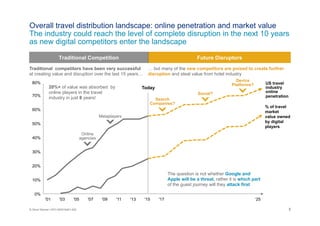

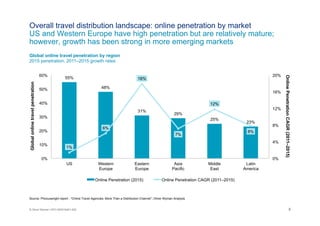

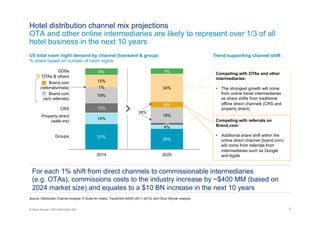

The digital travel revolution poses a threat to the hotel industry as new digital competitors are poised to disrupt distribution and capture significant market value. Large digital players have demonstrated the ability to rapidly gain scale in targeted segments. Winners will be those that solve customer hassles along the entire guest journey and build interactional and collaborative relationships rather than purely transactional ones. To respond, hotel companies must rethink distribution's role, build a holistic operating model, define segment and channel strategies, develop a comprehensive revenue agenda, and measure performance using RevPARD.