Downloaded 12 times

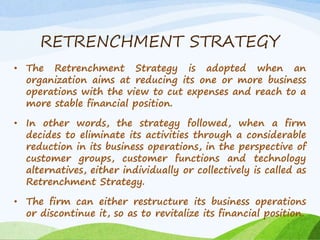

This document discusses various retrenchment strategies that a company can adopt when it aims to reduce business operations and expenses to reach a more stable financial position. It describes turnaround, dis-investment, and liquidation strategies. Turnaround strategy aims to convert a loss-making unit into a profitable one by cutting expenses and unproductive activities. Dis-investment strategy involves selling off business units that are underperforming. Liquidation strategy is the extreme case where a company decides to sell its entire business operations. The document provides reasons for and processes of implementing each retrenchment strategy through case studies.