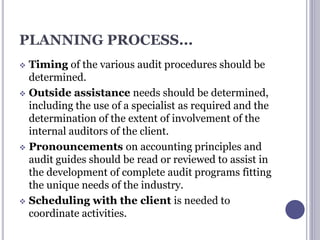

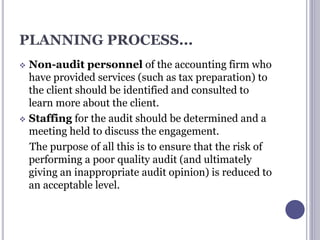

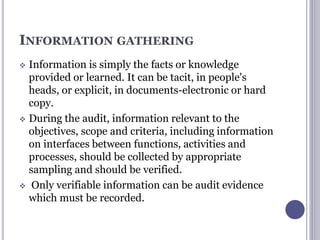

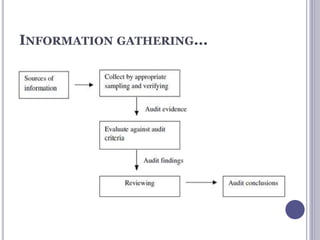

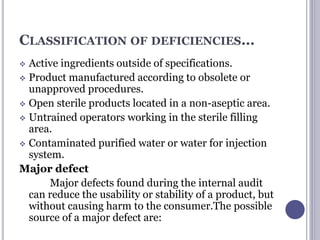

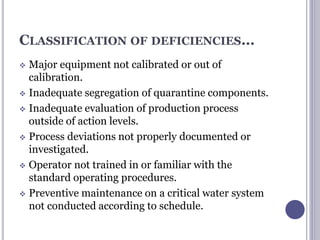

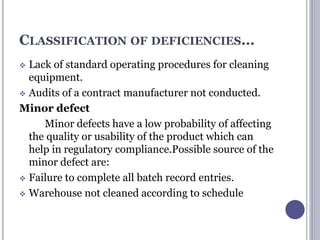

The document outlines the structure and significance of pharmaceutical quality audits, emphasizing their role in ensuring compliance with quality management system standards like ISO 9001. It details various types of audits including internal, external, and regulatory audits, along with their objectives, planning processes, and methods for gathering information. Additionally, responsibilities of auditors and management are discussed, highlighting the importance of effective communication and collaboration among stakeholders.

![TYPES OF AUDITS

Quality audits are performed to verify the

effectiveness of a quality management system. The

quality audit system mainly classified in three

different categories:

1.Internal Audits

2.External Audits

3.Regulatory Audits

Regulatory authority for quality audits:

ISO standards ,

Code of federal regulations [CFR] ,

ICH Q10,USFDA ,GMP](https://image.slidesharecdn.com/auditing-200207173952/85/Quality-Audit-in-pharmaceutical-industry-6-320.jpg)

![REFERENCE

1.Review on“Pharmaceutical quality audits” by princy

agarwal & amul misra , Nnovare;2018.

2. Vedanabhlata S, Gupta VN. “A review on audits and

compliance management”. Asian J Pharm Clin Res

2013;6:43-5.

3. Kaur J. Quality audit: Introduction, types and

procedure [Internet].Pharma Pathway; 2017.

http://pharmapathway.com/quality-audit-

introduction- types-and-procedure/.

4.Chartered Institute of Internal Auditors. How to

gather and evaluate information;2017.

https://www.iia.org.uk/resources/delivering-

internal-audit/how-/.](https://image.slidesharecdn.com/auditing-200207173952/85/Quality-Audit-in-pharmaceutical-industry-51-320.jpg)