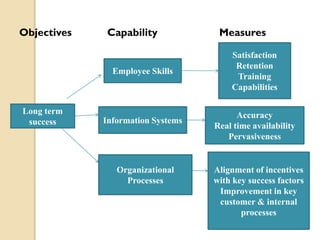

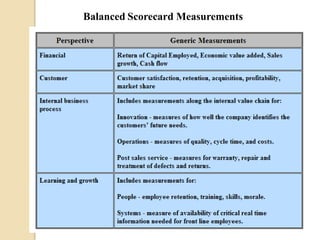

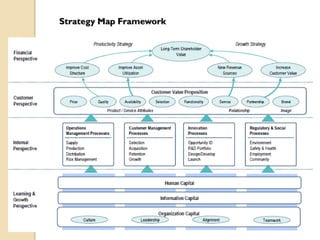

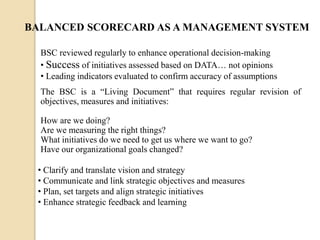

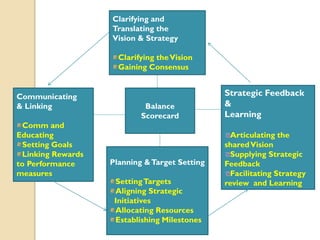

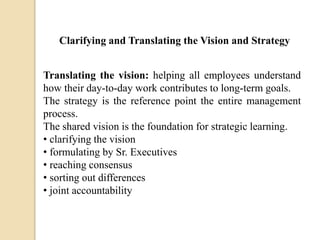

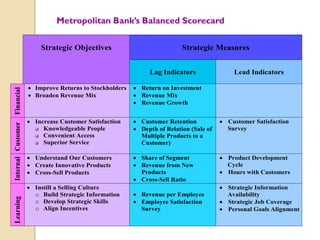

The document provides an overview of the Balanced Scorecard framework developed by Robert Kaplan and David Norton in the early 1990s. It discusses that the Balanced Scorecard translates an organization's mission and strategy into a comprehensive set of performance measures across four perspectives: financial, customer, internal business processes, and learning and growth. The Balanced Scorecard helps organizations implement their strategies by setting objectives and measures for each perspective, and monitoring performance to drive continuous improvement.