Download to read offline

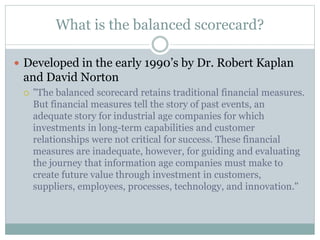

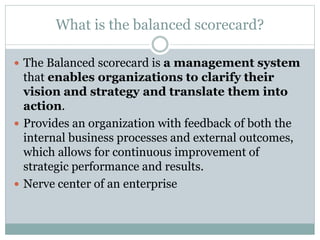

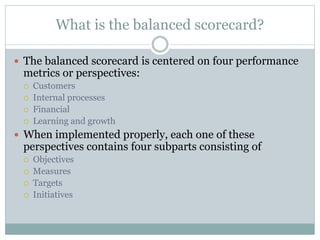

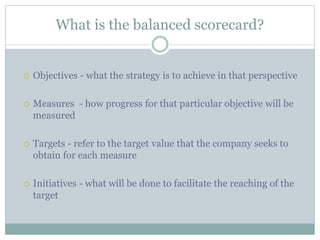

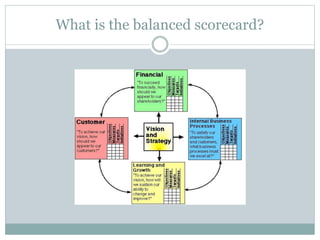

The balanced scorecard is a strategic planning and management system developed in the early 1990s. It provides a framework for translating an organization's mission and strategy into a comprehensive set of performance measures. The balanced scorecard suggests that organizations must balance four perspectives - financial, customer, internal business process, and learning and growth. Each perspective contains objectives, measures, targets, and initiatives. Together these provide managers with a comprehensive picture of an organization's overall health.