Download as PDF, PPTX

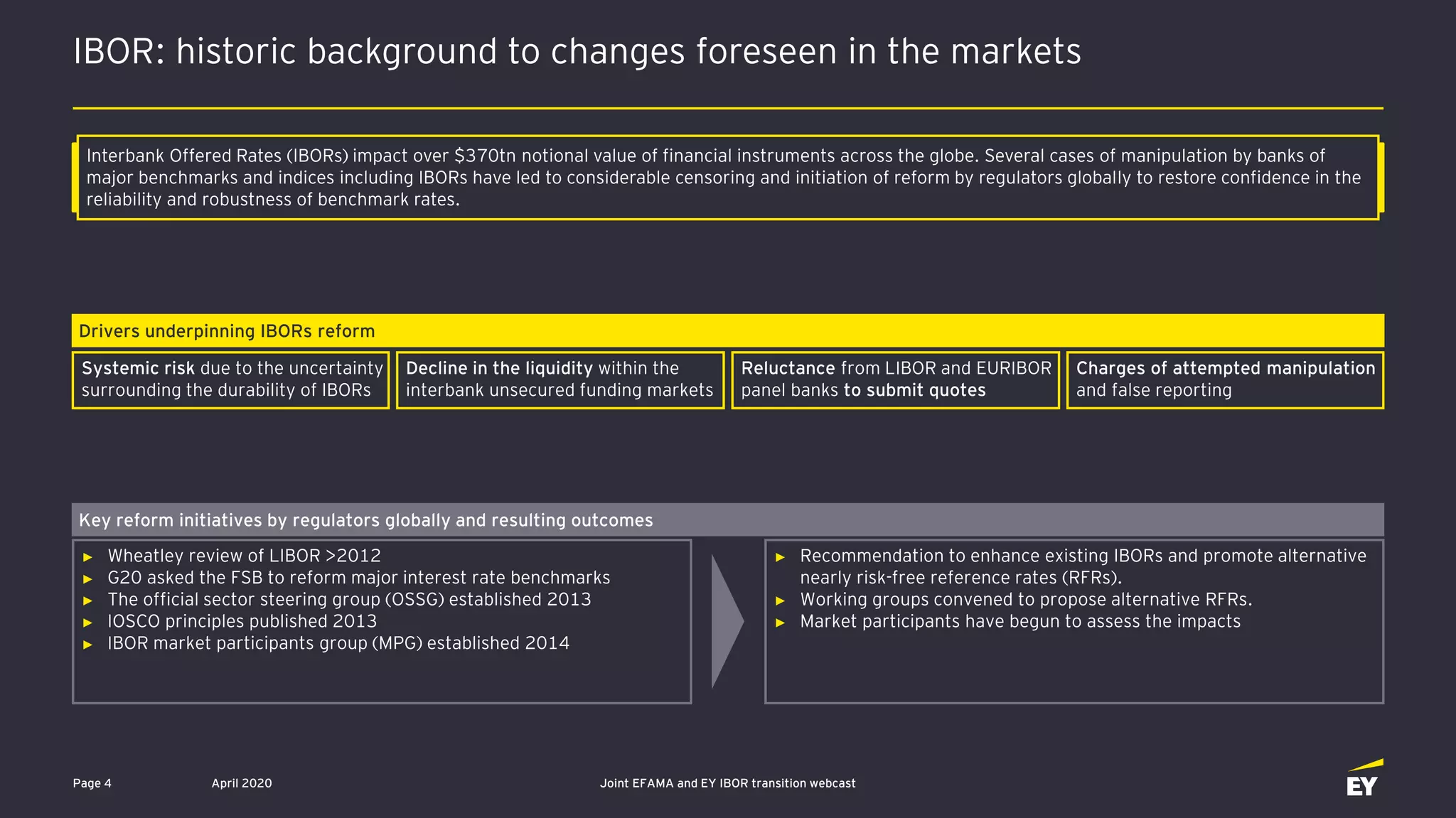

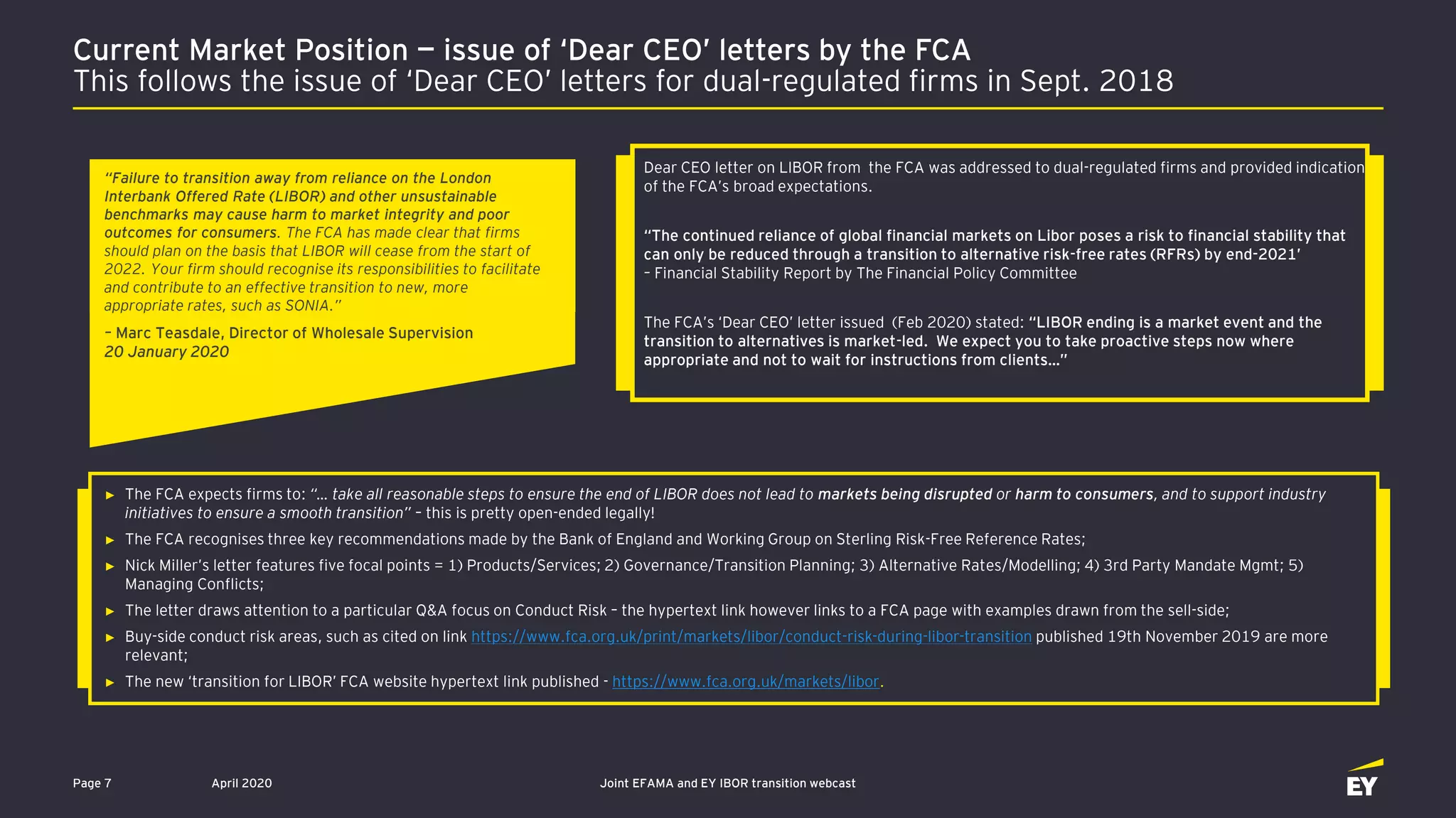

This document provides an agenda and overview of a webinar discussing the IBOR transition for the asset management industry. The webinar covers topics such as the progress of the transition, impact on asset managers and products, perspectives from European central banking working groups, and how firms are migrating. It introduces the speakers and their topics. In addition, it provides background on the drivers for IBOR reform, timeline of key milestones, and summaries of transition progress for different jurisdictions.