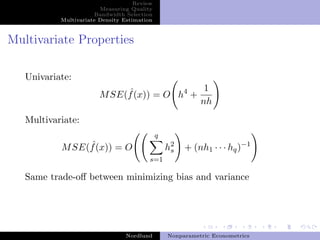

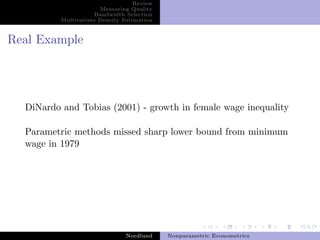

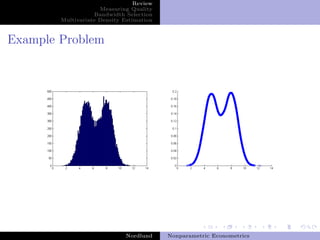

This document summarizes key concepts in nonparametric econometrics and kernel density estimation. It discusses bandwidth selection methods like cross-validation and plug-in approaches. It also covers multivariate density estimation, noting the trade-off between bias and variance. The document analyzes a real example from DiNardo and Tobias on estimating the density of female wages.

![Review

Measuring Quality

Bandwidth Selection

Multivariate Density Estimation

Definitions

Definition (Convergence in rth Mean)

We say that xn converges to X in the rth mean, if for some

r > 0,

lim E[||xn − X||r ] = 0

n→∞

rth

We write this as xn → X

Nordlund Nonparametric Econometrics](https://image.slidesharecdn.com/npdnordlund-13058405051495-phpapp02-110519162856-phpapp02/85/Nonparametric-Density-Estimation-6-320.jpg)

![Review

Measuring Quality

Bandwidth Selection

Multivariate Density Estimation

Inside the Proof

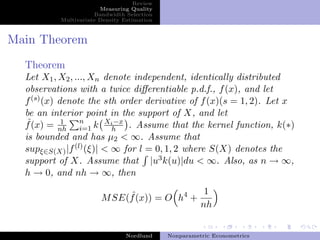

Recall that

ˆ ˆ ˆ ˆ

M SE(f (x) = E [f (x) − f (x)]2 = V ar(f (x)) + Bias(f (x))2 .

Along the proof, we obtain

ˆ h2 (2)

Bias(f (x)) = f (x) u2 k(u)du + O(h3 )

2

and

ˆ 1

V ar(f (x)) = f (x) k(u)j du + O(h)

nh

Notice that there is a trade off between minimizing variance

and bias

Nordlund Nonparametric Econometrics](https://image.slidesharecdn.com/npdnordlund-13058405051495-phpapp02-110519162856-phpapp02/85/Nonparametric-Density-Estimation-9-320.jpg)