This document provides an overview of management audits, including:

1. It defines management audit as a systematic examination and appraisal of management's overall performance, including examining organizational structure, plans, policies, operations, controls, facilities, and human resources.

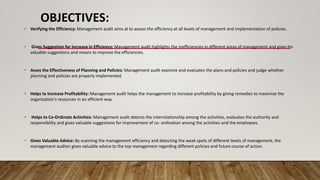

2. The objectives of a management audit are to verify efficiency, suggest improvements to increase efficiency, assess effectiveness of planning and policies, and help increase profitability.

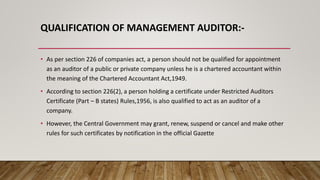

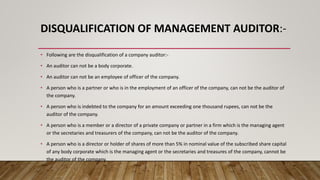

3. A management auditor must be a chartered accountant qualified under the Chartered Accountants Act of 1949 and cannot be employed by or indebted to the company being audited.