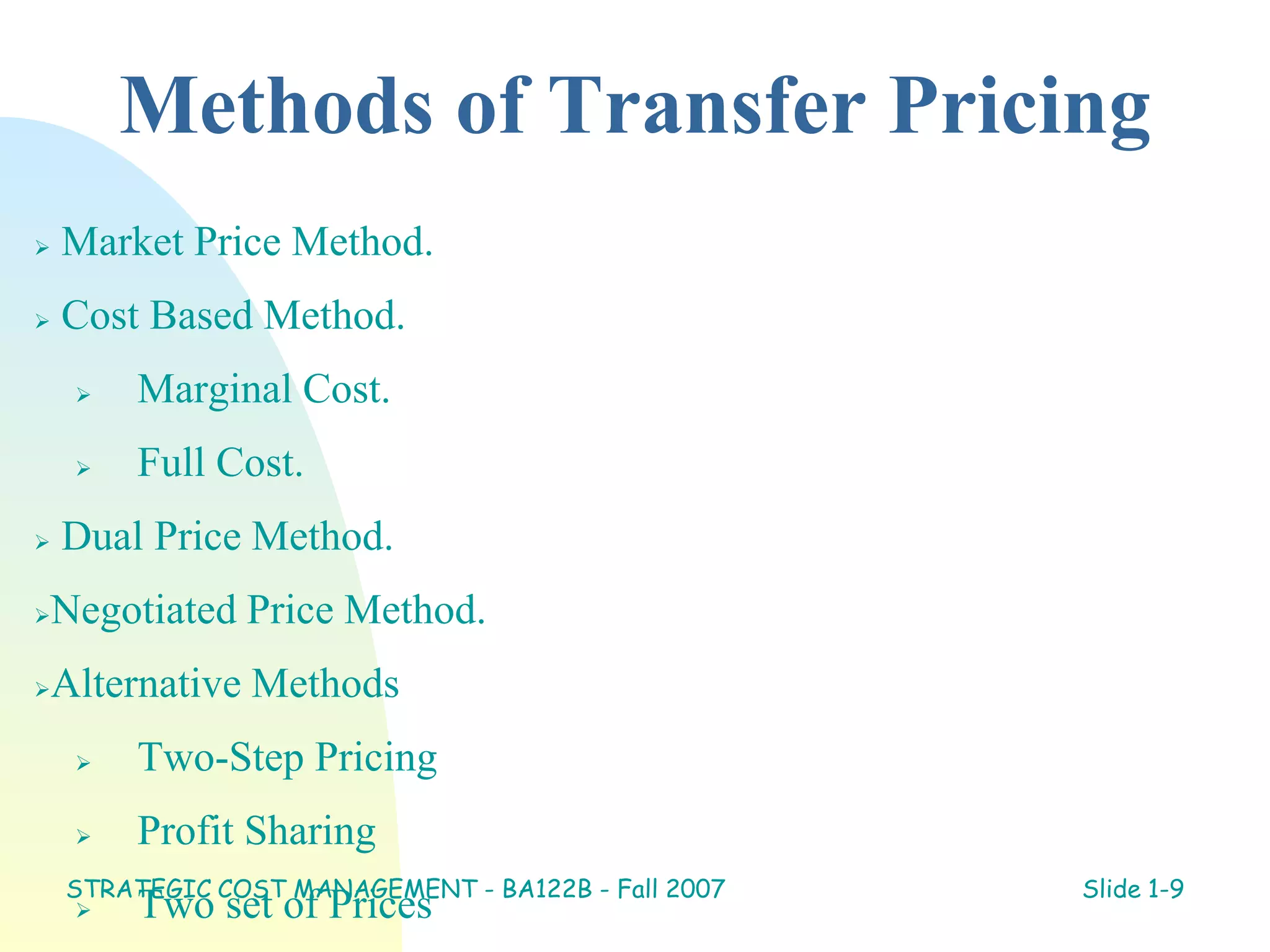

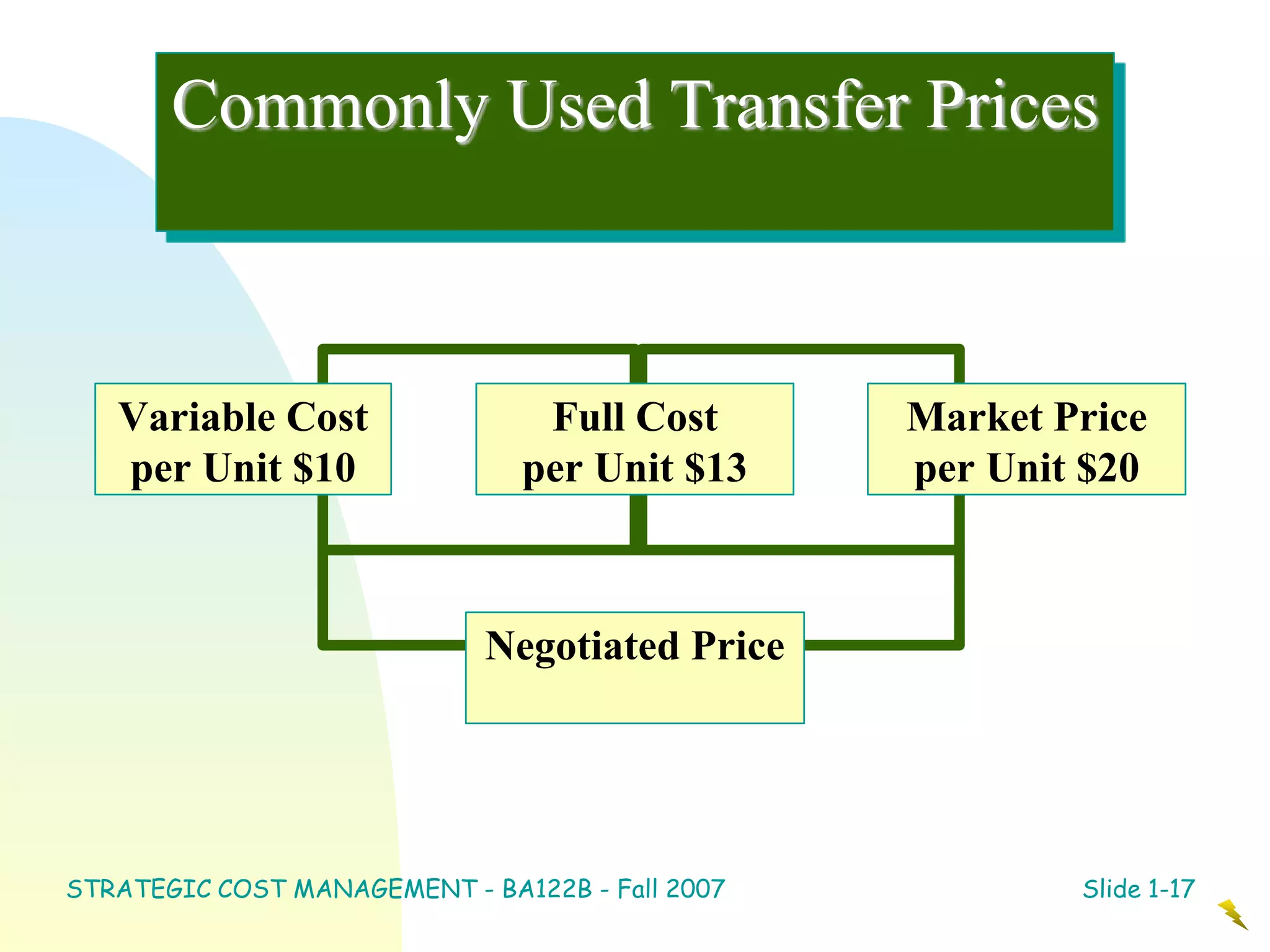

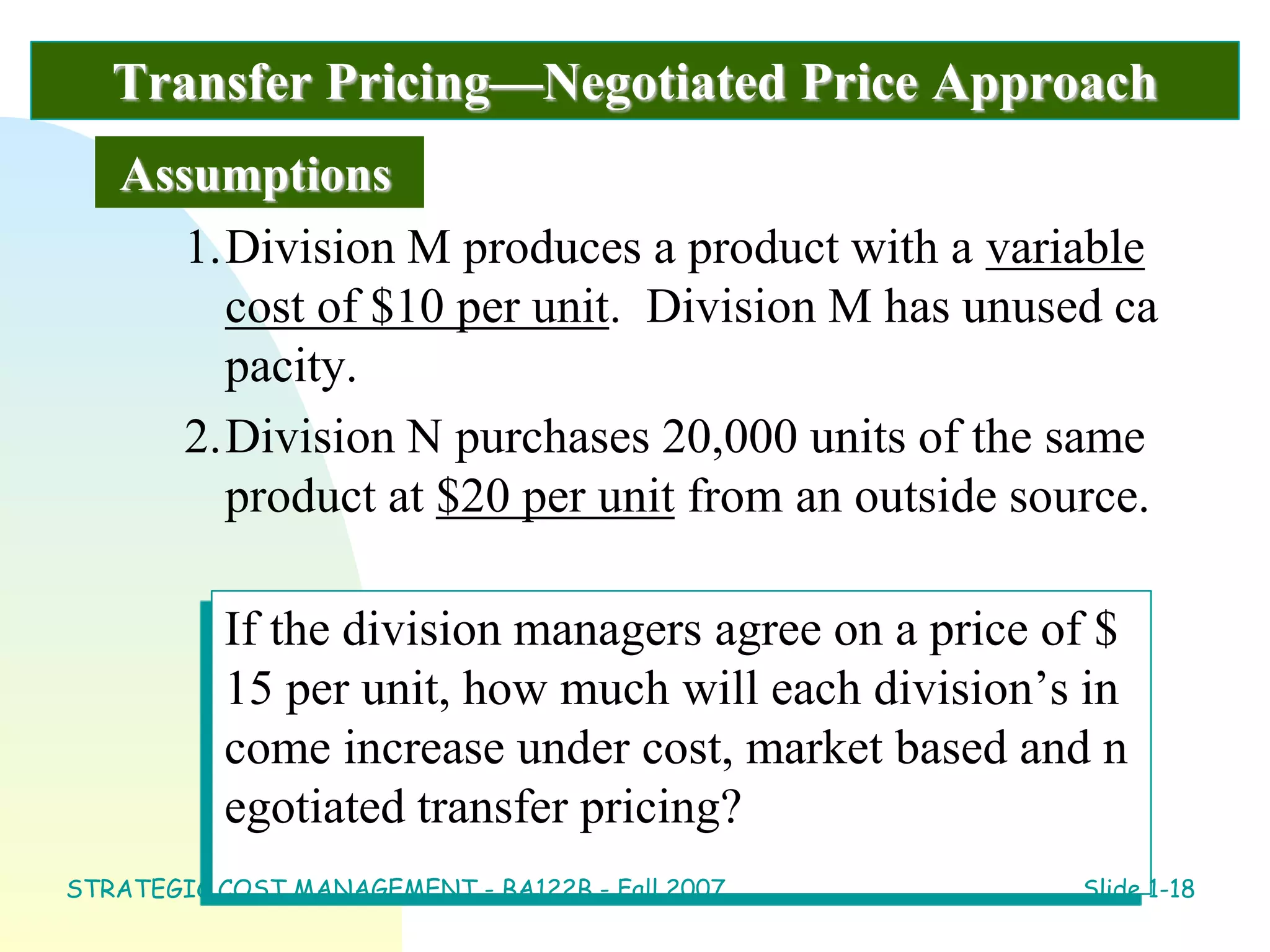

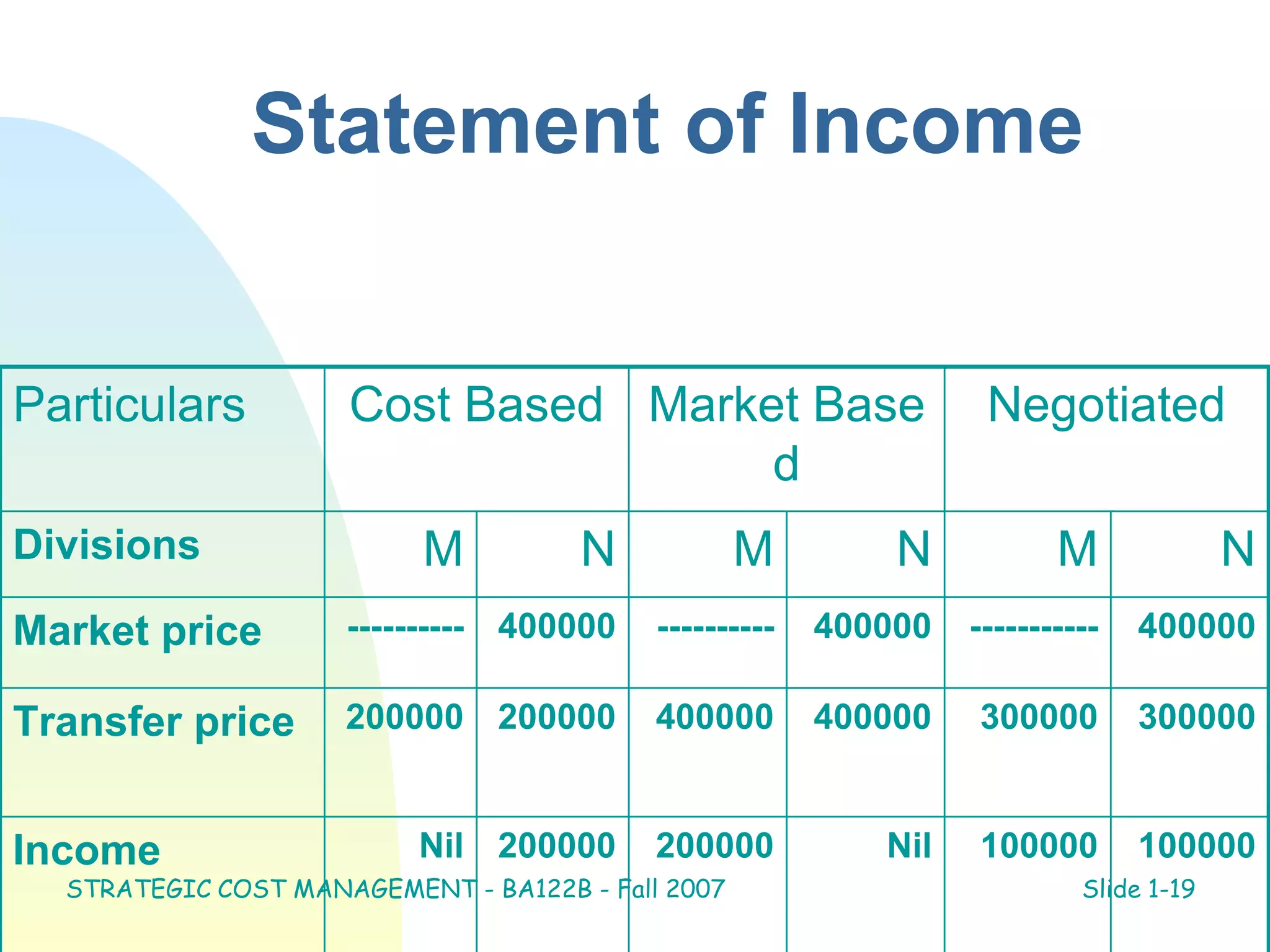

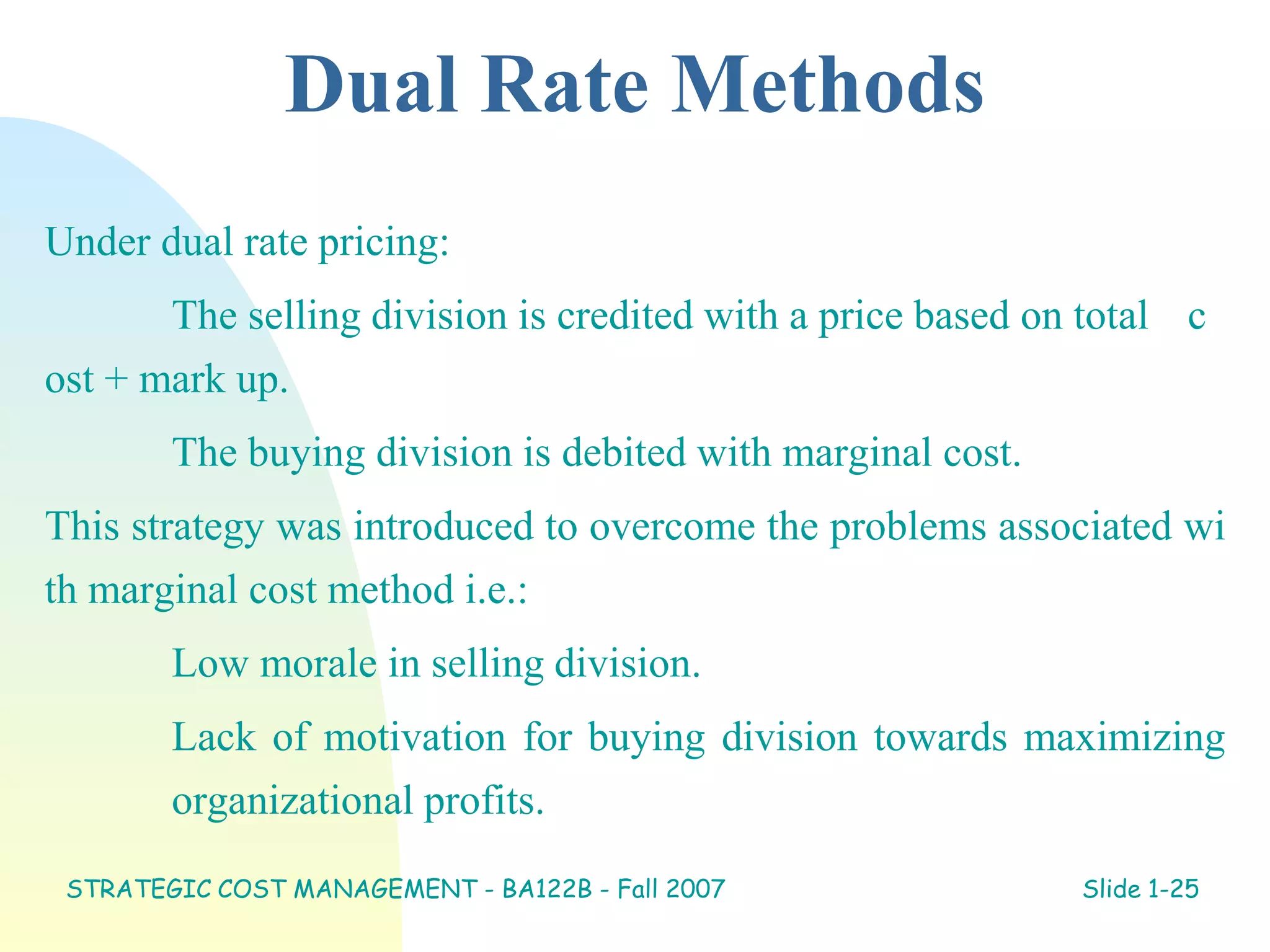

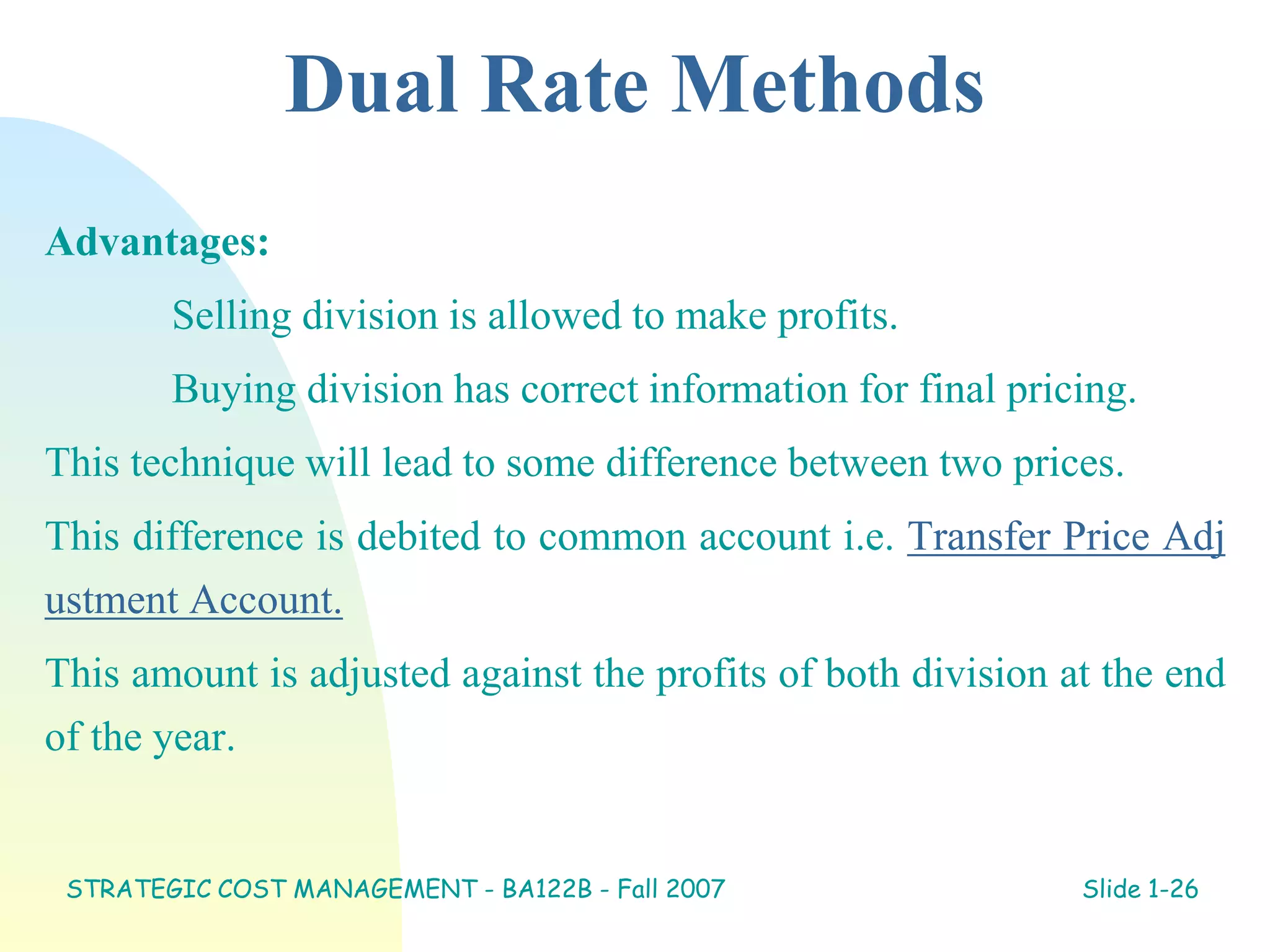

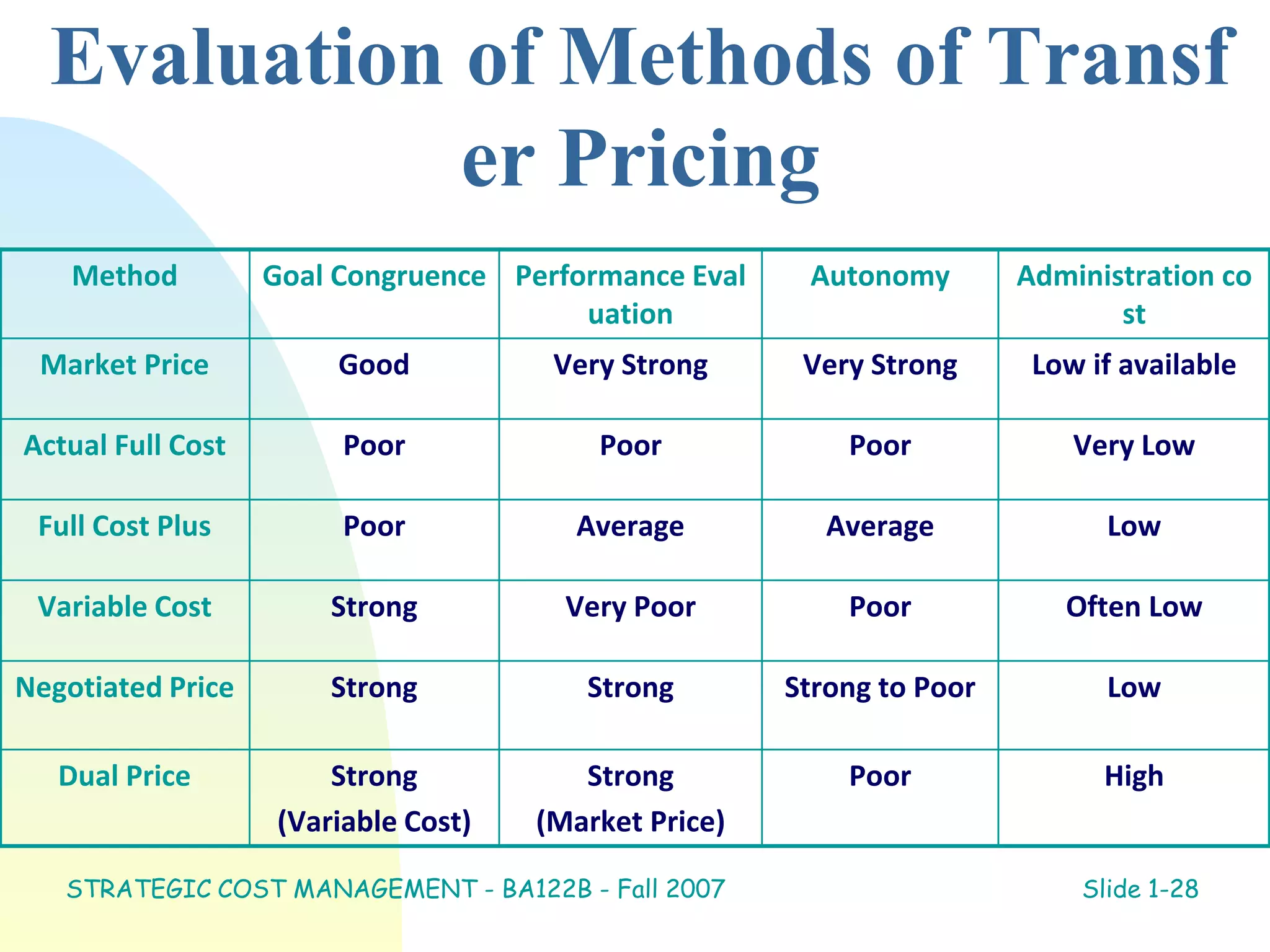

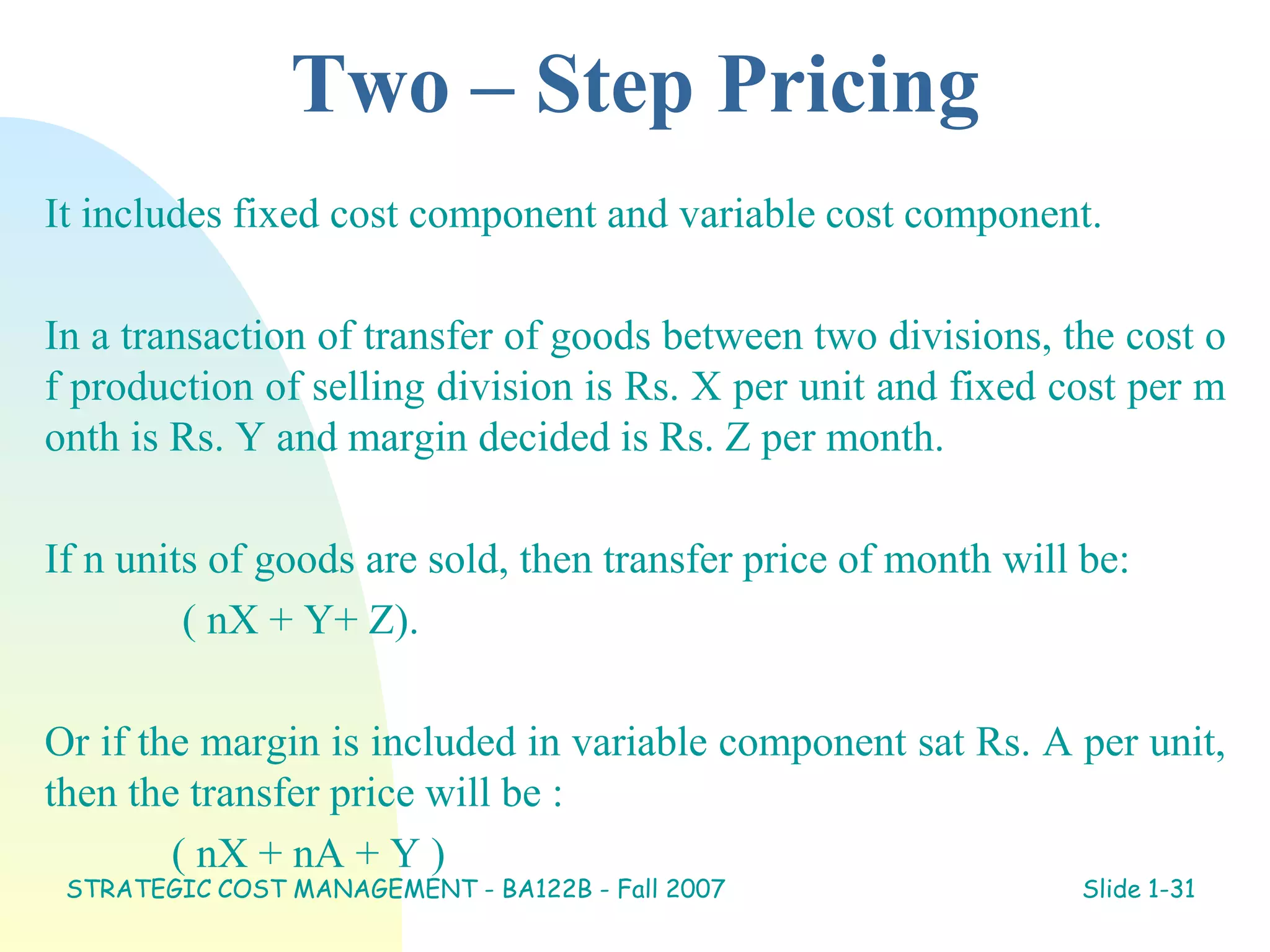

Transfer pricing refers to the pricing of goods and services transferred between divisions within a decentralized organization. The key objectives of transfer pricing are to encourage optimal cost-revenue tradeoffs, goal congruence between divisions and the overall company, and accurate measurement of divisional performance. Common transfer pricing methods include market price, cost-based methods like marginal cost and full cost, and negotiated prices. Proper administration of transfer prices includes clear communication of strategies, documentation, and establishing negotiation and conflict resolution procedures.

![Foreign exchange Risk [Autosaved].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/foreignexchangeriskautosaved-221217071434-1c7f0613-thumbnail.jpg?width=640&height=640&fit=bounds)