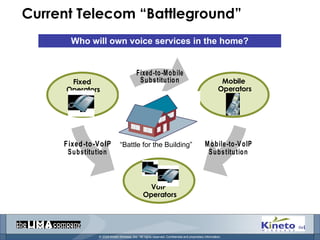

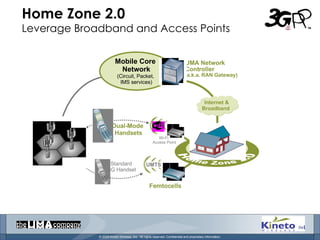

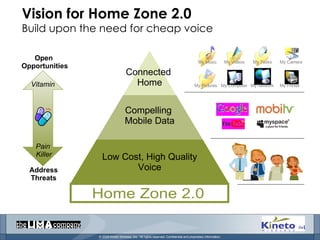

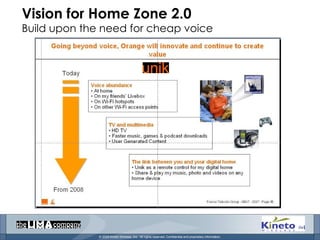

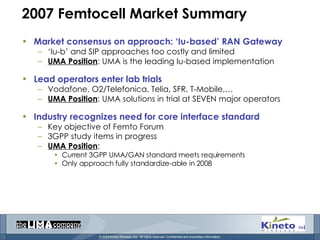

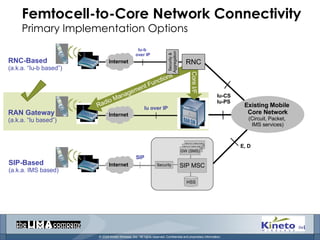

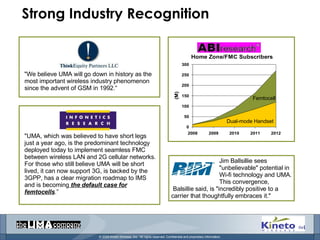

The document discusses the concept of "Home Zone 2.0" as a solution for mobile operators to own voice services in the home. It involves using low-power access points like femtocells and Wi-Fi to provide improved coverage and offload traffic. UMA is identified as the 3GPP standard that can enable Home Zone 2.0 by addressing challenges of earlier cellular-based approaches and leveraging broadband connectivity. Major mobile operators are expected to trial femtocell solutions in 2008 and UMA dual-mode handsets are gaining widespread commercial availability.