![February 2: Purchase of Pistachios: [email protected]$/Kg $

25.000

Purchase of Almonds: 4.000Kg @ 5$/Kg $ 20.000

Purchas of Peanuts: 6.000Kg @ 3$/ Kg $ 18.000

February 3: Purchase of Pistachios: [email protected]$/Kg

$18.000

Purchase of Almonds: 2.000Kg @ 6$/Kg $ 12.000

Purchas of Peanuts: 2.000Kg @ 4$/ Kg $ 18.000

mailto:[email protected]$/Kg

mailto:[email protected]$/Kg

February 6: Sold to several clients:

Pistachios: [email protected] 20$/Kg $40.000

Almonds: 2.500Kg @ 11$/Kg $ 27.500

Peanuts: 3.000Kg @ 7$/ Kg $ 21.000

February 6: Sold to Fruits Lovers Inc.:

Pistachios: 500Kg @20$/Kg. $ 10.000](data:image/gif;base64,R0lGODlhAQABAIAAAAAAAP///yH5BAEAAAAALAAAAAABAAEAAAIBRAA7)

Recommended

Recommended

More Related Content

Similar to BCO114 ACCOUNTING I Task brief & rubrics Task Final Ass.docx

Similar to BCO114 ACCOUNTING I Task brief & rubrics Task Final Ass.docx (20)

More from garnerangelika

More from garnerangelika (20)

Recently uploaded

Recently uploaded (20)

BCO114 ACCOUNTING I Task brief & rubrics Task Final Ass.docx

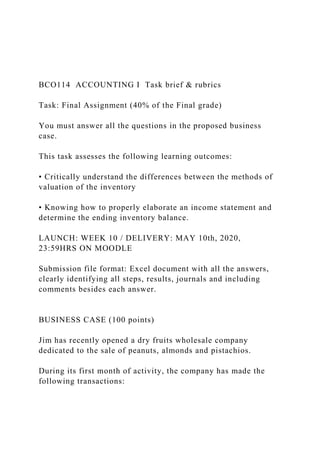

- 1. BCO114 ACCOUNTING I Task brief & rubrics Task: Final Assignment (40% of the Final grade) You must answer all the questions in the proposed business case. This task assesses the following learning outcomes: • Critically understand the differences between the methods of valuation of the inventory • Knowing how to properly elaborate an income statement and determine the ending inventory balance. LAUNCH: WEEK 10 / DELIVERY: MAY 10th, 2020, 23:59HRS ON MOODLE Submission file format: Excel document with all the answers, clearly identifying all steps, results, journals and including comments besides each answer. BUSINESS CASE (100 points) Jim has recently opened a dry fruits wholesale company dedicated to the sale of peanuts, almonds and pistachios. During its first month of activity, the company has made the following transactions:

- 2. February 2: Purchase of Pistachios: [email protected]$/Kg $ 25.000 Purchase of Almonds: 4.000Kg @ 5$/Kg $ 20.000 Purchas of Peanuts: 6.000Kg @ 3$/ Kg $ 18.000 February 3: Purchase of Pistachios: [email protected]$/Kg $18.000 Purchase of Almonds: 2.000Kg @ 6$/Kg $ 12.000 Purchas of Peanuts: 2.000Kg @ 4$/ Kg $ 18.000 mailto:[email protected]$/Kg mailto:[email protected]$/Kg February 6: Sold to several clients: Pistachios: [email protected] 20$/Kg $40.000 Almonds: 2.500Kg @ 11$/Kg $ 27.500 Peanuts: 3.000Kg @ 7$/ Kg $ 21.000 February 6: Sold to Fruits Lovers Inc.: Pistachios: 500Kg @20$/Kg. $ 10.000

- 3. Almonds: 1.000Kg @ 11$/Kg $ 11.000 Peanuts: 1.500Kg @ 8$/ Kg $ 12.000 February 12 Purchase of Pistachios: [email protected]$/Kg $ 21.000 Purchase of almonds: 2.000Kg @ 8$/Kg $ 16.000 February 13: Sale of peanuts to Peanuts Lovers Inc.: 3.500Kg @8$/kg $ 28.000 February 14: Purchase of Peanuts 6.000 Kg @4$/Kg $24.000 February 19: Sold to several clients: Pistachios: [email protected] 21$/Kg. $ 21.000 Almonds: 1.500Kg @ 13$/Kg $ 19.500 Peanuts: 3.000Kg @ 9$/ Kg $ 27.000 February 25: Purchased from various suppliers: Pistachios: [email protected]$/Kg. $ 13.000 mailto:[email protected]$/Kg mailto:[email protected]$/Kg

- 4. Almonds: 1.000Kg @ 9$/Kg $ 9.000 Peanuts: 1.000Kg @ 4$/ Kg $ 4.000 Besides these transactions, the company has had the following expenses: Salaries: $3500 Electricity bill: $300 Renting of equipment: &800 Rent of warehouse and office: $1.500 Miscellaneous: $1.200 Jim’s accountant recommended that he should use the average cost method in order to determine the cost of the inventory sold but he is not sur e about the consequences it nay have on his financial situation Relying on your accounting knowledge, Jim asks you the following questions: 1: Why in your opinion did Jim’s accountant recommend the average cost method and what difference is there whit the three other methods? Explain the main characteristics of each method of valuation of the inventory and the consequences they may have on the valuation of the

- 5. inventory and determination of the net income in case of price fluctuation. (20 points) 2: Prepare an Income statement of the company at the end of February using as method of valuation of the inventory the average cost method, FIFO and LIFO for each one of the products sold by Jim, and calculate the balance of the inventory at the end of the month. Explain the calculations. (40 points: 30 points for the calculation and 10 for explanations) 3: In order to compare with the records made by his accountant, Jim asks you to prepare the different journal entries for the purchases and sales mentioned above for each one of the 3 different methods used above. (15 points) 4: Jim’s accountant insisted that he should use a perpetual inventory system instead of a periodic inventory system and the average cost method for valuating the inventory. Do you agree with this advice (justify your answer)? Would the balance of the inventory at the end of the month be the same? And the net income? (15 points) 5: Jim would like to know a forecast of the number of days to sell the inventory based on the results of the month of February. Explain your calculation and the steps followed. (10 points: 5 for calculation and 5 for explanation)

- 6. 6. Jim expects that the prices of the merchandises will dramatically decrease in the next future as a result of the Covid 19 crisis. Which method of valuation of the inventory would you thus recommend to Jim? Explain your answer. (5 points) Rubrics Descriptor 9-10 The student demonstrates an excellent understanding of the concepts. 8-8.9 The student demonstrates a good understanding of the concepts. 7-7.9 The student demonstrates a fair understanding of the concepts. 6-6.9 The student demonstrates some, but insufficient understanding of the concepts. 3-5.9 The student demonstrates insufficient understanding of the concepts. They may mention some relevant ideas or concepts, although it

- 7. is clear that the relationship between them is not understood by the student. 1-2.9 The student demonstrates insufficient understanding of the concepts and does not mention any relevant ideas or concepts. 0 The student leaves the question blank or cheats. 95% of the grade based on the approach, calculations and comments, and 5% based on the presentation and look & field of the spreadsheet. Points are at the end of each question. ACC 371 Lecture 7 Statement of Cash Flows Introduction Generally Accepted Accounting Principles (GAAP) typically evolves in practice, rather than being written and then followed. An example of this evolution is the financial statement called, the statement of cash flows. Managers and business owners often asked why their companies were profitable but did not have available cash, or had plenty of cash but were operating at a loss. In response to this need, accountants developed the statement of cash flows to explain how cash was provided to the company or used by the company. The statement of cash flows is now a required financial statement according to GAAP. Since the statement of cash flows was developed long after the other three statements—the balance sheet, income statement, and

- 8. statement of stockholders' equity—it does not follow the same flow as the other statements and requires information from all of the other statements, as well as additional information, in order to be compiled. Today, the statement of cash flows is one of the most significant financial statements for the potential investor or creditor. Usefulness of the Statement of Cash Flows The statement of cash flows is useful because it shows an organization's ability to produce future cash flows, provides an indication that the organization can meet its obligations, reports the differences between net income and net cash flows, and identifies the cash and noncash investing and financing activities during the period. Profitable operations do not always ensure positive cash flow. While net income is important, cash flow is also critical to a company's success. Cash flow permits a company to expand operations, replace worn assets, take advantage of new investment opportunities, and pay dividends to its owners. Both managers and analysts need to understand the various sources and uses of cash that are associated with business activities. The cash flow statement focuses attention on a firm's ability to generate cash internally, its management of current assets and current liabilities, and the details of its investments and its external financing (Libby, Libby, & Short, 2004). It is designed to help both managers and analysts answer important cash- related questions such as these: Will the company have enough cash to pay its short-term debts to suppliers and other creditors without additional borrowing? Is the company adequately managing its accounts receivable and inventory? Has the company made necessary investments in new productive capacity? Did the company generate enough cash flow internally to finance necessary investment or did it rely on external financing? Is the company changing the makeup of its external financing?

- 9. These questions and others can be answered through the preparation and examination of the statement of cash flows. Operating, Investing, and Financing Activities The statement has three main sections: (a) cash flows from operating activities, which are related to income from normal, recurring operations; (b) cash flows from investing activities, which are related to the acquisition and sale of productive assets; and (c) cash flows from financing activities, which are related to external financing of the enterprise. The net cash inflow or outflow for the year is the same amount as the increase or decrease in cash and cash equivalents for the year on the balance sheet. Cash equivalents are highly liquid investments with original maturities of less than three months. The operating activities section of the statement of cash flows can be prepared using direct or indirect methods; the investing and financing activities sections are always prepared directly. The cash flows from operating activities section of the statement of cash flows includes the "cash effects of transactions that enter into the determination of net income" (Kieso, Weygandt & Warfield, 2013, p. 1413). The cash flows from investing activities section of the statement of cash flows includes transactions involving long-term assets, and the cash flows from financing activities section of the statement of cash flows includes transactions involving liability and equity items (Kieso, et. al., 2013). Direct Method of Determining Cash Flows from Operating Activities The direct method for reporting cash flows from operating activities accumulates all of the operating transactions that result in either a debit or credit to cash into categories of cash inflows and cash outflows. The most common inflows are cash received from customers and dividends as well as interest on investments. The most common outflows are cash paid for the purchase of services and goods for resale, salaries and wages, income taxes, and interest on liabilities. The statement of cash flows from operating activities is prepared by adjusting each

- 10. item on the income statement from an accrual basis to a cash basis. Indirect Method of Determining Cash Flows from Operating Activities The indirect method for reporting cash flows from operating activities includes a conversion of net income to net cash flow from operating activities. The conversion involves additions and subtractions for non-cash accruals, including expenses (such as depreciation expense) and revenues that do not affect current assets or current liabilities, and changes in each of the individual current assets (other than cash and short-term investments) and current liabilities (other than short-term debt to financial institutions and current maturities of long-term debt, which relate to financing), which reflect differences in the timing of accrual-basis net income and cash flows. The Financial Accounting Standards Board (FASB) encourages the use of the direct method over the indirect method for reporting the operating activities section of the statement of cash flows, and requires supplemental disclosures of information if the indirect method is presented (Kieso, Weygandt, & Warfield, 2013). It is important to note that net cash provided by operating activities on the statement of cash flows is equivalent to cash basis net income for the company (Kieso, et. al., 2013). Cash Flows from Investing Activities Investing activities reported on the cash flow statement include cash payments to acquire fixed assets and short- and long-term investments and cash proceeds from the sale of fixed assets and short- and long-term investments. Cash Flows from Financing Activities Cash inflows from financing activities include cash proceeds from the issuance of short- and long-term debt and common stock. Cash outflows include cash principal payments on short- and long-term debt, cash paid for the repurchase of the

- 11. company's stock, and cash dividend payments. Cash payments associated with interest are a cash flow from operating activities. Significant Noncash Transactions Any significant non-cash transactions that would not otherwise be presented in the statement of cash flows must be disclosed so that the user can reconcile the statement of cash flows to the comparative balance sheets. Analysis of Cash Flow Ratios Cash flow ratios are highly scrutinized by present and potential creditors. The statement of cash flows, in conjunction with ratio analysis, can indicate whether a borrower will be able to repay funds if borrowed. The following ratios are typically used by present and potential creditors in analyzing cash flow potential. Free cash flow - (cash flow from operating activities – capital expenditures – cash dividends) measures the cash remaining from operations after the company makes investments in new assets and pays out the expected dividends to stockholders (Kimmel, Weygandt, & Kieso, 2009). Free cash flow gives the analyst a better idea of how much cash truly is available from cash flows from operations than looking at the statement of cash flows alone. Quality of income ratio - (cash flow from operating activities ÷ net income) measures the portion of income that was generated in cash. A higher quality of income ratio indicates greater ability to finance operating and other cash needs from operating cash inflows. A higher ratio also indicates that it is less likely that the company is using aggressive revenue recognition policies to increase net income. Capital acquisition ratio - (cash flow from operating activities ÷ cash paid for property, plant, and equipment) reflects the portion of purchases of property, plant, and equipment financed from operating activities without the need for outside debt or equity financing or the sale of other investments or fixed assets. A high ratio benefits the company because it provides the company with opportunities for strategic acquisitions (Libby et

- 12. al., 2004). Impact of Additional Cash Flow Disclosures Noncash investing and financing activities are investing and financing activities that do not involve cash. They include, for example, purchases of fixed assets with long-term debt or stock, exchanges of fixed assets, and exchanges of debt for stock. These transactions are disclosed only as supplemental disclosures to the cash flow statement along with cash paid for taxes and interest under the indirect method. Relevance to Professional Accounting Examinations The Uniform CPA (Certified Public Accountant) Exam tests knowledge of information contained in this lecture in the Financial Accounting and Reporting (FAR) section, according to the Content Specific Outlines published by the AICPA (AICPA, 2009). This content is part of the Financial Statement Accounts: Recognition, Measurement, Valuation, Calculation, Presentation, and Disclosures section that comprises 27 - 33% of the FAR section of the Uniform CPA Exam (AICPA, 2009). Conclusion The statement of cash flows is considered by many to be the most important of the financial statements in indicating a company's ability to remain a going concern. Although a company's mission, product, distribution chain, corporate culture, and marketing strategy are all key elements of a successful business, a company cannot survive in the short term without available cash. To employ workers, replenish inventory, and foster growth a company must have sufficient cash available to pay for its current operating expenses, meet maturing long-term debt obligations, and supply working capital for opportunities that arise. There must exist a balance between having enough cash on hand to meet needs and keeping funds invested in the assets of a business. The statement of cash flows aids users in analyzing whether a company is successful in achieving this balance. References American Institute of Certified Public Accountants (AICPA).

- 13. (2009). Content and skill specifications for the Uniform CPA Exam. Retrieved electronically from http://www.aicpa.org/BecomeACPA/CPAExam/ExaminationCon tent/ContentAndSkills/DownloadableDocuments/CSOs-SSOs- Final-Release-Version-effective-01-01-2011.pdf. Kieso, D. E., Weygandt, J. J., & Warfield, T. D. (2013). Intermediate accounting (15e). Hoboken, NJ: John Wiley & Sons. Kimmel, P. D., Weygandt, J. J., & Kieso, D. E. (2009). Accounting: Tools for business decision making (3rd ed.). Hoboken, NJ: John Wiley & Sons, Inc. Libby, R., Libby, P., & Short, D. (2004). Financial accounting (4th ed.). Boston: McGraw-Hill/Irwin. © 2013. Grand Canyon University. All Rights Reserved.