Download to read offline

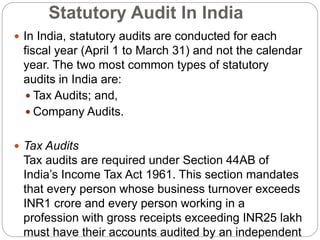

The document outlines the auditing process in India, distinguishing between statutory and internal audits, with statutory audits required for companies based on specific financial thresholds. It details the qualifications for auditors, the procedure for appointing them, and the responsibilities in preparing audit reports, emphasizing the importance of audits for businesses and investors. The document also discusses the advantages and limitations of auditing, highlighting factors that affect the audit's effectiveness.