Downloaded 94 times

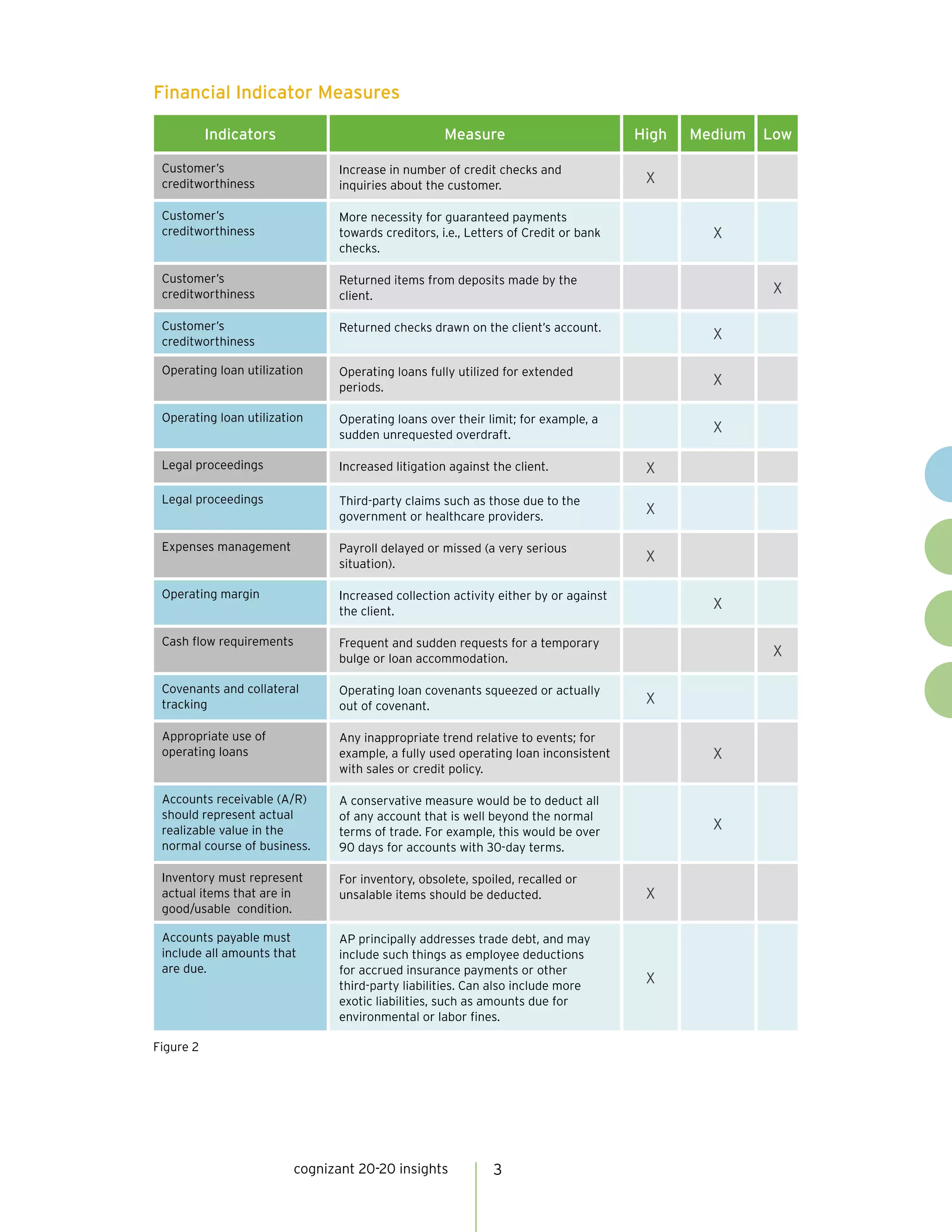

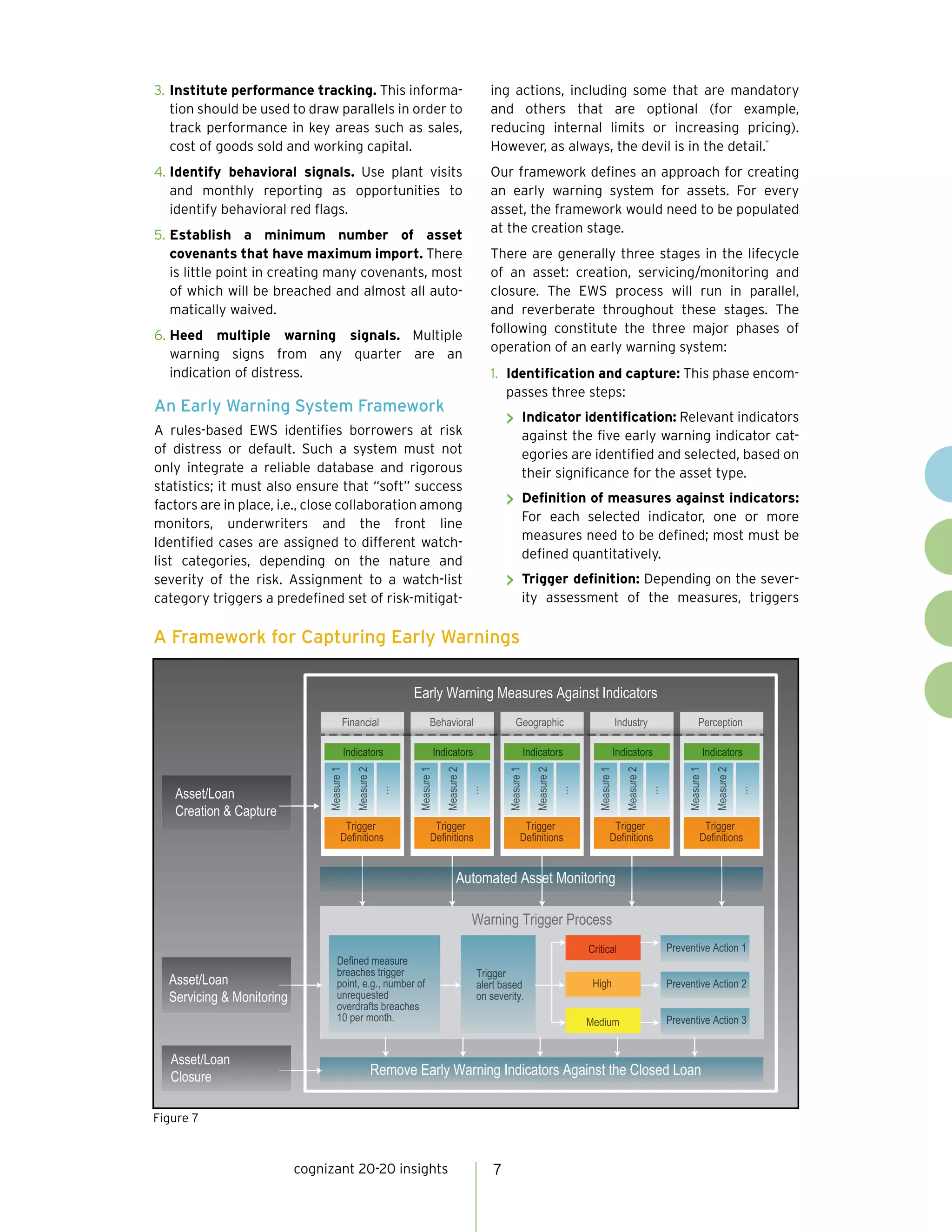

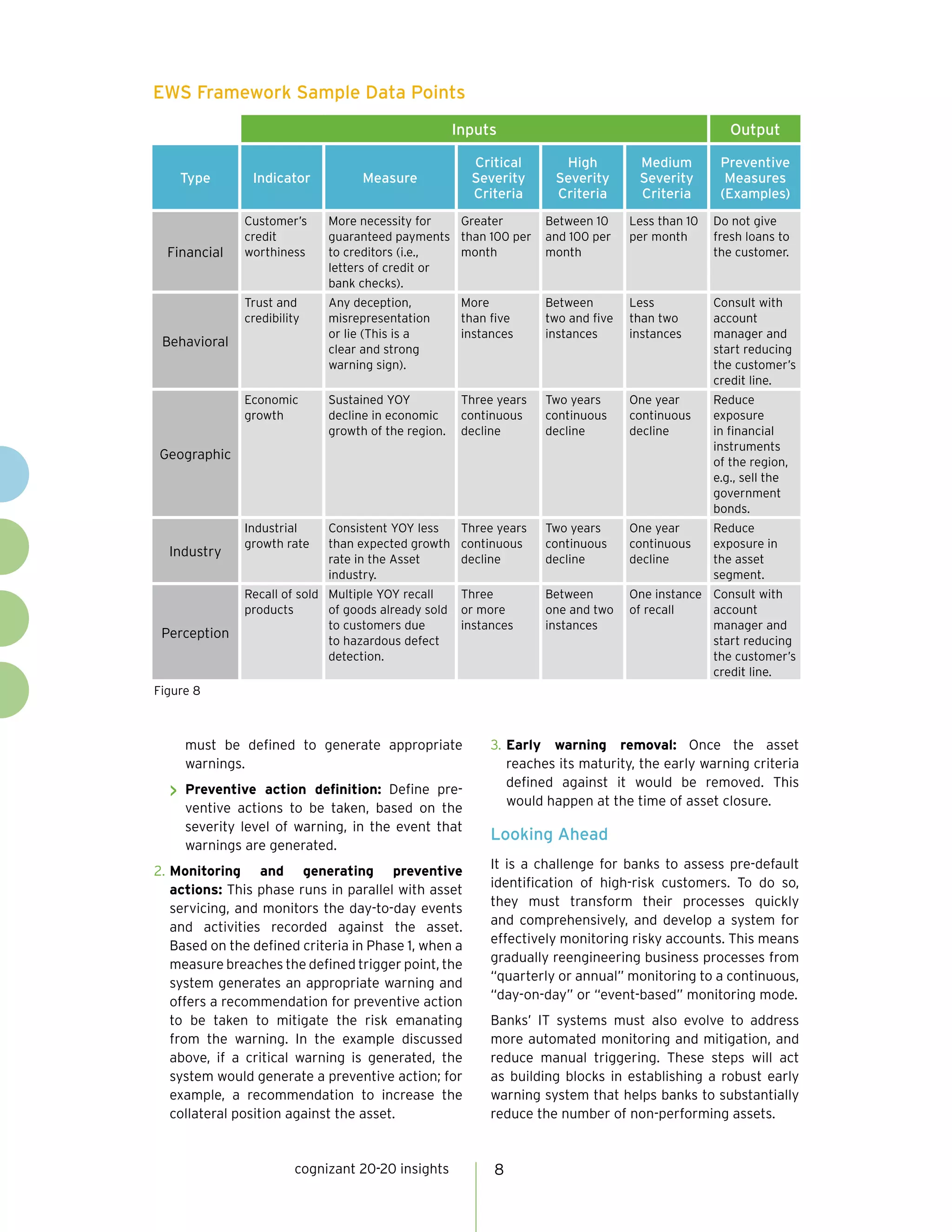

The document discusses the importance of an early warning system for banks to safeguard assets and reduce risks associated with non-performing loans. It identifies key warning indicators across financial, behavioral, geographic, industry, and perception categories, urging banks to adopt proactive monitoring practices. The paper outlines a framework for establishing such a system, emphasizing the need for continuous communication and performance tracking to identify potential risks early.