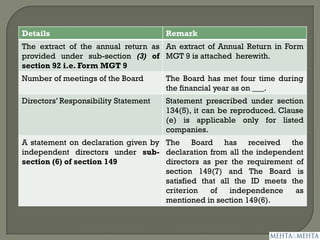

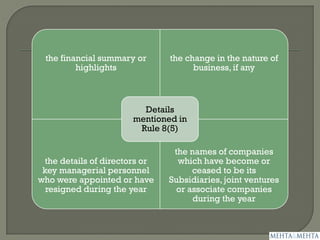

![ To be prepared based on stand alone financial

statement of the company [Rule 8(1) of the

Companies Accounts Rules, 2014];

Contain a separate section on report on the

performance and financial position of each of the

subsidiaries, associates and joint venture companies

[Rule 8(1) of the Companies Accounts Rules, 2014];

Signed by Chairperson, if authorized else by two

directors, one of them should be MD, if there is one

[Section 134 (6)];

Penalty [Section 134 (8)];](https://image.slidesharecdn.com/boardreport-150209220120-conversion-gate02/85/Board-report-Under-Companies-Act-2013-23-320.jpg)

The document summarizes the key information that must be included in the Board's report according to the Companies Act 2013 and related rules. It lists items that must be mentioned under section 134, other sections of the Act, and various rules. These include details of meetings, directors, auditors' qualifications, related party transactions, CSR activities, and more. The document provides guidance on the format and content required for the Board's report to comply with statutory requirements.