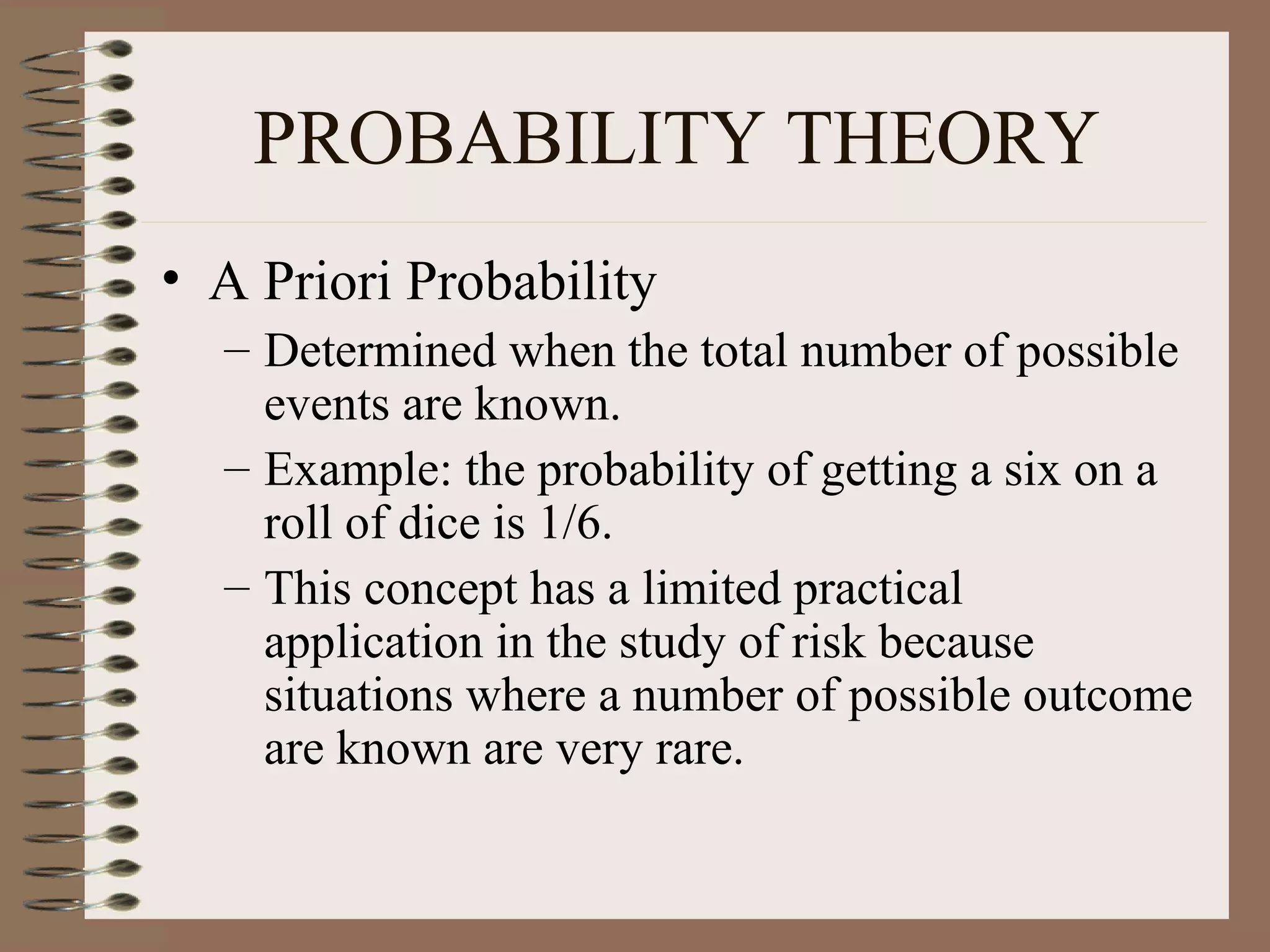

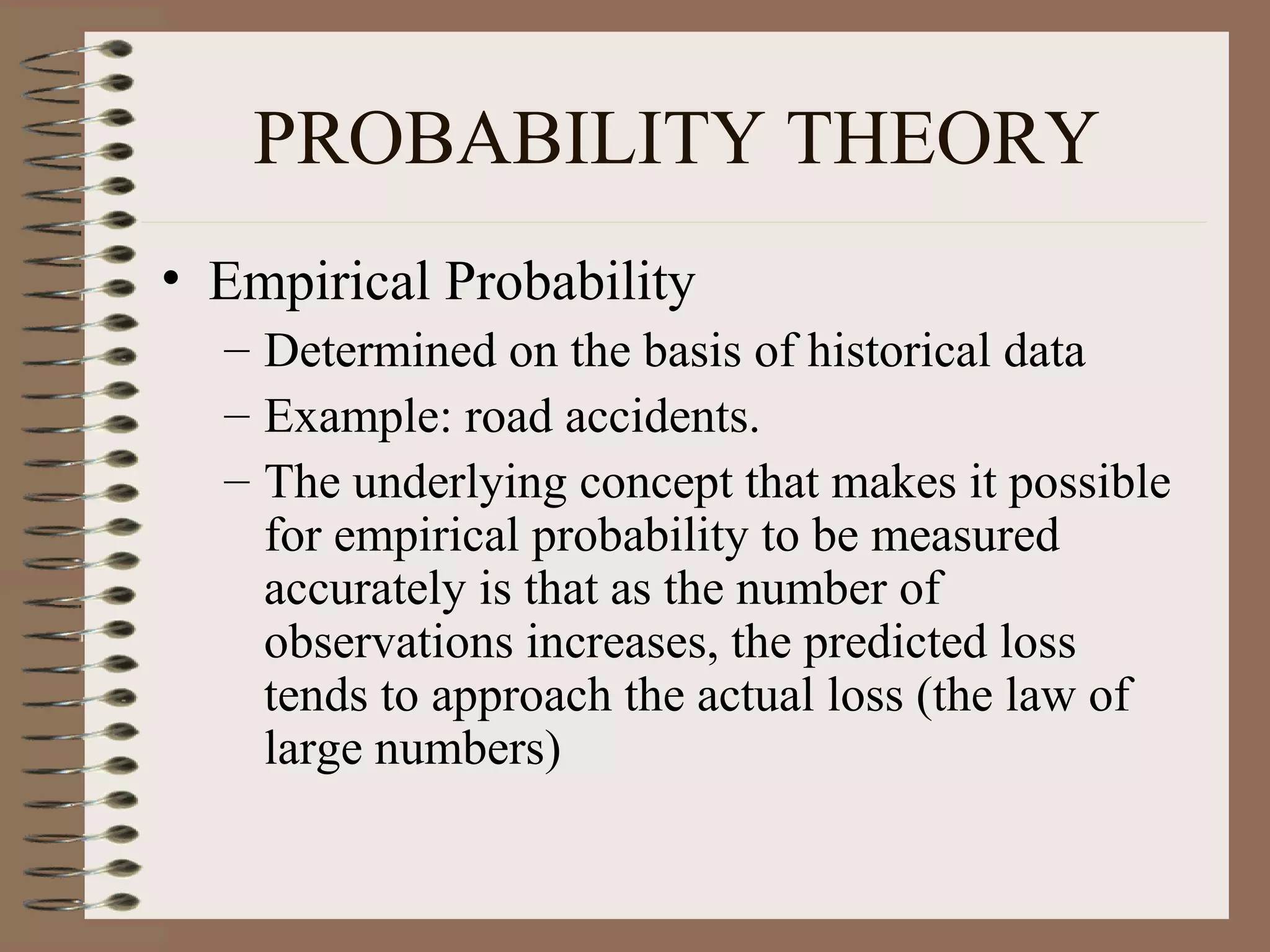

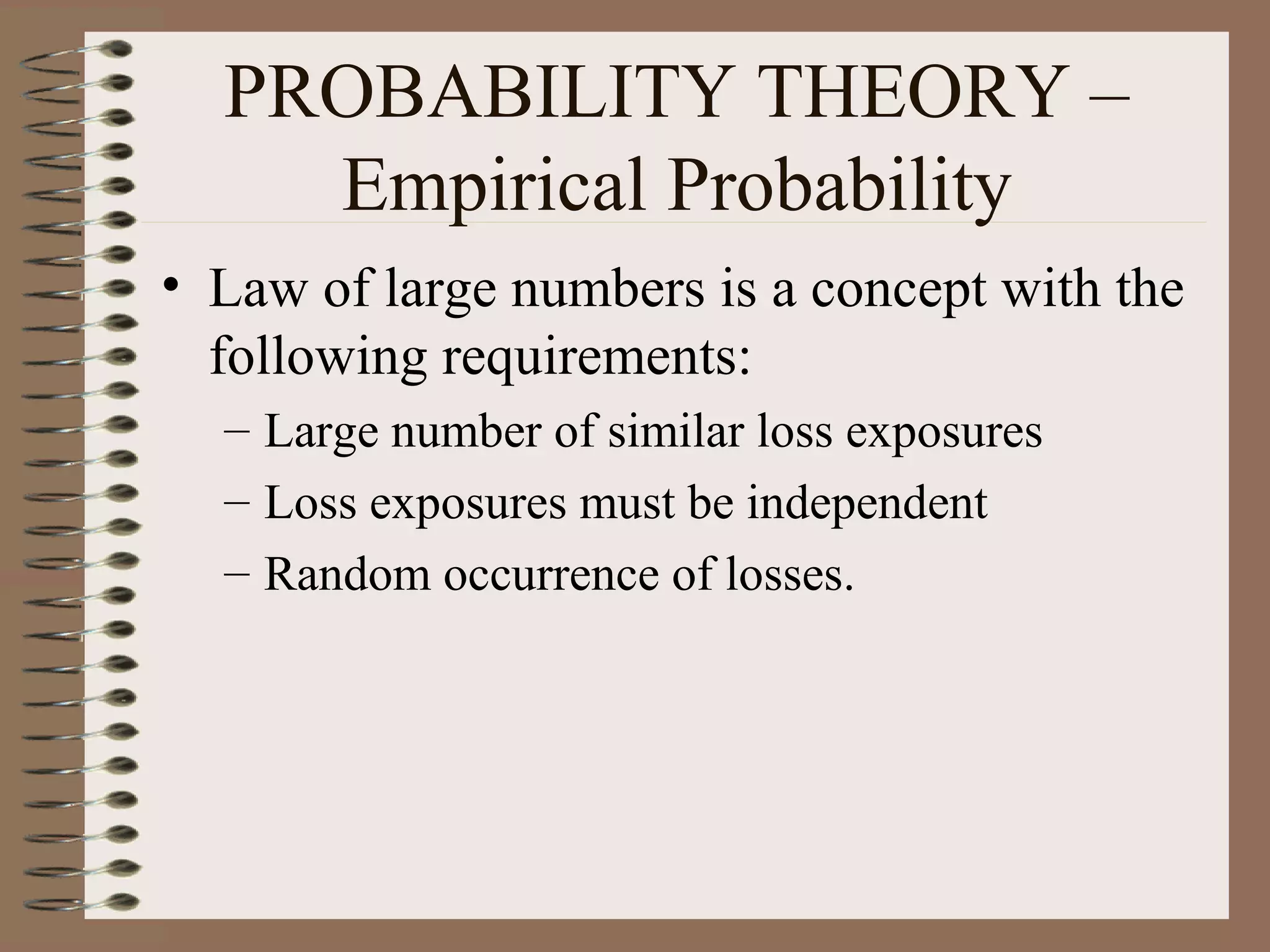

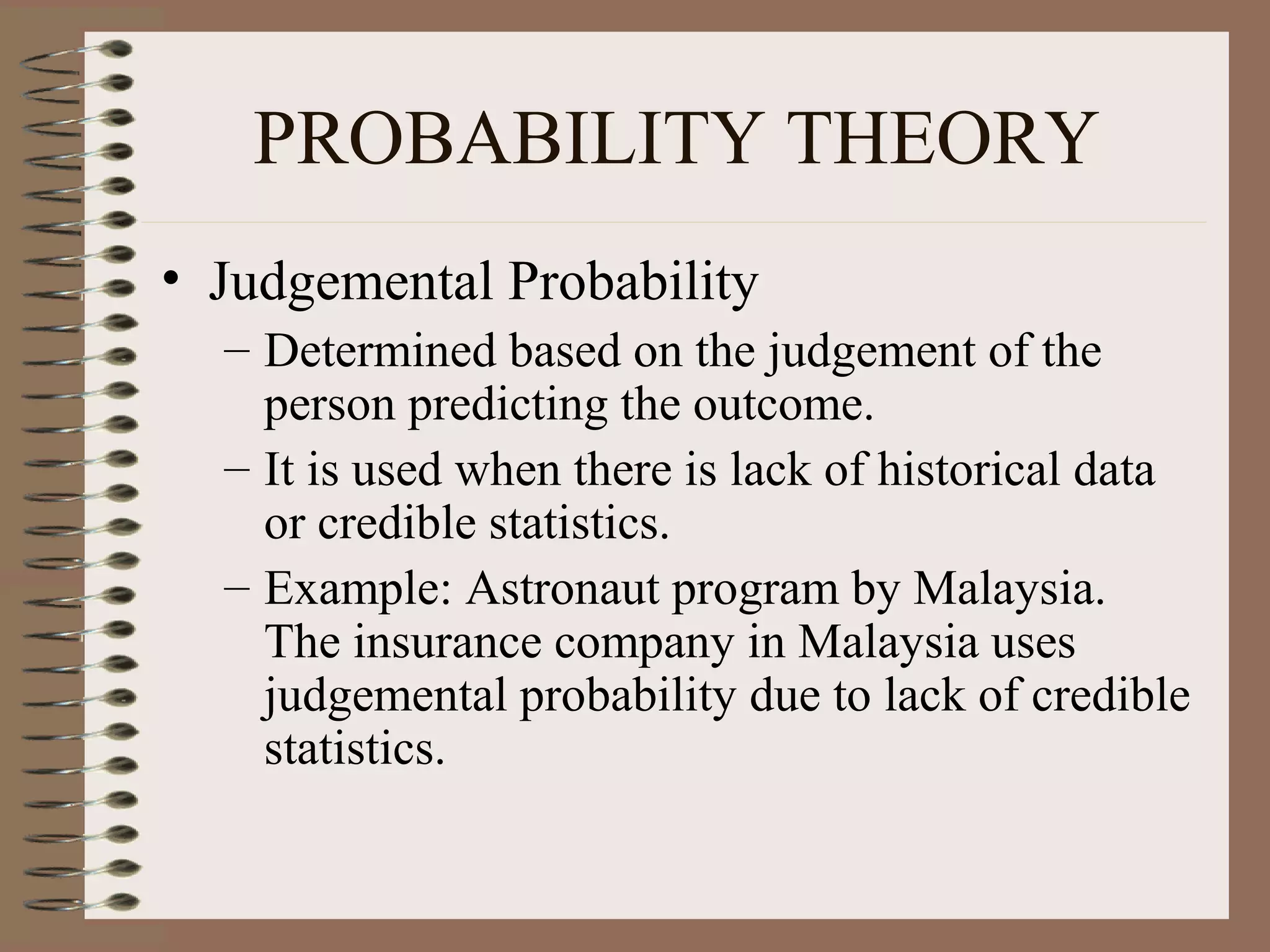

Downloaded 149 times

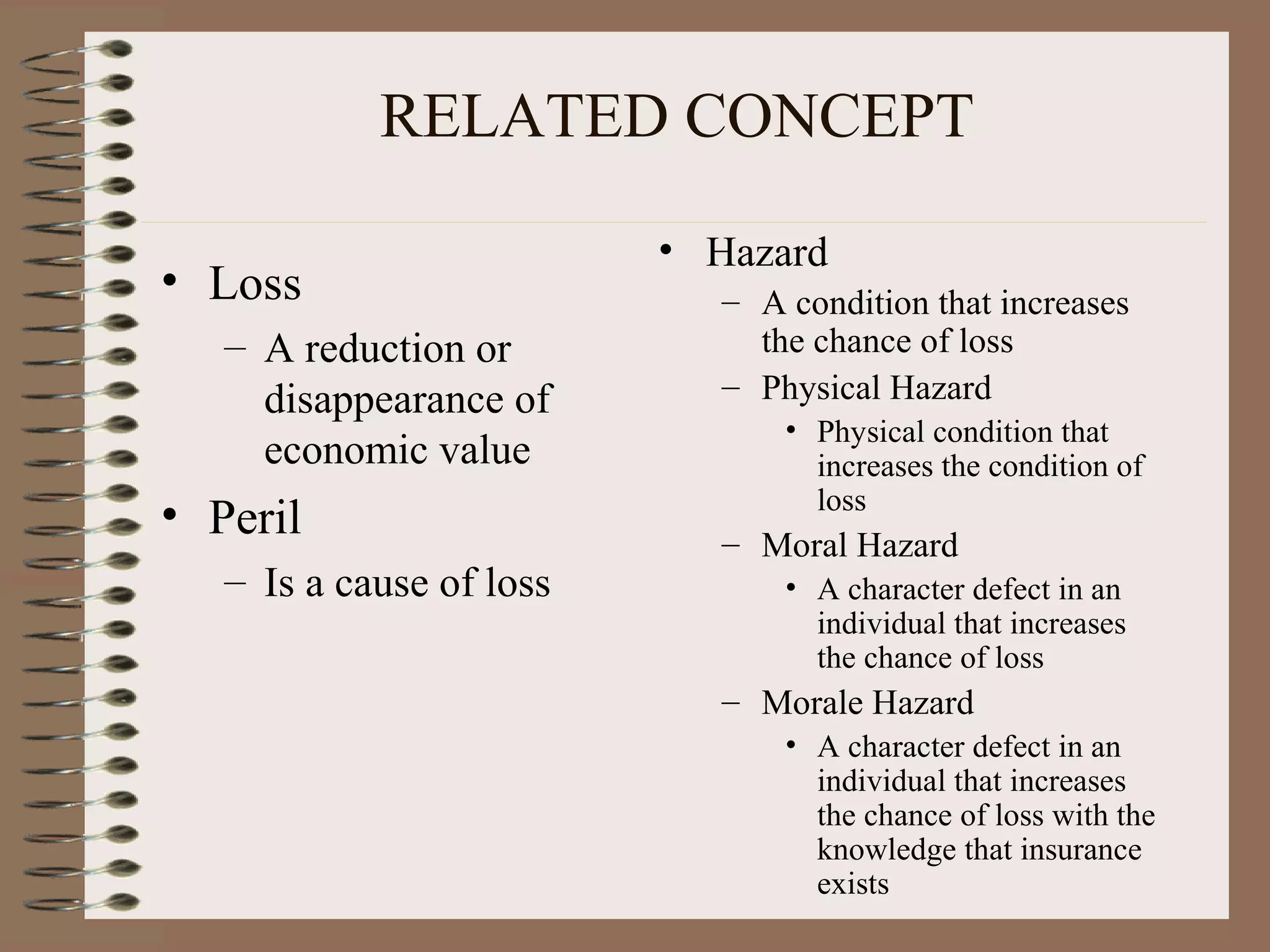

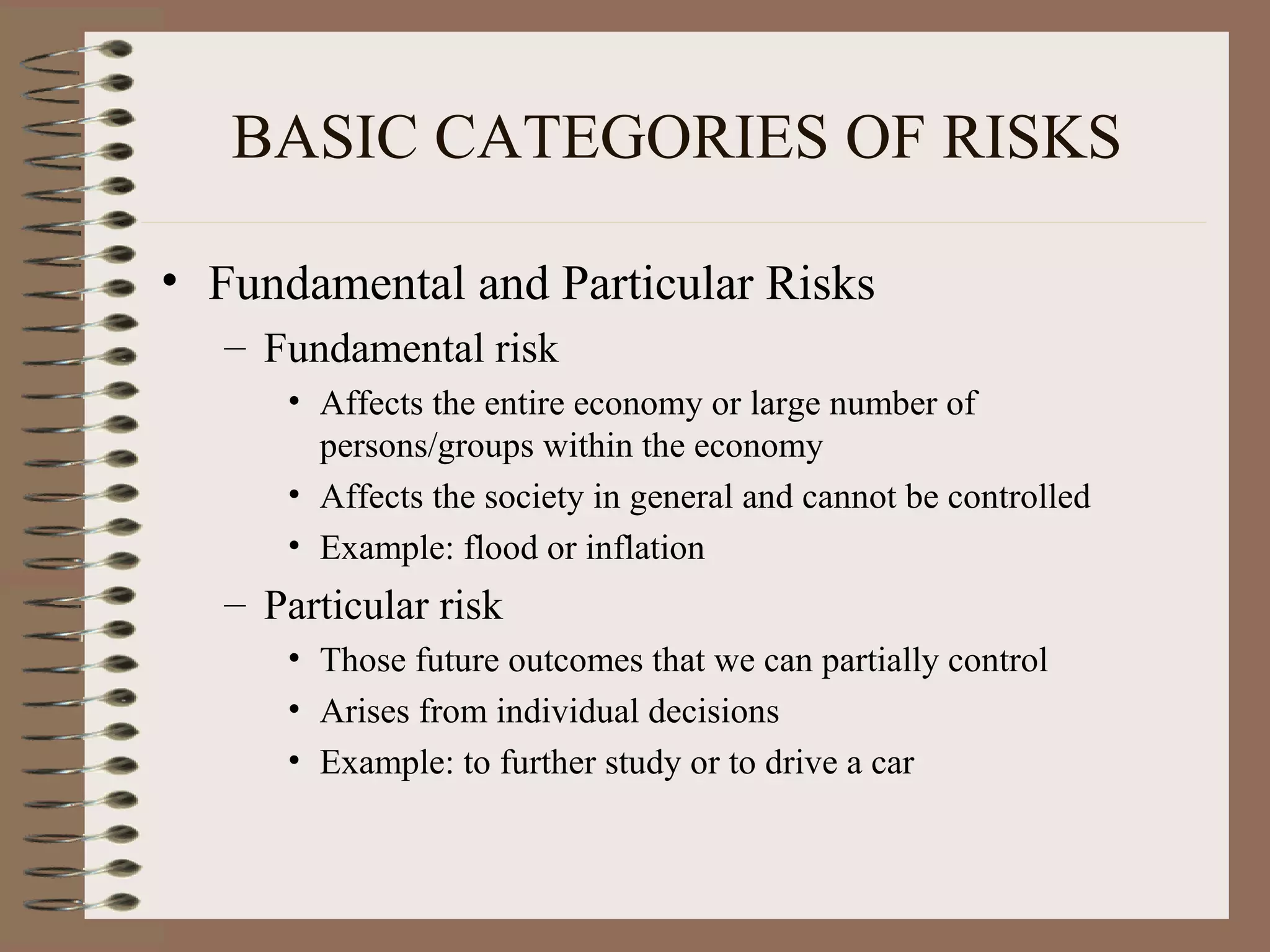

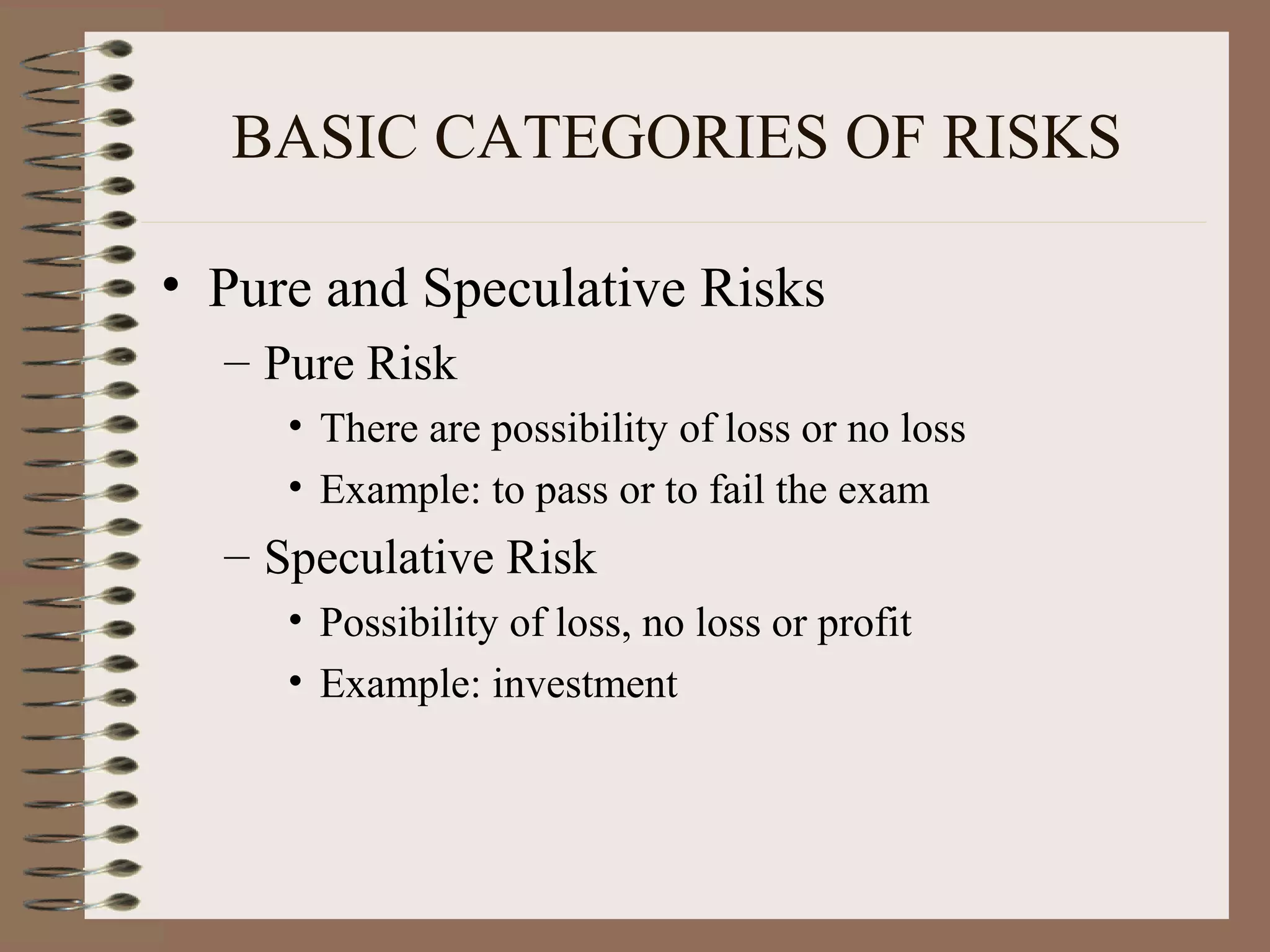

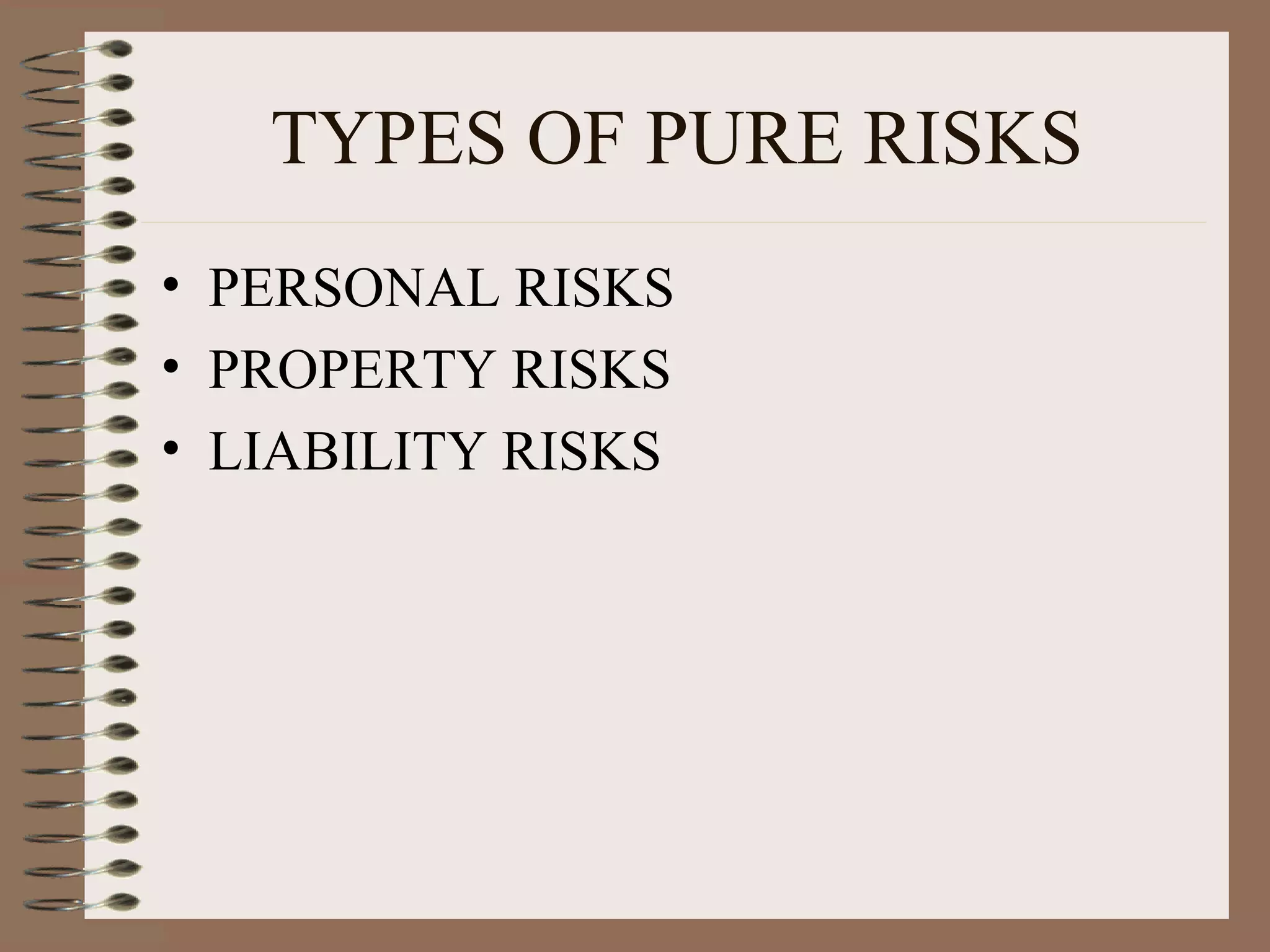

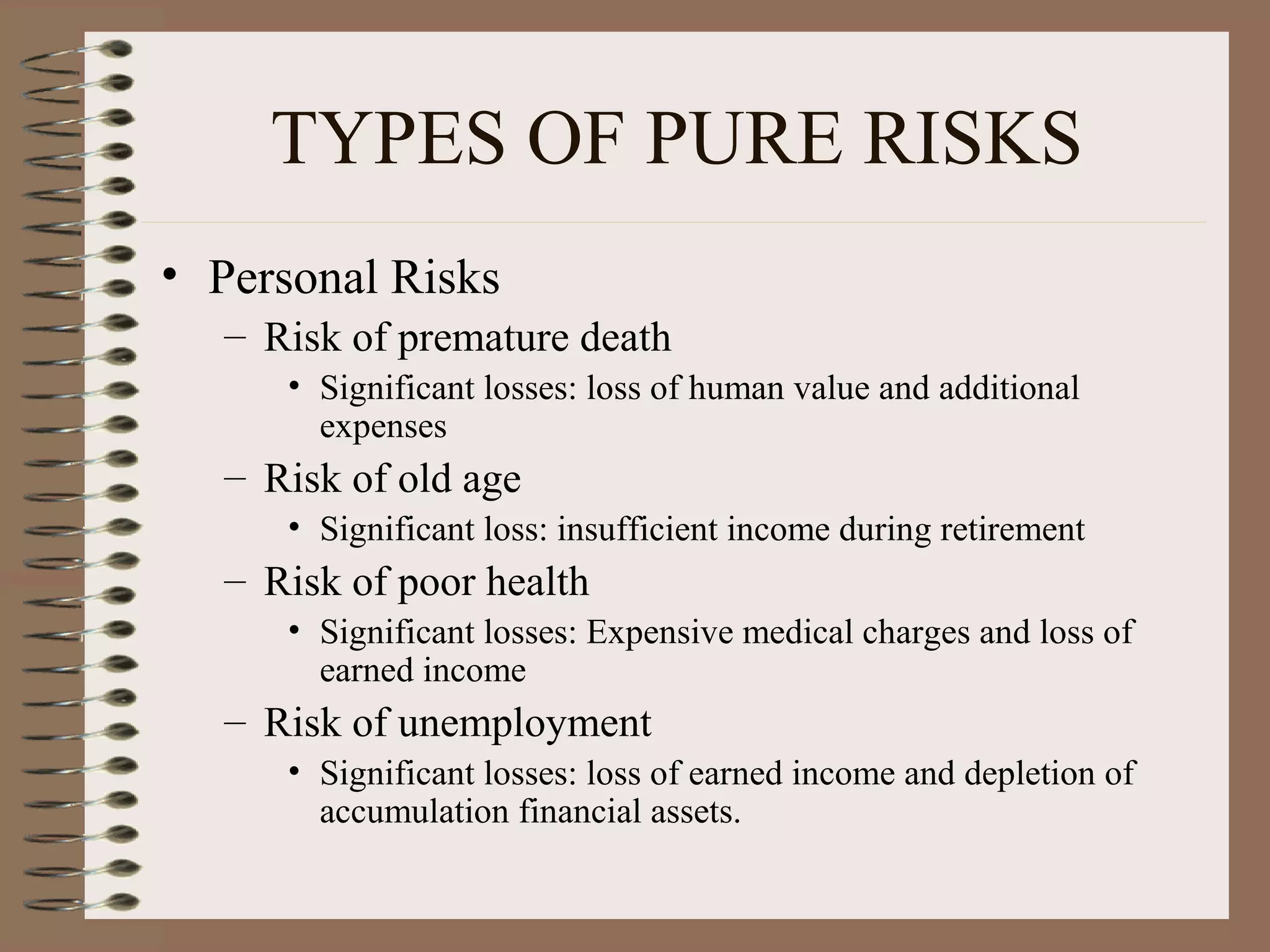

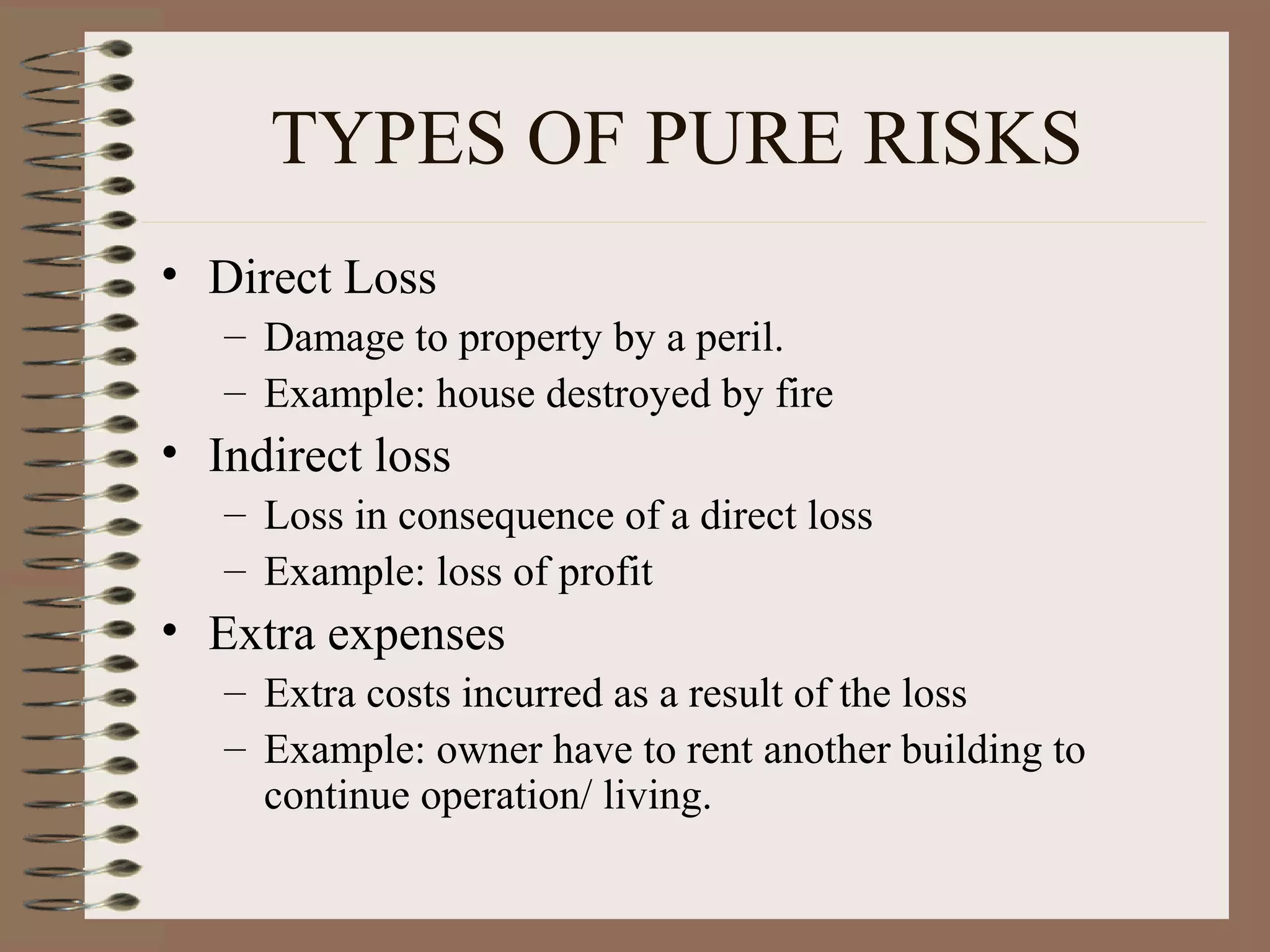

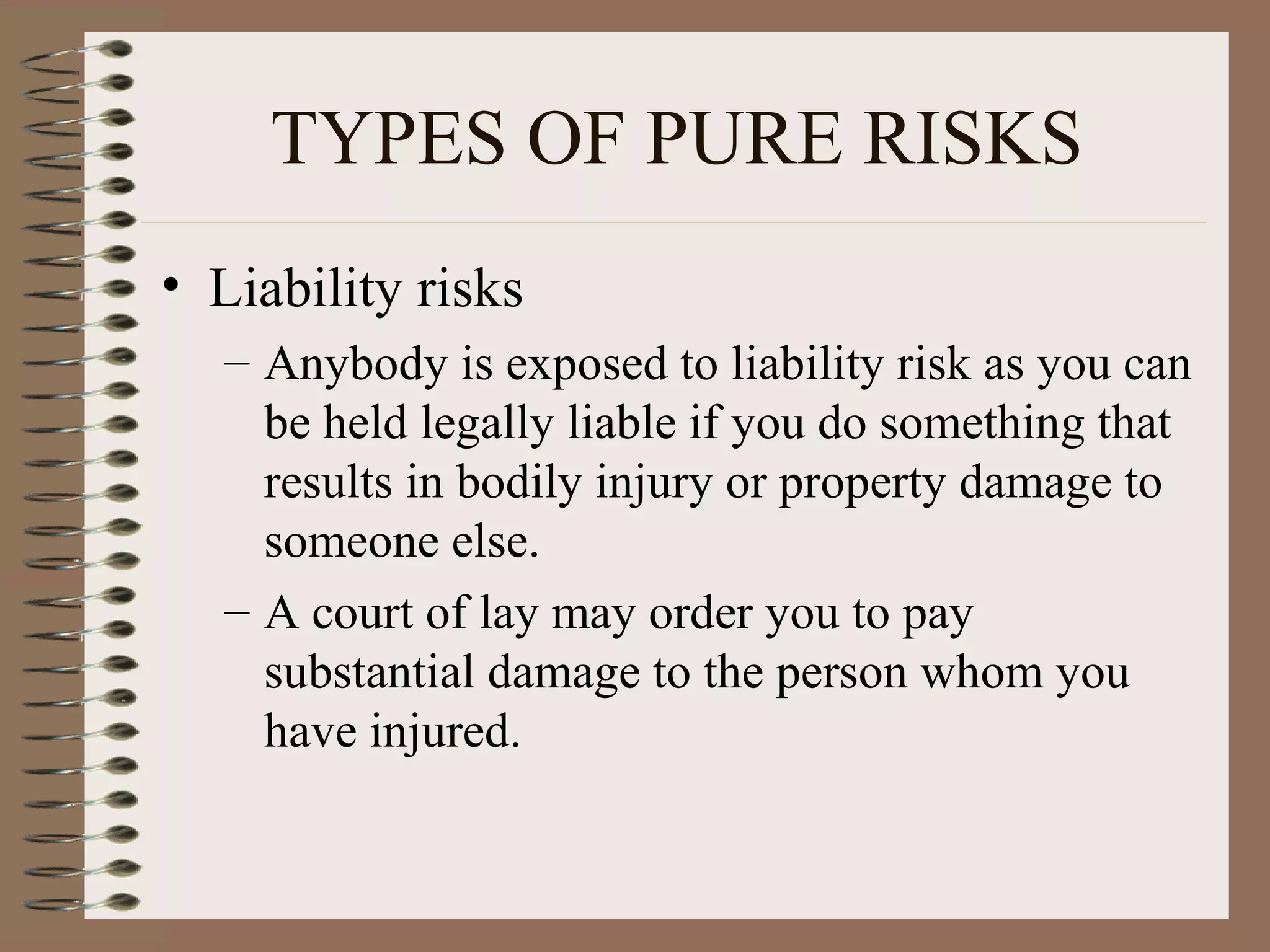

Risk is the possibility of a loss or an unfavorable outcome affecting an individual's or organization's financial state. Insurance provides compensation for losses to transfer risk. There are different ways to deal with risk including avoiding, reducing, ignoring, or transferring it. Probability can be determined a priori, empirically based on historical data, or through judgement. Risks can be fundamental to society or particular to individuals and organizations. They can also be pure risks involving only possibilities of loss or gain, or speculative risks involving profit. Common types of pure risks include personal health and financial risks, property damage risks, and legal liability risks.