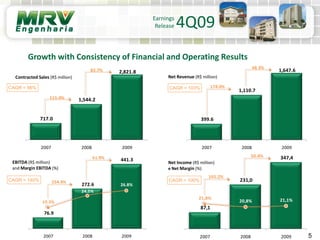

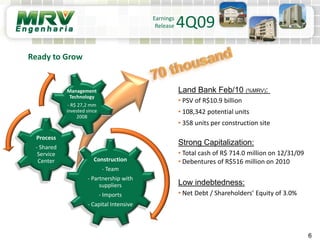

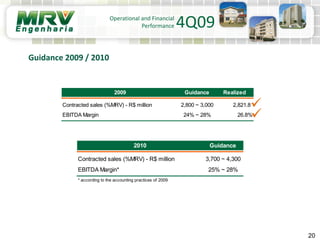

Contracted sales in 2009 were R$2.8 billion, up 82.7% from the previous year and achieving guidance. EBITDA margin was 26.8% in 2009, achieving guidance. Net income increased 50.4% to R$347.4 million in 2009 with a net margin of 21.1%. The company has a strong land bank of R$10.9 billion and is well capitalized with R$714 million in cash and a recent R$516 million debenture issue in March 2010. Guidance for 2010 is for contracted sales of R$3.7-4.3 billion and an EBITDA margin of 25-28%.