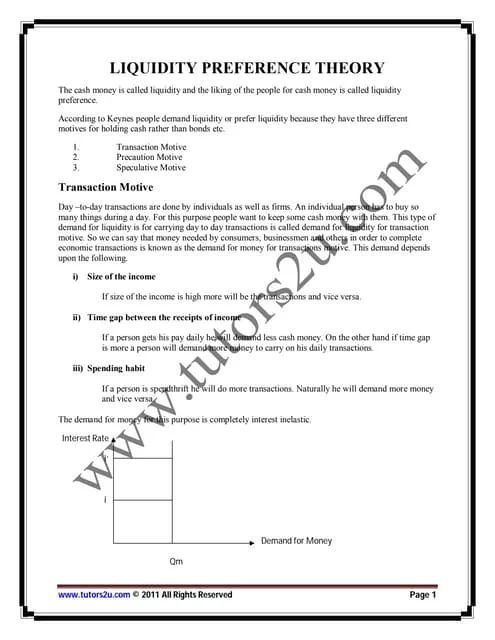

Downloaded 66 times

Inflation can be defined as a general rise in price levels and a fall in the value of money. It occurs when the amount of buying power exceeds the output of goods and services or when the money supply exceeds available goods and services. Inflation is normally measured as a percentage increase in price indexes like the Consumer Price Index or Producer Price Index over a set period of time, usually yearly. Governments have several policy options for controlling inflation including tightening the money supply through monetary policy tools or reducing private and public spending through fiscal policy like tax increases.

![Impact on profession and preparation for tomorrow cs ca nirc_22_nov[1]](https://cdn.slidesharecdn.com/ss_thumbnails/impactonprofessionandpreparationfortomorrowcscanirc22nov1-120117050529-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![What is Inflation? [Examining the PPI, CPI, and PCE Indices]](https://cdn.slidesharecdn.com/ss_thumbnails/inflationcpimonetaryandcostpushinflation2-250524044427-996efc14-thumbnail.jpg?width=640&height=640&fit=bounds)