Downloaded 3,479 times

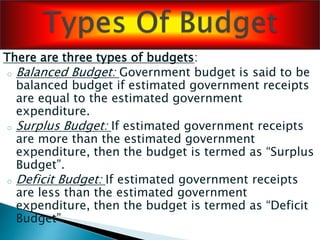

The document discusses key aspects of government budgets including: - Budgets show estimated annual receipts and expenditures and are divided into revenue and capital components. - Objectives include reallocating resources, managing public enterprises, and promoting economic stability. - Receipts are classified as revenue or capital, and expenditures are classified as revenue or capital. - Budgets can be balanced, in surplus, or in deficit depending on a comparison of estimated receipts to expenditures. - Deficits include revenue deficit, fiscal deficit, and primary deficit, with fiscal deficit being the broadest measure of imbalance.