Download to read offline

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

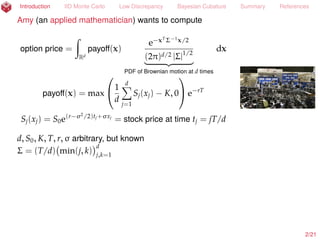

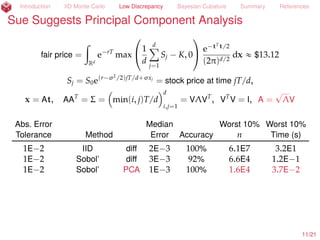

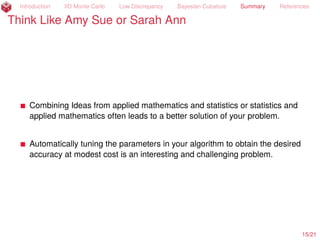

Amy (an applied mathematician) wants to compute

option price =

ż

Rd

payoff(x)

e´xT

Σ´1

x/2

(2π)d/2 |Σ|1/2

looooooomooooooon

PDF of Brownian motion at d times

dx

payoff(x) = max

1

d

dÿ

k=1

Sk(xk) ´ K, 0 e´rT

Sk(xk) = S0e(r´σ2

/2)tk+σxk

= stock price at time tk = kT/d

d, S0, K, T, r, σ arbitrary, but known

Σ = (T/d) min(k, l)

d

k,l=1

Sue (a statistician) wants to compute

Gaussian probability =

ż

[a,b]

e´xT

Σ´1

x/2

(2π)d/2 |Σ|1/2

dx

a, b, Σ arbitrary, but known

2/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-3-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Amy Suggests Rectangular Grids & Product Rules

ż 1

0

f(x) dx ´

1

m

mÿ

i=1

f

2i ´ 1

2m

= O(m´2

), so

ż

[0,1]d

f(x) dx

´

1

2m

mÿ

i1=1

¨ ¨ ¨

mÿ

id=1

f

2i1 ´ 1

2m

, . . . ,

2id ´ 1

2m

= O(m´2

) = O(n´2/d

)

assuming partial derivatives of up to order 2 in each direction exist.

3/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-4-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Amy Suggests Rectangular Grids & Product Rules

ż 1

0

f(x) dx ´

1

m

mÿ

i=1

f

2i ´ 1

2m

= O(m´2

), so

ż

[0,1]d

f(x) dx

´

1

2m

mÿ

i1=1

¨ ¨ ¨

mÿ

id=1

f

2i1 ´ 1

2m

, . . . ,

2id ´ 1

2m

= O(m´2

) = O(n´2/d

)

assuming partial derivatives of up to order 2 in each direction exist.

3/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-5-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Amy Suggests Rectangular Grids & Product Rules

ż 1

0

f(x) dx ´

1

m

mÿ

i=1

f

2i ´ 1

2m

= O(m´2

), so

ż

[0,1]d

f(x) dx

´

1

2m

mÿ

i1=1

¨ ¨ ¨

mÿ

id=1

f

2i1 ´ 1

2m

, . . . ,

2id ´ 1

2m

= O(m´2

) = O(n´2/d

)

assuming partial derivatives of up to order 2 in each direction exist.

Computational cost is prohibitive for large dimensions, d:

d 1 2 5 10 100

m = 8, n = 8d

8 64 3.3E4 1.0E9 2.0E90

Product rules are a bad idea unless d is small.

3/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-6-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Sue Suggests IID Monte Carlo

µ = E[f(X)] =

ż

Rd

f(x) ρ(x) dx

« ^µn =

1

n

nÿ

i=1

f(xi), xi

IID

„ ρ

P[|µ ´ ^µn| ď errn] « 99%

for errn =

2.58 ˆ 1.2^σ

?

n

by the Central Limit Theorem (CLT),

where ^σ2

is the sample variance. But the CLT is only an asymptotic result, and

1.2^σ may be an overly optimistic upper bound on σ.

5/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-8-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Sue Suggests IID Monte Carlo

µ = E[f(X)] =

ż

Rd

f(x) ρ(x) dx

« ^µn =

1

n

nÿ

i=1

f(xi), xi

IID

„ ρ

P[|µ ´ ^µn| ď errn] « 99%

for errn =

2.58 ˆ 1.2^σ

?

n

by the Central Limit Theorem (CLT),

where ^σ2

is the sample variance. But the CLT is only an asymptotic result, and

1.2^σ may be an overly optimistic upper bound on σ.

A Berry-Esseen Inequality, Cantelli’s Inequality, and an assumed upper bound on

the kurtosis can be used to provide a rigorous error bound (H. et al., 2013; Jiang,

2016). More

5/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-9-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Sue’s Gaussian Probability

µ =

ż

[a,b]

exp ´1

2 tT

Σ´1

t

a

(2π)d det(Σ)

dt

affine

=

ż

[0,1]d

f(x) dx

For some typical choice of a, b, Σ, d = 3; µ « 0.6763

Rel. Error Median Worst 10% Worst 10%

Tolerance Method Error Accuracy n Time (s)

1E´2 IID Affine 7E´4 100% 1.5E6 1.8E´1

6/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-10-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Amy Suggests a Variable Transformation

µ =

ż

[a,b]

exp ´1

2 tT

Σ´1

t

a

(2π)d det(Σ)

dt

Genz (1993)

=

ż

[0,1]d´1

f(x) dx

For some typical choice of a, b, Σ, d = 3; µ « 0.6763

Rel. Error Median Worst 10% Worst 10%

Tolerance Method Error Accuracy n Time (s)

1E´2 IID Affine 7E´4 100% 1.5E6 1.8E´1

1E´2 IID Genz 4E´4 100% 8.1E4 1.9E´2

6/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-11-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

IID Monte Carlo Is Slow

µ =

ż

[a,b]

exp ´1

2 tT

Σ´1

t

a

(2π)d det(Σ)

dt

Genz (1993)

=

ż

[0,1]d´1

f(x) dx

For some typical choice of a, b, Σ, d = 3; µ « 0.6763

Rel. Error Median Worst 10% Worst 10%

Tolerance Method Error Accuracy n Time (s)

1E´2 IID Affine 7E´4 100% 1.5E6 1.8E´1

1E´2 IID Genz 4E´4 100% 8.1E4 1.9E´2

1E´3 IID Genz 7E´5 100% 2.0E6 3.8E´1

6/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-12-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Sue Suggests IID Monte Carlo

µ = E[f(X)] =

ż

Rd

f(x) ρ(x) dx

« ^µn =

1

n

nÿ

i=1

f(xi), xi

IID

„ ρ

P[|µ ´ ^µn| ď errn] « 99%

for errn =

2.58 ˆ 1.2^σ

?

n

by the Central Limit Theorem (CLT),

where ^σ2

is the sample variance. But the CLT is only an asymptotic result, and

1.2^σ may be an overly optimistic upper bound on σ.

A Berry-Esseen Inequality, Cantelli’s Inequality, and an assumed upper bound on

the kurtosis can be used to provide a rigorous error bound (H. et al., 2013; Jiang,

2016). More

7/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-13-320.jpg)

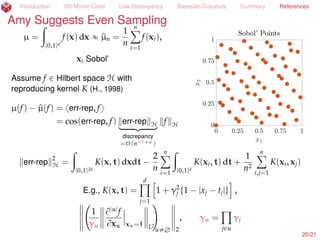

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Amy Suggests More Even Sampling than IID

µ =

ż

[0,1]d

f(x) dx « ^µn =

1

n

nÿ

i=1

f(xi),

xi Sobol’ (Dick and Pillichshammer, 2010)

Normally n should be a power of 2

8/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-14-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Amy Suggests More Even Sampling than IID

µ =

ż

[0,1]d

f(x) dx « ^µn =

1

n

nÿ

i=1

f(xi),

xi Sobol’ (Dick and Pillichshammer, 2010)

Normally n should be a power of 2

8/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-15-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Amy Suggests More Even Sampling than IID

µ =

ż

[0,1]d

f(x) dx « ^µn =

1

n

nÿ

i=1

f(xi),

xi Sobol’ (Dick and Pillichshammer, 2010)

Normally n should be a power of 2

8/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-16-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Amy Suggests More Even Sampling than IID

µ =

ż

[0,1]d

f(x) dx « ^µn =

1

n

nÿ

i=1

f(xi),

xi Sobol’ (Dick and Pillichshammer, 2010)

Normally n should be a power of 2

8/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-17-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Amy Suggests More Even Sampling than IID

µ =

ż

[0,1]d

f(x) dx « ^µn =

1

n

nÿ

i=1

f(xi),

xi Sobol’ (Dick and Pillichshammer, 2010)

Normally n should be a power of 2

8/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-18-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Amy Suggests More Even Sampling than IID

µ =

ż

[0,1]d

f(x) dx « ^µn =

1

n

nÿ

i=1

f(xi),

xi Sobol’ (Dick and Pillichshammer, 2010)

Normally n should be a power of 2

8/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-19-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Amy Suggests More Even Sampling than IID

µ =

ż

[0,1]d

f(x) dx « ^µn =

1

n

nÿ

i=1

f(xi),

xi Sobol’ (Dick and Pillichshammer, 2010)

Normally n should be a power of 2

8/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-20-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Amy Suggests More Even Sampling than IID

µ =

ż

[0,1]d

f(x) dx « ^µn =

1

n

nÿ

i=1

f(xi),

xi Sobol’ (Dick and Pillichshammer, 2010)

Normally n should be a power of 2

8/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-21-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Amy Suggests More Even Sampling than IID

µ =

ż

[0,1]d

f(x) dx « ^µn =

1

n

nÿ

i=1

f(xi),

xi Sobol’ (Dick and Pillichshammer, 2010)

Normally n should be a power of 2

8/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-22-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Amy Suggests More Even Sampling than IID

µ =

ż

[0,1]d

f(x) dx « ^µn =

1

n

nÿ

i=1

f(xi),

xi Sobol’ (Dick and Pillichshammer, 2010)

Normally n should be a power of 2

8/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-23-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Amy Suggests More Even Sampling than IID

µ =

ż

[0,1]d

f(x) dx « ^µn =

1

n

nÿ

i=1

f(xi),

xi Sobol’ (Dick and Pillichshammer, 2010)

Normally n should be a power of 2

8/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-24-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Amy Suggests More Even Sampling than IID

µ =

ż

[0,1]d

f(x) dx « ^µn =

1

n

nÿ

i=1

f(xi),

xi Sobol’ (Dick and Pillichshammer, 2010)

Normally n should be a power of 2

8/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-25-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Amy Suggests More Even Sampling than IID

µ =

ż

[0,1]d

f(x) dx « ^µn =

1

n

nÿ

i=1

f(xi),

xi Sobol’ (Dick and Pillichshammer, 2010)

Normally n should be a power of 2

8/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-26-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Amy Suggests More Even Sampling than IID

µ =

ż

[0,1]d

f(x) dx « ^µn =

1

n

nÿ

i=1

f(xi),

xi Sobol’ (Dick and Pillichshammer, 2010)

Normally n should be a power of 2

8/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-27-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Amy Suggests More Even Sampling than IID

µ =

ż

[0,1]d

f(x) dx « ^µn =

1

n

nÿ

i=1

f(xi),

xi Sobol’ (Dick and Pillichshammer, 2010)

Assume f P Hilbert space H with

reproducing kernel K (H., 1998)

µ(f) ´ ^µ(f) = xerr-rep, fy

= cos(err-rep, f) ˆ err-rep Hlooooomooooon

discrepancy

=O(n´1+

)

ˆ f H

err-rep

2

H =

ż

[0,1]2d

K(x, t) dxdt ´

2

n

nÿ

i=1

ż

[0,1]d

K(xi, t) dt +

1

n2

nÿ

i,j=1

K(xi, xj)

Adaptive stopping criteria developed (H. and Jiménez Rugama, 2016; Jiménez

Rugama and H., 2016; H. et al., 2017+). More

8/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-28-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Sobol’ Sampling Converges Faster

µ =

ż

[a,b]

exp ´1

2 tT

Σ´1

t

a

(2π)d det(Σ)

dt

Genz (1993)

=

ż

[0,1]d´1

f(x) dx

For some typical choice of a, b, Σ, d = 3; µ « 0.6763

Rel. Error Median Worst 10% Worst 10%

Tolerance Method Error Accuracy n Time (s)

1E´2 IID Affine 7E´4 100% 1.5E6 1.8E´1

1E´2 IID Genz 4E´4 100% 8.1E4 1.9E´2

1E´2 Sobol’ Genz 3E´4 100% 1.0E3 4.6E´3

1E´3 IID Genz 7E´5 100% 2.0E6 3.8E´1

1E´3 Sobol’ Genz 2E´4 100% 2.0E3 6.1E´3

9/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-29-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Sue Randomizes Even Sampling

µ =

ż

[0,1]d

f(x) dx « ^µn =

1

n

nÿ

i=1

f(xi),

xi scrambled Sobol’ (Owen, 1997a; 1997b)

Normally n should be a power of 2

E(^µ) = µ no bias

std(^µ) = n´1.5+

for scrambled Sobol’

10/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-30-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Sue Randomizes Even Sampling

µ =

ż

[0,1]d

f(x) dx « ^µn =

1

n

nÿ

i=1

f(xi),

xi scrambled Sobol’ (Owen, 1997a; 1997b)

Normally n should be a power of 2

E(^µ) = µ no bias

std(^µ) = n´1.5+

for scrambled Sobol’

10/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-31-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Sue Randomizes Even Sampling

µ =

ż

[0,1]d

f(x) dx « ^µn =

1

n

nÿ

i=1

f(xi),

xi scrambled Sobol’ (Owen, 1997a; 1997b)

Normally n should be a power of 2

E(^µ) = µ no bias

std(^µ) = n´1.5+

for scrambled Sobol’

10/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-32-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Sue Randomizes Even Sampling

µ =

ż

[0,1]d

f(x) dx « ^µn =

1

n

nÿ

i=1

f(xi),

xi scrambled Sobol’ (Owen, 1997a; 1997b)

Normally n should be a power of 2

E(^µ) = µ no bias

std(^µ) = n´1.5+

for scrambled Sobol’

10/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-33-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Sue Randomizes Even Sampling

µ =

ż

[0,1]d

f(x) dx « ^µn =

1

n

nÿ

i=1

f(xi),

xi scrambled Sobol’ (Owen, 1997a; 1997b)

Normally n should be a power of 2

E(^µ) = µ no bias

std(^µ) = n´1.5+

for scrambled Sobol’

10/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-34-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Sue Randomizes Even Sampling

µ =

ż

[0,1]d

f(x) dx « ^µn =

1

n

nÿ

i=1

f(xi),

xi scrambled Sobol’ (Owen, 1997a; 1997b)

Normally n should be a power of 2

E(^µ) = µ no bias

std(^µ) = n´1.5+

for scrambled Sobol’

10/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-35-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Sue Randomizes Even Sampling

µ =

ż

[0,1]d

f(x) dx « ^µn =

1

n

nÿ

i=1

f(xi),

xi scrambled Sobol’ (Owen, 1997a; 1997b)

Normally n should be a power of 2

E(^µ) = µ no bias

std(^µ) = n´1.5+

for scrambled Sobol’

10/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-36-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Sue Randomizes Even Sampling

µ =

ż

[0,1]d

f(x) dx « ^µn =

1

n

nÿ

i=1

f(xi),

xi scrambled Sobol’ (Owen, 1997a; 1997b)

Normally n should be a power of 2

E(^µ) = µ no bias

std(^µ) = n´1.5+

for scrambled Sobol’

10/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-37-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Sue Randomizes Even Sampling

µ =

ż

[0,1]d

f(x) dx « ^µn =

1

n

nÿ

i=1

f(xi),

xi scrambled Sobol’ (Owen, 1997a; 1997b)

Normally n should be a power of 2

E(^µ) = µ no bias

std(^µ) = n´1.5+

for scrambled Sobol’

10/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-38-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Sue Randomizes Even Sampling

µ =

ż

[0,1]d

f(x) dx « ^µn =

1

n

nÿ

i=1

f(xi),

xi scrambled Sobol’ (Owen, 1997a; 1997b)

Normally n should be a power of 2

E(^µ) = µ no bias

std(^µ) = n´1.5+

for scrambled Sobol’

10/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-39-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Sue Randomizes Even Sampling

µ =

ż

[0,1]d

f(x) dx « ^µn =

1

n

nÿ

i=1

f(xi),

xi scrambled Sobol’ (Owen, 1997a; 1997b)

Normally n should be a power of 2

E(^µ) = µ no bias

std(^µ) = n´1.5+

for scrambled Sobol’

10/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-40-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Sue Randomizes Even Sampling

µ =

ż

[0,1]d

f(x) dx « ^µn =

1

n

nÿ

i=1

f(xi),

xi scrambled Sobol’ (Owen, 1997a; 1997b)

Normally n should be a power of 2

E(^µ) = µ no bias

std(^µ) = n´1.5+

for scrambled Sobol’

10/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-41-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Sue Randomizes Even Sampling

µ =

ż

[0,1]d

f(x) dx « ^µn =

1

n

nÿ

i=1

f(xi),

xi scrambled Sobol’ (Owen, 1997a; 1997b)

Normally n should be a power of 2

E(^µ) = µ no bias

std(^µ) = n´1.5+

for scrambled Sobol’

10/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-42-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Sue Randomizes Even Sampling

µ =

ż

[0,1]d

f(x) dx « ^µn =

1

n

nÿ

i=1

f(xi),

xi scrambled Sobol’ (Owen, 1997a; 1997b)

Normally n should be a power of 2

E(^µ) = µ no bias

std(^µ) = n´1.5+

for scrambled Sobol’

10/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-43-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Sue Randomizes Even Sampling

µ =

ż

[0,1]d

f(x) dx « ^µn =

1

n

nÿ

i=1

f(xi),

xi scrambled Sobol’ (Owen, 1997a; 1997b)

or shifted lattice (Cranley and Patterson, 1976)

Normally n should be a power of 2

E(^µ) = µ no bias

std(^µ) = n´1+

for shifted lattices

10/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-44-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Sue Randomizes Even Sampling

µ =

ż

[0,1]d

f(x) dx « ^µn =

1

n

nÿ

i=1

f(xi),

xi scrambled Sobol’ (Owen, 1997a; 1997b)

or shifted lattice (Cranley and Patterson, 1976)

Normally n should be a power of 2

E(^µ) = µ no bias

std(^µ) = n´1+

for shifted lattices

10/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-45-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Scrambled Sobol’ Is Better

µ =

ż

[a,b]

exp ´1

2 tT

Σ´1

t

a

(2π)d det(Σ)

dt

Genz (1993)

=

ż

[0,1]d´1

f(x) dx

For some typical choice of a, b, Σ, d = 3; µ « 0.6763

Rel. Error Median Worst 10% Worst 10%

Tolerance Method Error Accuracy n Time (s)

1E´2 IID Affine 7E´4 100% 1.5E6 1.8E´1

1E´2 IID Genz 4E´4 100% 8.1E4 1.9E´2

1E´2 Sobol’ Genz 3E´4 100% 1.0E3 4.6E´3

1E´2 Scr. Sobol’ Genz 6E´5 100% 1.0E3 5.0E´3

1E´3 IID Genz 7E´5 100% 2.0E6 3.8E´1

1E´3 Sobol’ Genz 2E´4 100% 2.0E3 6.1E´3

1E´3 Scr. Sobol’ Genz 2E´5 100% 2.0E3 6.7E´3

1E´4 Scr. Sobol’ Genz 5E´7 100% 1.6E4 1.9E´2

11/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-46-320.jpg)

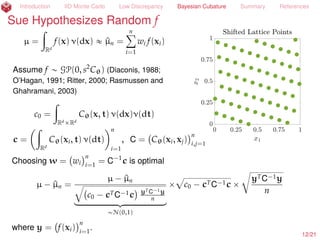

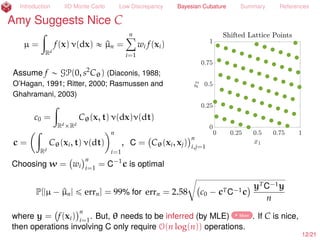

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Amy Suggests Nice C

µ =

ż

Rd

f(x) ρ(x) dx « ^µn =

nÿ

i=1

wi f(xi)

Assume f „ GP(0, s2

Cθ) (Diaconis, 1988;

O’Hagan, 1991; Ritter, 2000; Rasmussen and

Ghahramani, 2003)

c0 =

ż

RdˆRd

Cθ(x, t) ρ(x)ρ(t) dxdt

c =

ż

Rd

Cθ(xi, t) ρ(x) dx

n

i=1

, C = Cθ(xi, xj)

n

i,j=1

Choosing w = wi

n

i=1

= C´1

c is optimal

P[|µ ´ ^µn| ď errn] = 99% for errn = 2.58

c

c0 ´ cTC´1c

yTC´1y

n

where y = f(xi)

n

i=1

. But, θ needs to be inferred (by MLE) More . If C is nice,

then operations involving C only require O(n log(n)) operations.

13/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-51-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Bayesian Cubature Is Promising

µ =

ż

[a,b]

exp ´1

2 tT

Σ´1

t

a

(2π)d det(Σ)

dt

Genz (1993)

=

ż

[0,1]d´1

f(x) dx

For some typical choice of a, b, Σ, d = 3; µ « 0.6763

Rel. Error Median Worst 10% Worst 10%

Tolerance Method Error Accuracy n Time (s)

1E´2 IID Affine 7E´4 100% 1.5E6 1.8E´1

1E´2 IID Genz 4E´4 100% 8.1E4 1.9E´2

1E´2 Sobol’ Genz 3E´4 100% 1.0E3 4.6E´3

1E´2 Scr. Sobol’ Genz 6E´5 100% 1.0E3 5.0E´3

1E´2 Bayes. Latt. Genz 1E´5 100% 1.0E3 3.7E´3

1E´3 IID Genz 7E´5 100% 2.0E6 3.8E´1

1E´3 Sobol’ Genz 2E´4 100% 2.0E3 6.1E´3

1E´3 Scr. Sobol’ Genz 2E´5 100% 2.0E3 6.7E´3

1E´3 Bayes. Latt. Genz 9E´6 100% 1.0E3 2.6E´3

1E´4 Scr. Sobol’ Genz 5E´7 100% 1.6E4 1.9E´2

1E´4 Bayes. Latt. Genz 5E´7 100% 8.2E3 1.3E´2

14/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-52-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

References II

H., F. J. and Ll. A. Jiménez Rugama. 2016. Reliable adaptive cubature using digital sequences,

Monte Carlo and quasi-Monte Carlo methods: MCQMC, Leuven, Belgium, April 2014, pp. 367–383.

arXiv:1410.8615 [math.NA].

H., F. J., Ll. A. Jiménez Rugama, and D. Li. 2017+. Adaptive quasi-Monte Carlo methods. submitted

for publication, arXiv:1702.01491 [math.NA].

H., F. J., C. Lemieux, and A. B. Owen. 2005. Control variates for quasi-Monte Carlo, Statist. Sci. 20,

1–31.

Jiang, L. 2016. Guaranteed adaptive Monte Carlo methods for estimating means of random

variables, Ph.D. Thesis.

Jiménez Rugama, Ll. A. and F. J. H. 2016. Adaptive multidimensional integration based on rank-1

lattices, Monte Carlo and quasi-Monte Carlo methods: MCQMC, Leuven, Belgium, April 2014,

pp. 407–422. arXiv:1411.1966.

Meng, X. 2017+. Statistical paradises and paradoxes in big data. in preparation.

O’Hagan, A. 1991. Bayes-Hermite quadrature, J. Statist. Plann. Inference 29, 245–260.

Owen, A. B. 1997a. Monte Carlo variance of scrambled net quadrature, SIAM J. Numer. Anal. 34,

1884–1910.

. 1997b. Scrambled net variance for integrals of smooth functions, Ann. Stat. 25, 1541–1562.

Rasmussen, C. E. and Z. Ghahramani. 2003. Bayesian Monte Carlo, Advances in Neural Information

Processing Systems, pp. 489–496.

19/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-57-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Sue Suggests IID Monte Carlo

µ = E[f(X)] =

ż

Rd

f(x) ρ(x) dx

« ^µn =

1

n

nÿ

i=1

f(xi), xi

IID

„ ρ

P[|µ ´ ^µn| ď errn] ě 99%

for Φ ´

?

n errn /(1.2^σnσ

)

+ ∆n(´

?

n errn /(1.2^σnσ

), κmax) = 0.0025

by the Berry-Esseen Inequality,

where ^σ2

nσ

is the sample variance using an independent sample from that used to

simulate the mean, and provided that kurt(f(X)) ď κmax(nσ) (H. et al., 2013;

Jiang, 2016). Return

21/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-59-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Amy Suggests More Even Sampling than IID

µ =

ż

[0,1]d

f(x) dx « ^µn =

1

n

nÿ

i=1

f(xi),

xi Sobol’ (Dick and Pillichshammer, 2010)

Assume f P Hilbert space H with

reproducing kernel K (H., 1998)

µ(f) ´ ^µ(f) = xerr-rep, fy

= cos(err-rep, f) ˆ err-rep Hlooooomooooon

discrepancy

=O(n´1+

)

ˆ f H

err-rep

2

H =

ż

[0,1]2d

K(x, t) dxdt ´

2

n

nÿ

i=1

ż

[0,1]d

K(xi, t) dt +

1

n2

nÿ

i,j=1

K(xi, xj)

E.g., K(x, t) =

dź

k=1

1 + γ2

kt1 ´ |xk ´ tk|u ,

1

γu

B|u|

f

Bxu xsu=1 L2

u‰H 2

, γu =

ź

kPu

γk

22/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-60-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Amy Suggests More Even Sampling than IID

µ =

ż

[0,1]d

f(x) dx « ^µn =

1

n

nÿ

i=1

f(xi),

xi Sobol’ (Dick and Pillichshammer, 2010)

Let pf(k)

(

k

denote the coefficients of the

Fourier Walsh expansion of f. Let tω(k)uk

be some weights. Then

µ ´ ^µn =

´

ÿ

0‰kPdual

pf(k)

! pf(k)

ω(k)

)

k 2

tω(k)u0‰kPdual 2

loooooooooooooooooooomoooooooooooooooooooon

ALNP[´1,1]

ˆ tω(k)u0‰kPdual 2loooooooooomoooooooooon

DSC(txiun

i=1)=O(n´1+ )

ˆ

#

pf(k)

ω(k)

+

k 2looooooomooooooon

VAR(f)

22/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-61-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Amy Suggests More Even Sampling than IID

µ =

ż

[0,1]d

f(x) dx « ^µn =

1

n

nÿ

i=1

f(xi),

xi Sobol’ (Dick and Pillichshammer, 2010)

Let pf(k)

(

k

denote the coefficients of the

Fourier Walsh expansion of f. Let tω(k)uk

be some weights. Then

Assuming that the pf(k) do not decay erratically as k Ñ ∞, the discrete

transform, rfn(k)

(

k

, may be used to bound the error reliably (H. and Jiménez

Rugama, 2016; Jiménez Rugama and H., 2016; H. et al., 2017+):

|µ ´ ^µn| ď errn := C(n)

ÿ

certaink

rfn(k)

Return

22/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-62-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Maximum Likelihood Estimation of the Covariance Kernel

f „ GP(0, s2

Cθ), Cθ = Cθ(xi, xj)

n

i,j=1

y = f(xi)

n

i=1

, ^µn = cT

^θ

C´1

^θ

y

^θ = argmin

θ

yT

C´1

θ y

[det(C´1

θ )]1/n

P[|µ ´ ^µn| ď errn] = 99% for errn =

2.58

?

n

b

c0,^θ ´ cT

^θ

C´1

^θ

c^θ yTC´1

^θ

y

23/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-63-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Maximum Likelihood Estimation of the Covariance Kernel

f „ GP(0, s2

Cθ), Cθ = Cθ(xi, xj)

n

i,j=1

y = f(xi)

n

i=1

, ^µn = cT

^θ

C´1

^θ

y

^θ = argmin

θ

yT

C´1

θ y

[det(C´1

θ )]1/n

P[|µ ´ ^µn| ď errn] = 99% for errn =

2.58

?

n

b

c0,^θ ´ cT

^θ

C´1

^θ

c^θ yTC´1

^θ

y

There is a de-randomized interpretation of Bayesian cubature (H., 2017+)

f P Hilbert space w/ reproducing kernel Cθ and with best interpolant rfy

Return 23/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-64-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Maximum Likelihood Estimation of the Covariance Kernel

f „ GP(0, s2

Cθ), Cθ = Cθ(xi, xj)

n

i,j=1

y = f(xi)

n

i=1

, ^µn = cT

^θ

C´1

^θ

y

^θ = argmin

θ

yT

C´1

θ y

[det(C´1

θ )]1/n

P[|µ ´ ^µn| ď errn] = 99% for errn =

2.58

?

n

b

c0,^θ ´ cT

^θ

C´1

^θ

c^θ yTC´1

^θ

y

There is a de-randomized interpretation of Bayesian cubature (H., 2017+)

f P Hilbert space w/ reproducing kernel Cθ and with best interpolant rfy

|µ ´ ^µn| ď

2.58

?

n

b

c0,^θ ´ cT

^θ

C´1

^θ

c^θ

loooooooooomoooooooooon

error representer ^θ

b

yTC´1

^θ

y

looooomooooon

rfy ^θ

if f ´ rfy ^θ

ď

2.58 rf ^θ?

n

Return 23/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-65-320.jpg)

![Introduction IID Monte Carlo Low Discrepancy Bayesian Cubature Summary References

Maximum Likelihood Estimation of the Covariance Kernel

f „ GP(0, s2

Cθ), Cθ = Cθ(xi, xj)

n

i,j=1

y = f(xi)

n

i=1

, ^µn = cT

^θ

C´1

^θ

y

^θ = argmin

θ

yT

C´1

θ y

[det(C´1

θ )]1/n

P[|µ ´ ^µn| ď errn] = 99% for errn =

2.58

?

n

b

c0,^θ ´ cT

^θ

C´1

^θ

c^θ yTC´1

^θ

y

There is a de-randomized interpretation of Bayesian cubature (H., 2017+)

f P Hilbert space w/ reproducing kernel Cθ and with best interpolant rfy

^θ = argmin

θ

yT

C´1

θ y

[det(C´1

θ )]1/n

= argmin

θ

vol z P Rn

: rfz θ ď rfy θ

(

|µ ´ ^µn| ď

2.58

?

n

b

c0,^θ ´ cT

^θ

C´1

^θ

c^θ

loooooooooomoooooooooon

error representer ^θ

b

yTC´1

^θ

y

looooomooooon

rfy ^θ

if f ´ rfy ^θ

ď

2.58 rf ^θ?

n

Return 23/23](https://image.slidesharecdn.com/mines2017apriltalk-170406043746/85/Mines-April-2017-Colloquium-66-320.jpg)

The document discusses various computational methods for estimating option prices and Gaussian probabilities using techniques such as Monte Carlo and cubature. It evaluates the efficiency of these methods based on dimensionality and sampling strategies, noting that traditional methods can be computationally prohibitive in higher dimensions. The authors, Amy and Sue, suggest alternatives for sampling to improve accuracy and convergence rates in computations.