Download as PDF, PPTX

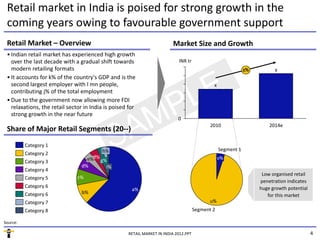

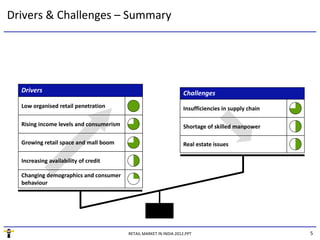

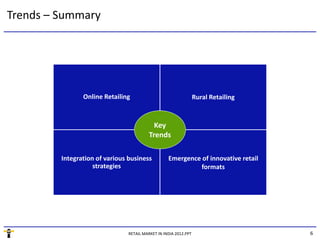

The retail market in India was valued at INR a trillion in 20-- and is projected to grow significantly due to low organized retail penetration and rising consumer income levels. Key trends include the rise of online and rural retailing, innovative formats, and the relaxation of FDI policies. The sector faces challenges including supply chain inefficiencies and real estate issues, but remains a critical part of the economy, employing millions and contributing substantially to GDP.