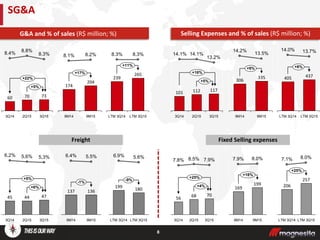

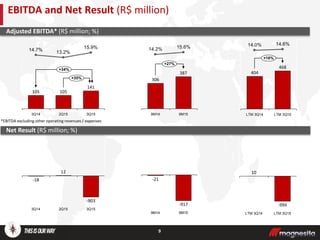

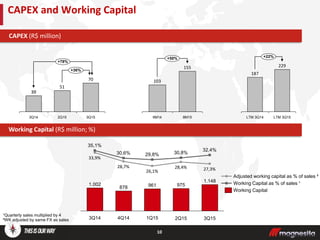

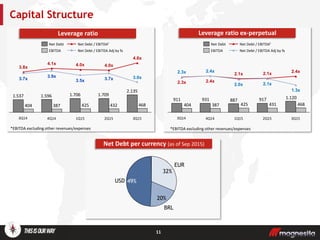

Magnesita reported its 3Q15 earnings. Revenue declined 5% year-over-year to $669 million due to lower steel production in key markets. EBITDA increased 27% to $141 million despite lower sales, with margins improving to 15.9% from 14.7% in 3Q14. Working capital increased to 32.4% of sales due to currency impacts and strategic inventory build. Net debt declined but leverage ratios remained elevated at 3.0x net debt/EBITDA excluding perpetual bonds. Overall, earnings exceeded expectations due to margin expansion despite currency headwinds and weaker steel markets.