Downloaded 17 times

The 'Principles of Accounts Curriculum' outlines a three-year teaching framework for the Caribbean Secondary Education Certificate (CSEC) syllabus, effective from September 2017. It emphasizes diverse teaching strategies to accommodate different learning styles and provides a comprehensive content breakdown for secondary education students across various topics including bookkeeping, financial statements, partnerships, and limited liability companies. The curriculum aims to standardize the education of accounting principles in all secondary schools while promoting practical activities and assessments.

Overview of the Principles of Accounts curriculum, designed to standardize CSEC syllabus across all secondary schools.

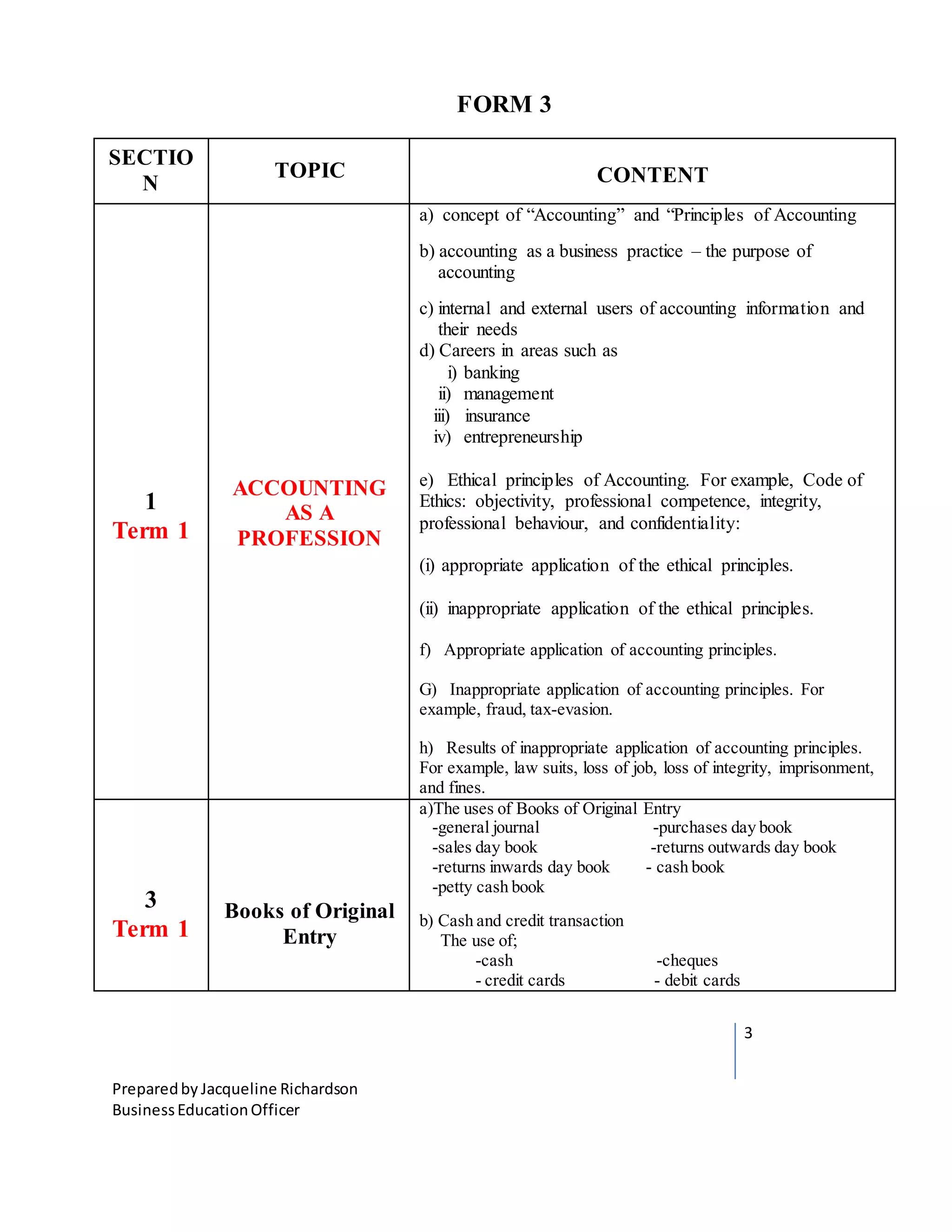

Introduction to accounting principles, career options, and ethical considerations in accounting.

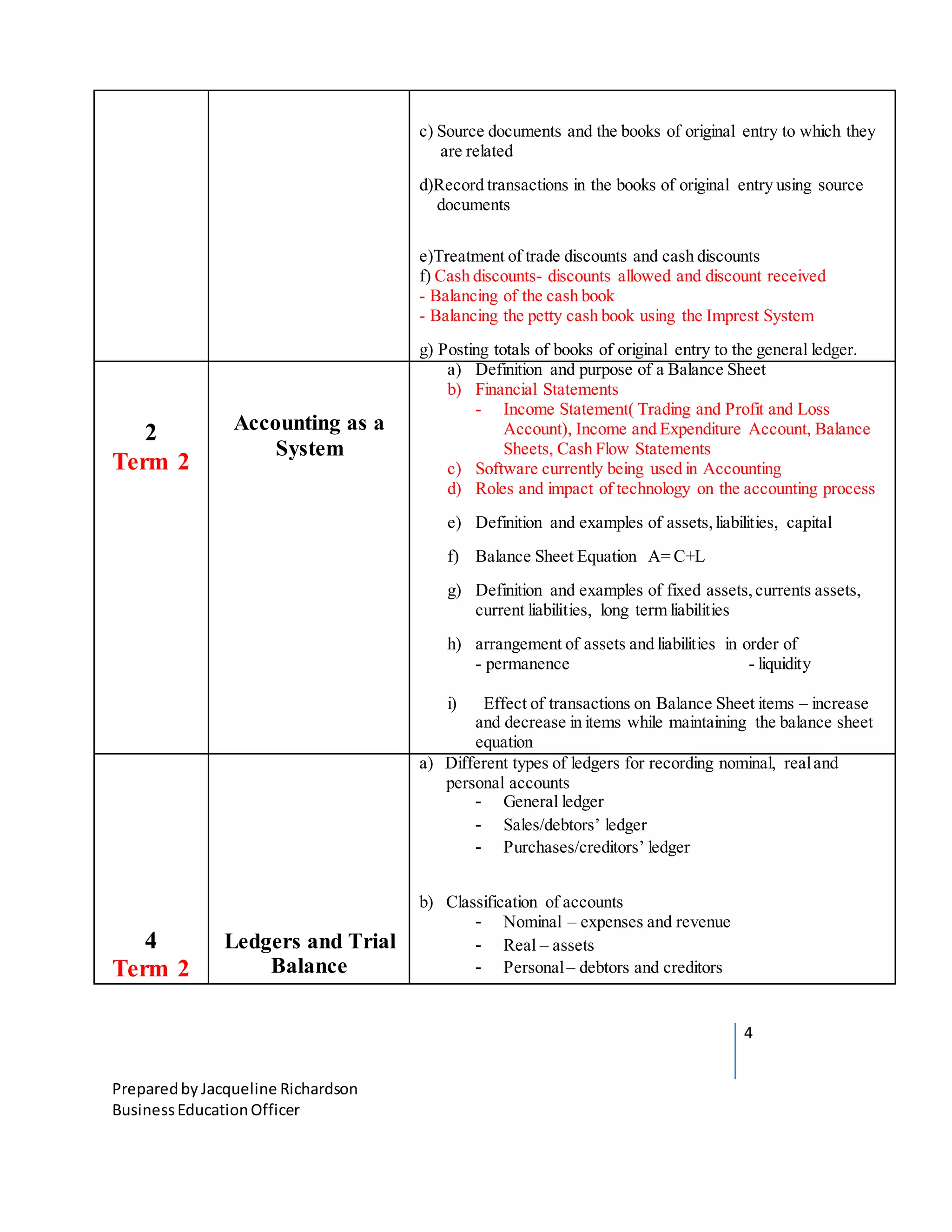

Study of Books of Original Entry including cash book, and treatments for transactions and discounts.

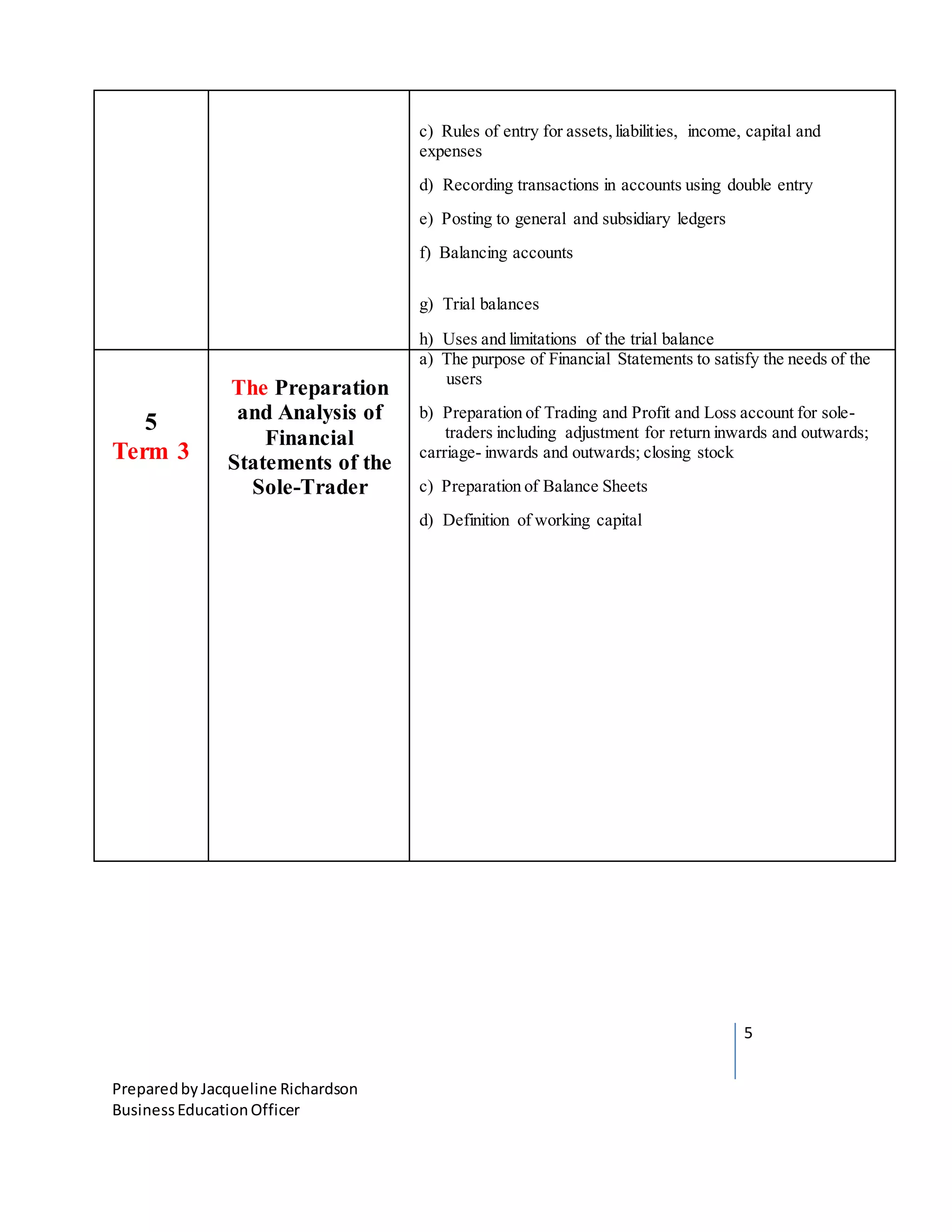

Preparation and analysis of financial statements specifically for sole-traders, focusing on working capital.

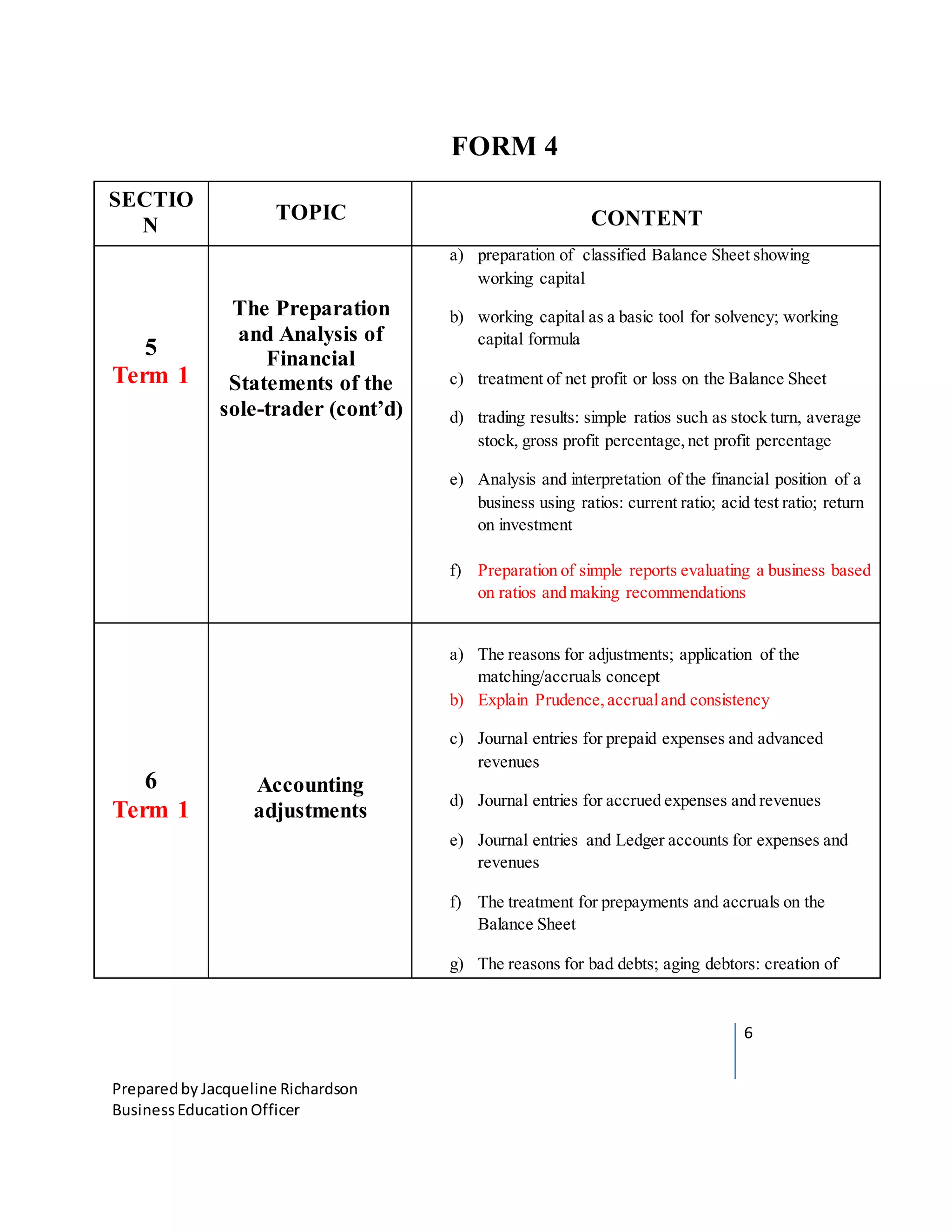

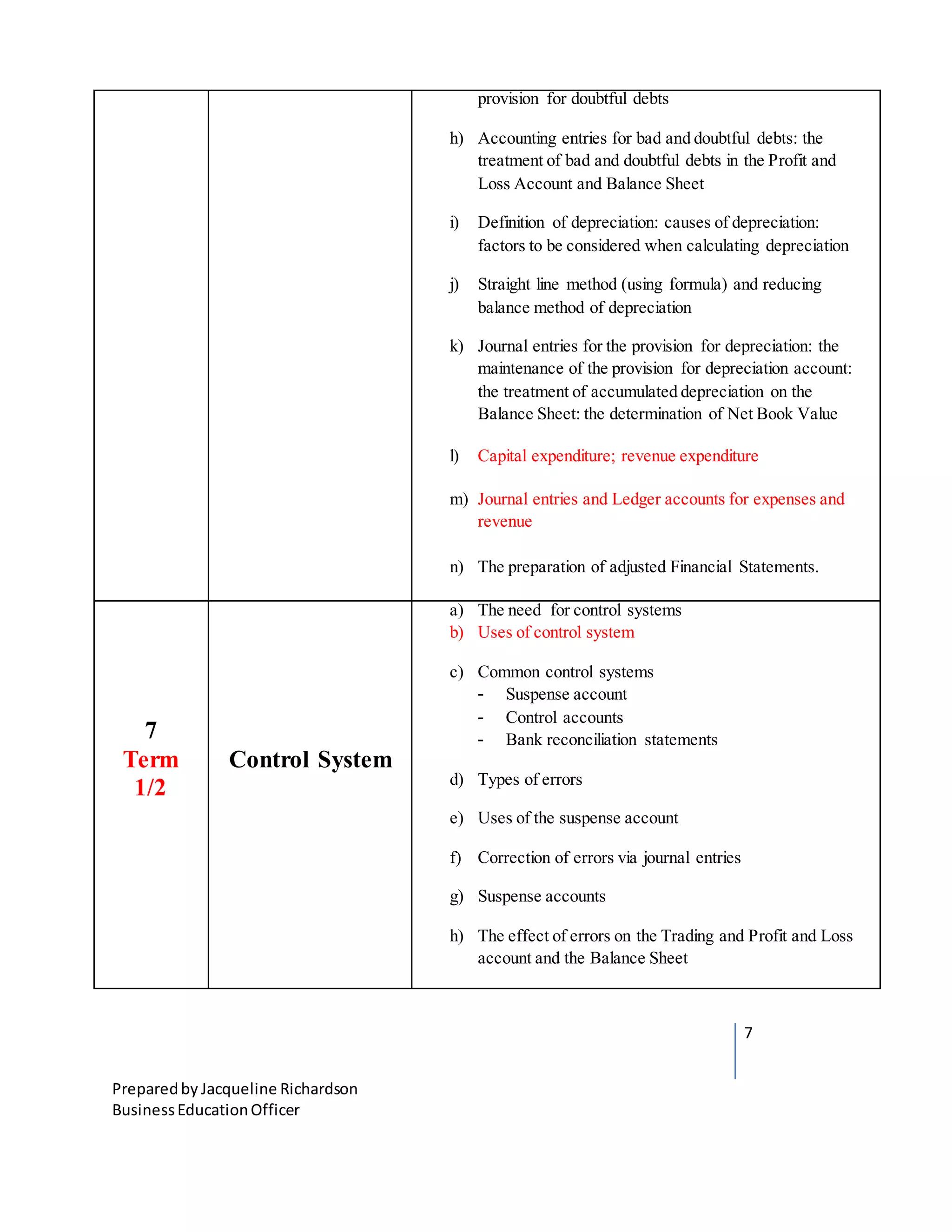

Detailed preparation and analysis of sole-trader financial statements, adjustments, and reporting.

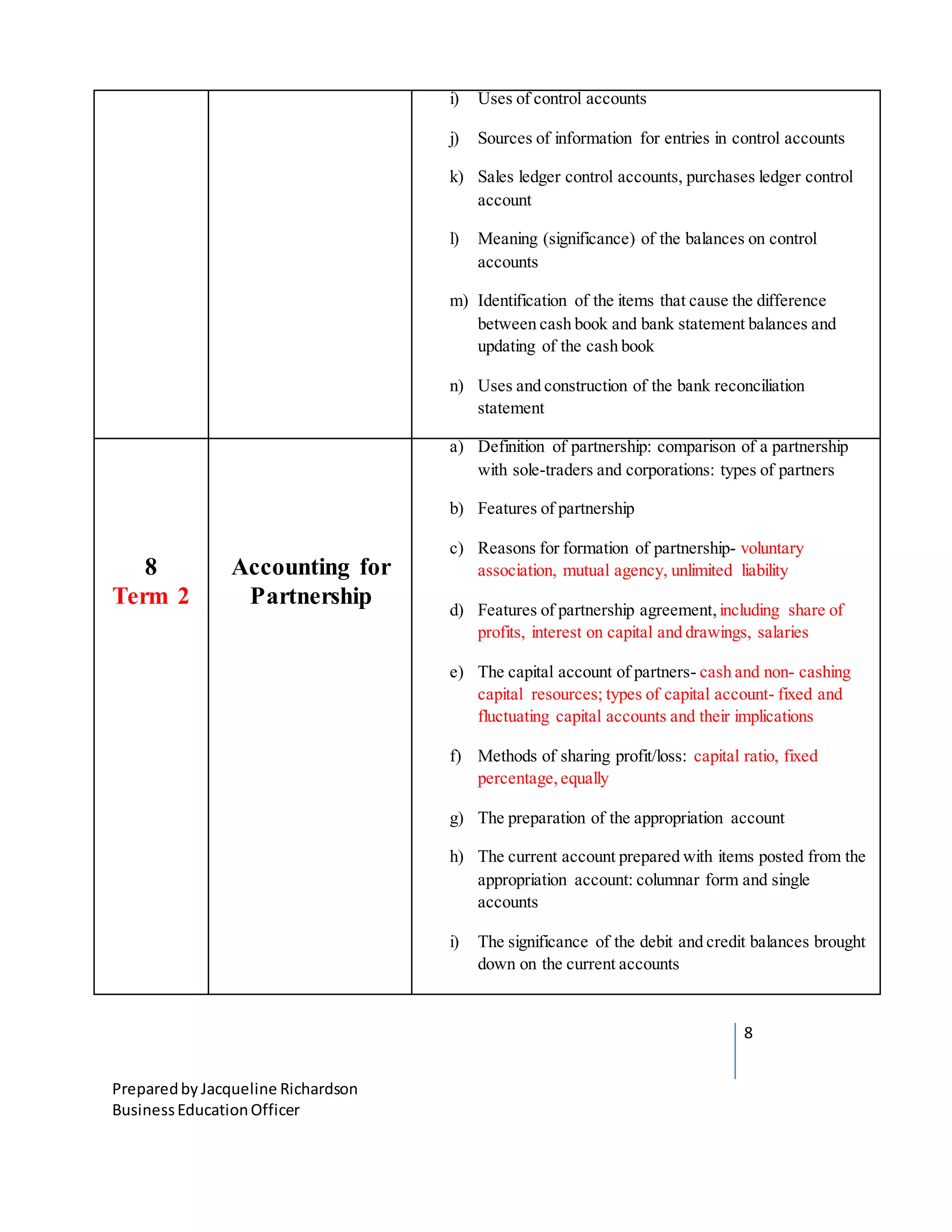

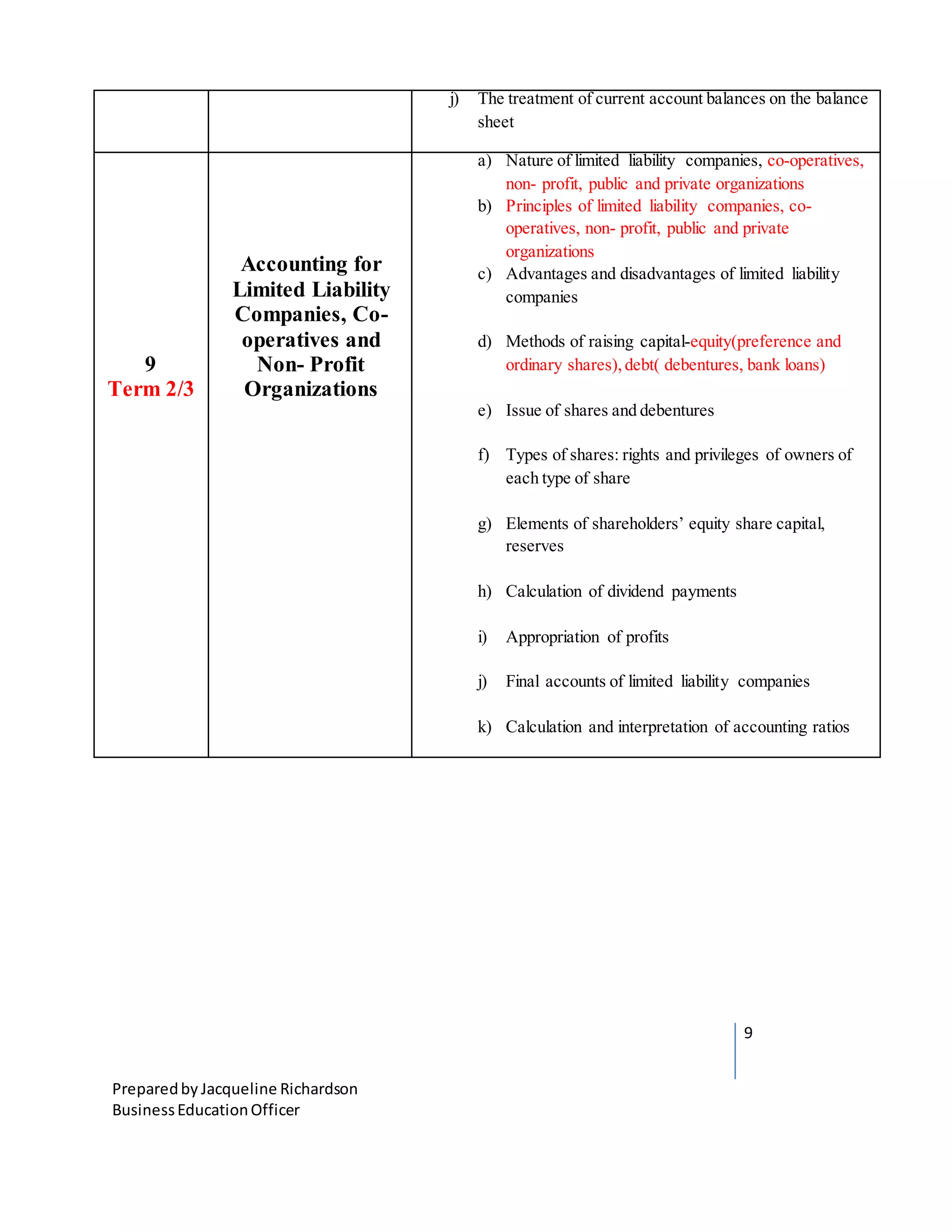

Explains control systems, types of errors, and the use of bank reconciliation statements.Definitions, features, and accounting treatments for partnerships, including the appropriation account.

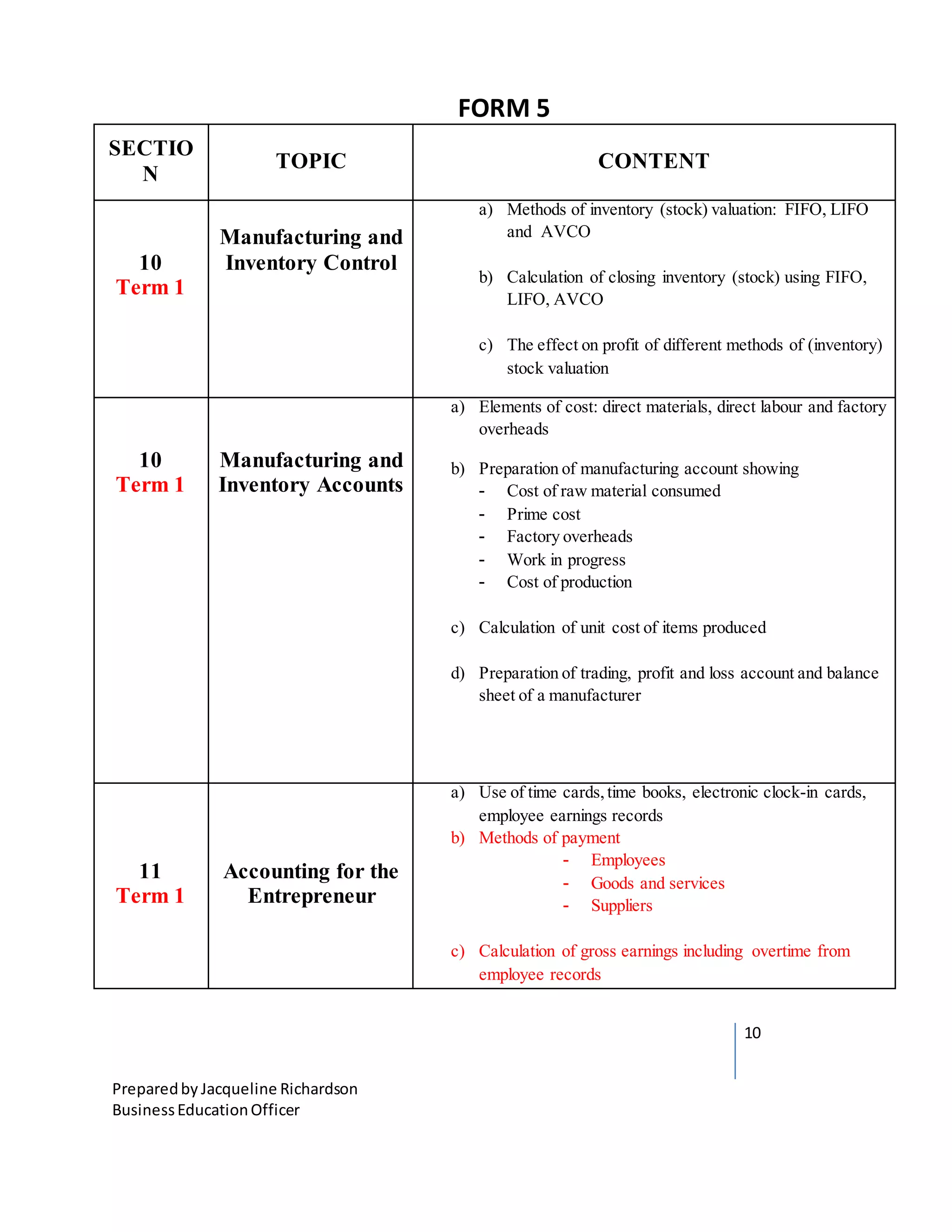

Methods of inventory valuation, manufacturing accounts preparation, and profit impact.

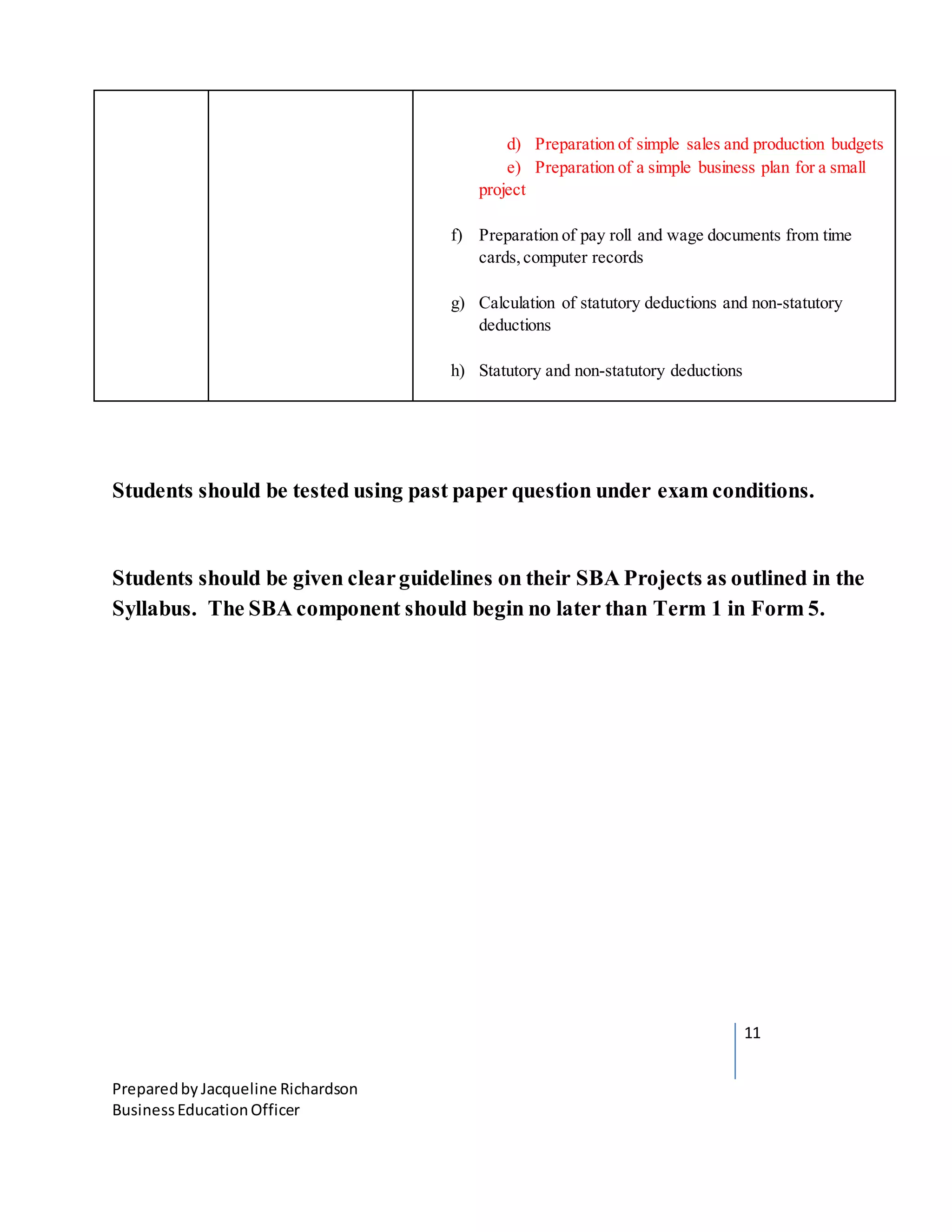

Processes and documentation for employees' earnings, payroll management, and business planning.