Downloaded 1,731 times

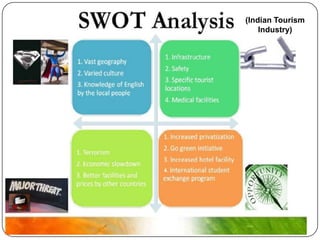

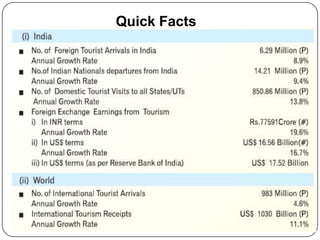

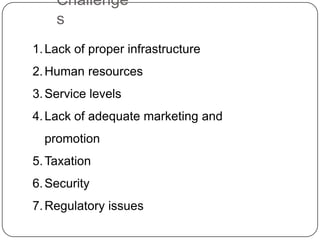

The document provides an analysis of the tourism industry in India. Some key points: - Tourism accounts for 6% of India's exports and 30% of exports in services, and is the 2nd fastest growing tourism economy. - India is poised to lead tourism growth in South Asia with 8.9 million expected arrivals by 2020. - Domestic tourism is emerging as a major segment as discretionary spending increases in India. - Challenges include lack of infrastructure, human resources, service quality issues, inadequate marketing and promotion, taxation, security, and regulatory hurdles.