Downloaded 22 times

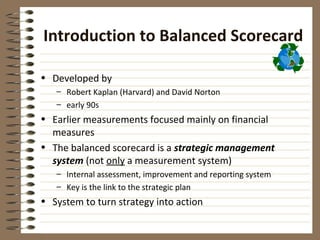

The balanced scorecard is a strategic management tool developed in the early 1990s by Robert Kaplan and David Norton to provide a more holistic view of an organization beyond just financial measures by including additional perspectives such as customer, internal business processes, and learning and growth; it helps organizations translate their strategy into actionable objectives and measures across multiple perspectives and provides feedback to improve performance over time.