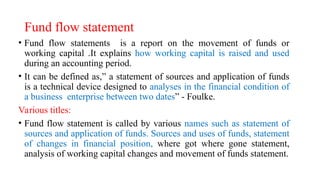

Fund flow statement

•Fund flow statements is a report on the movement of funds or

working capital .It explains how working capital is raised and used

during an accounting period.

• It can be defined as,” a statement of sources and application of funds

is a technical device designed to analyses in the financial condition of

a business enterprise between two dates” - Foulke.

Various titles:

• Fund flow statement is called by various names such as statement of

sources and application of funds. Sources and uses of funds, statement

of changes in financial position, where got where gone statement,

analysis of working capital changes and movement of funds statement.

3.

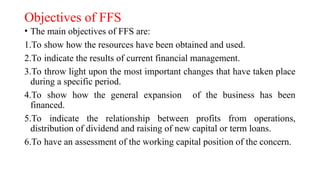

Objectives of FFS

•The main objectives of FFS are:

1.To show how the resources have been obtained and used.

2.To indicate the results of current financial management.

3.To throw light upon the most important changes that have taken place

during a specific period.

4.To show how the general expansion of the business has been

financed.

5.To indicate the relationship between profits from operations,

distribution of dividend and raising of new capital or term loans.

6.To have an assessment of the working capital position of the concern.

4.

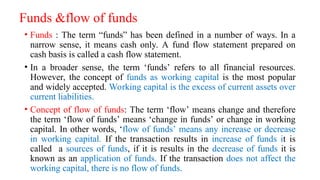

Funds &flow offunds

• Funds : The term “funds” has been defined in a number of ways. In a

narrow sense, it means cash only. A fund flow statement prepared on

cash basis is called a cash flow statement.

• In a broader sense, the term ‘funds’ refers to all financial resources.

However, the concept of funds as working capital is the most popular

and widely accepted. Working capital is the excess of current assets over

current liabilities.

• Concept of flow of funds: The term ‘flow’ means change and therefore

the term ‘flow of funds’ means ‘change in funds’ or change in working

capital. In other words, ‘flow of funds’ means any increase or decrease

in working capital. If the transaction results in increase of funds it is

called a sources of funds, if it is results in the decrease of funds it is

known as an application of funds. If the transaction does not affect the

working capital, there is no flow of funds.

5.

***

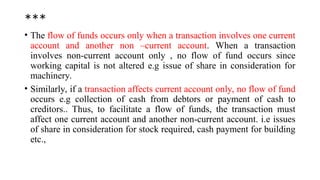

• The flowof funds occurs only when a transaction involves one current

account and another non –current account. When a transaction

involves non-current account only , no flow of fund occurs since

working capital is not altered e.g issue of share in consideration for

machinery.

• Similarly, if a transaction affects current account only, no flow of fund

occurs e.g collection of cash from debtors or payment of cash to

creditors.. Thus, to facilitate a flow of funds, the transaction must

affect one current account and another non-current account. i.e issues

of share in consideration for stock required, cash payment for building

etc.,

6.

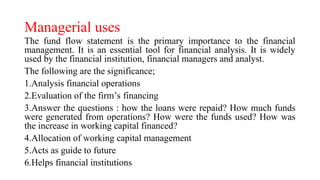

Managerial uses

The fundflow statement is the primary importance to the financial

management. It is an essential tool for financial analysis. It is widely

used by the financial institution, financial managers and analyst.

The following are the significance;

1.Analysis financial operations

2.Evaluation of the firm’s financing

3.Answer the questions : how the loans were repaid? How much funds

were generated from operations? How were the funds used? How was

the increase in working capital financed?

4.Allocation of working capital management

5.Acts as guide to future

6.Helps financial institutions

7.

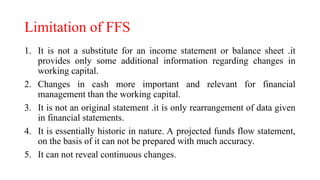

Limitation of FFS

1.It is not a substitute for an income statement or balance sheet .it

provides only some additional information regarding changes in

working capital.

2. Changes in cash more important and relevant for financial

management than the working capital.

3. It is not an original statement .it is only rearrangement of data given

in financial statements.

4. It is essentially historic in nature. A projected funds flow statement,

on the basis of it can not be prepared with much accuracy.

5. It can not reveal continuous changes.

8.

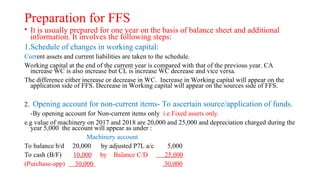

Preparation for FFS

•It is usually prepared for one year on the basis of balance sheet and additional

information. It involves the following steps:

1.Schedule of changes in working capital:

Current assets and current liabilities are taken to the schedule.

Working capital at the end of the current year is compared with that of the previous year. CA

increase WC is also increase but CL is increase WC decrease and vice versa.

The difference either increase or decrease in WC. Increase in Working capital will appear on the

application side of FFS. Decrease in Working capital will appear on the sources side of FFS.

2. Opening account for non-current items- To ascertain source/application of funds.

-By opening account for Non-current items only i.e Fixed assets only.

e.g value of machinery on 2017 and 2018 are 20,000 and 25,000 and depreciation charged during the

year 5,000 the account will appear as under :

Machinery account

To balance b/d 20,000 by adjusted P7L a/c 5,000

To cash (B/F) 10,000 by Balance C/D 25,000

(Purchase-app) 30,000 30,000

9.

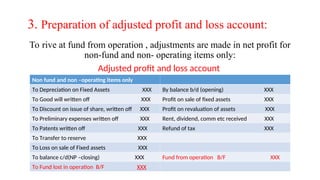

3. Preparation ofadjusted profit and loss account:

To rive at fund from operation , adjustments are made in net profit for

non-fund and non- operating items only:

Adjusted profit and loss account

Non fund and non –operating items only

To Depreciation on Fixed Assets XXX By balance b/d (opening) XXX

To Good will written off XXX Profit on sale of fixed assets XXX

To Discount on issue of share, written off XXX Profit on revaluation of assets XXX

To Preliminary expenses written off XXX Rent, dividend, comm etc received XXX

To Patents written off XXX Refund of tax XXX

To Transfer to reserve XXX

To Loss on sale of Fixed assets XXX

To balance c/d(NP –closing) XXX Fund from operation B/F XXX

To Fund lost in operation B/F XXX

10.

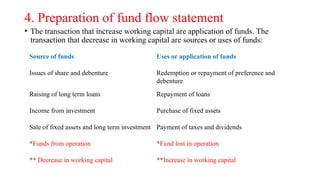

4. Preparation offund flow statement

• The transaction that increase working capital are application of funds. The

transaction that decrease in working capital are sources or uses of funds:

Source of funds Uses or application of funds

Issues of share and debenture Redemption or repayment of preference and

debenture

Raising of long term loans Repayment of loans

Income from investment Purchase of fixed assets

Sale of fixed assets and long term investment Payment of taxes and dividends

*Funds from operation *Fund lost in operation

** Decrease in working capital **Increase in working capital

11.

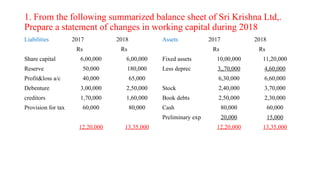

1. From thefollowing summarized balance sheet of Sri Krishna Ltd,.

Prepare a statement of changes in working capital during 2018

Liabilities 2017 2018 Assets 2017 2018

Rs Rs Rs Rs

Share capital 6,00,000 6,00,000 Fixed assets 10,00,000 11,20,000

Reserve 50,000 180,000 Less deprec 3,,70,000 4,60,000

Profit&loss a/c 40,000 65,000 6,30,000 6,60,000

Debenture 3,00,000 2,50,000 Stock 2,40,000 3,70,000

creditors 1,70,000 1,60,000 Book debts 2,50,000 2,30,000

Provision for tax 60,000 80,000 Cash 80,000 60,000

Preliminary exp 20,000 15,000

12,20,000 13,35,000 12,20,000 13,35,000

12.

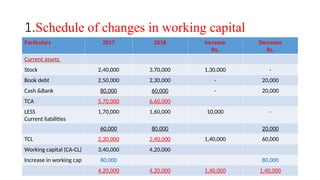

1.Schedule of changesin working capital

Particulars 2017 2018 Increase

Rs.

Decrease

Rs.

Current assets

Stock 2,40,000 3,70,000 1,30,000 -

Book debt 2,50,000 2,30,000 - 20,000

Cash &Bank 80,000 60,000 - 20,000

TCA 5,70,000 6,60,000

LESS

Current liabilities

1,70,000 1,60,000 10,000 -

60,000 80,000 20,000

TCL 2,30,000 2,40,000 1,40,000 60,000

Working capital (CA-CL) 3,40,000 4,20,000

Increase in working cap 80,000 80,000

4,20,000 4,20,000 1,40,000 1,40,000

13.

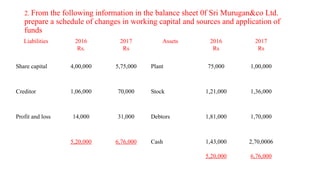

2. From thefollowing information in the balance sheet 0f Sri Murugan&co Ltd.

prepare a schedule of changes in working capital and sources and application of

funds

Liabilities 2016

Rs.

2017

Rs

Assets 2016

Rs

2017

Rs

Share capital 4,00,000 5,75,000 Plant 75,000 1,00,000

Creditor 1,06,000 70,000 Stock 1,21,000 1,36,000

Profit and loss 14,000 31,000 Debtors 1,81,000 1,70,000

5,20,000 6,76,000 Cash 1,43,000

5,20,000

2,70,0006

6,76,000

14.

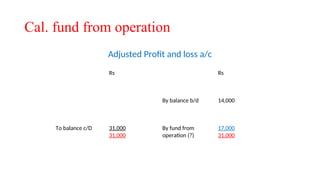

Cal. fund fromoperation

Adjusted Profit and loss a/c

Rs Rs

By balance b/d 14,000

To balance c/D 31,000

31,000

By fund from

operation (?)

17,000

31,000

15.

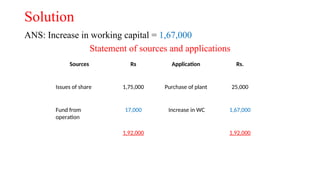

Solution

ANS: Increase inworking capital = 1,67,000

Statement of sources and applications

Sources Rs Application Rs.

Issues of share 1,75,000 Purchase of plant 25,000

Fund from

operation

17,000 Increase in WC 1,67,000

1,92,000 1,92,000

16.

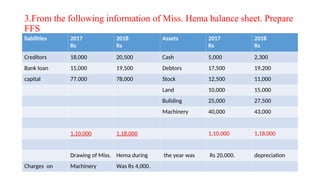

3.From the followinginformation of Miss. Hema balance sheet. Prepare

FFS

liabilities 2017

Rs

2018

Rs

Assets 2017

Rs

2018

Rs

Creditors 18,000 20,500 Cash 5,000 2,300

Bank loan 15,000 19,500 Debtors 17,500 19,200

capital 77.000 78,000 Stock 12,500 11,000

Land 10,000 15,000

Buliding 25,000 27,500

Machinery 40,000 43,000

1,10,000 1,18,000 1,10,000 1,18,000

Drawing of Miss. Hema during the year was Rs 20,000. depreciation

Charges on Machinery Was Rs 4,000.

17.

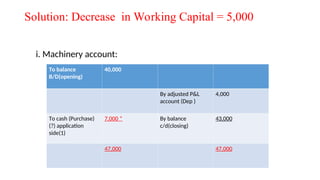

Solution: Decrease inWorking Capital = 5,000

i. Machinery account:

To balance

B/D(opening)

40,000

By adjusted P&L

account (Dep )

4,000

To cash (Purchase)

(?) application

side(1)

7,000 * By balance

c/d(closing)

43,000

47,000 47,000

18.

***

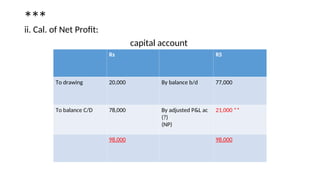

ii. Cal. ofNet Profit:

capital account

Rs RS

To drawing 20,000 By balance b/d 77,000

To balance C/D 78,000 By adjusted P&L ac

(?)

(NP)

21,000 **

98,000 98,000

19.

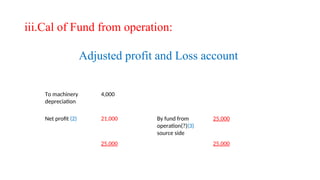

iii.Cal of Fundfrom operation:

Adjusted profit and Loss account

To machinery

depreciation

4,000

Net profit (2) 21,000 By fund from

operation(?)(3)

source side

25,000

25,000 25,000

20.

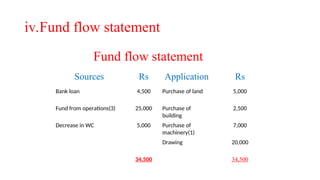

iv.Fund flow statement

Fundflow statement

Sources Rs Application Rs

Bank loan 4,500 Purchase of land 5,000

Fund from operations(3) 25,000 Purchase of

building

2,500

Decrease in WC 5,000 Purchase of

machinery(1)

7,000

Drawing 20,000

34,500 34,500

21.

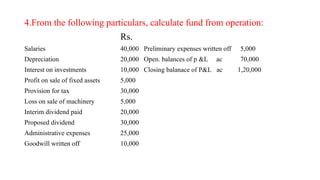

4.From the followingparticulars, calculate fund from operation:

Rs.

Salaries 40,000 Preliminary expenses written off 5,000

Depreciation 20,000 Open. balances of p &L ac 70,000

Interest on investments 10,000 Closing balanace of P&L ac 1,20,000

Profit on sale of fixed assets 5,000

Provision for tax 30,000

Loss on sale of machinery 5,000

Interim dividend paid 20,000

Proposed dividend 30,000

Administrative expenses 25,000

Goodwill written off 10,000

22.

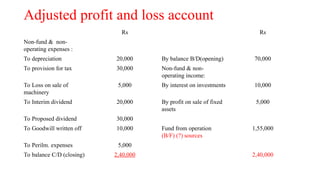

Adjusted profit andloss account

Rs Rs

Non-fund & non-

operating expenses :

To depreciation 20,000 By balance B/D(opening) 70,000

To provision for tax 30,000 Non-fund & non-

operating income:

To Loss on sale of

machinery

5,000 By interest on investments 10,000

To Interim dividend 20,000 By profit on sale of fixed

assets

5,000

To Proposed dividend 30,000

To Goodwill written off 10,000 Fund from operation

(B/F) (?) sources

1,55,000

To Perilm. expenses 5,000

To balance C/D (closing) 2,40,000 2,40,000

23.

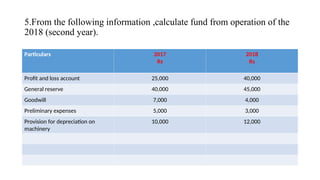

5.From the followinginformation ,calculate fund from operation of the

2018 (second year).

Particulars 2017

Rs

2018

Rs

Profit and loss account 25,000 40,000

General reserve 40,000 45,000

Goodwill 7,000 4,000

Preliminary expenses 5,000 3,000

Provision for depreciation on

machinery

10,000 12,000

24.

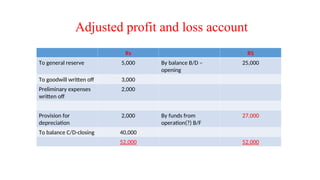

Adjusted profit andloss account

Rs RS

To general reserve 5,000 By balance B/D –

opening

25,000

To goodwill written off 3,000

Preliminary expenses

written off

2,000

Provision for

depreciation

2,000 By funds from

operation(?) B/F

27,000

To balance C/D-closing 40,000

52,000 52,000

25.

***

Note:

•Non-fund and non-operatingitems are taken into account in the

preparation of adjusted profit and loss account.

•Changes during the second year are ascertained by comparison with

first year. For instance, transfer to general reserve, during the second

year is (45,000-40,0000) Rs.5,000

26.

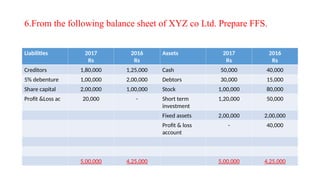

6.From the followingbalance sheet of XYZ co Ltd. Prepare FFS.

Liabilities 2017

Rs

2016

Rs

Assets 2017

Rs

2016

Rs

Creditors 1,80,000 1,25,000 Cash 50,000 40,000

5% debenture 1,00,000 2,00,000 Debtors 30,000 15,000

Share capital 2,00,000 1,00,000 Stock 1,00,000 80,000

Profit &Loss ac 20,000 - Short term

investment

1,20,000 50,000

Fixed assets 2,00,000 2,00,000

Profit & loss

account

- 40,000

5,00,000 4,25,000 5,00,000 4,25,000

27.

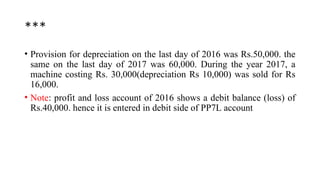

***

• Provision fordepreciation on the last day of 2016 was Rs.50,000. the

same on the last day of 2017 was 60,000. During the year 2017, a

machine costing Rs. 30,000(depreciation Rs 10,000) was sold for Rs

16,000.

• Note: profit and loss account of 2016 shows a debit balance (loss) of

Rs.40,000. hence it is entered in debit side of PP7L account

28.

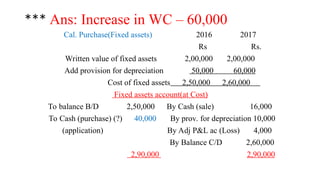

*** Ans: Increasein WC – 60,000

Cal. Purchase(Fixed assets) 2016 2017

Rs Rs.

Written value of fixed assets 2,00,000 2,00,000

Add provision for depreciation 50,000 60,000

Cost of fixed assets 2,50,000 2,60,000

Fixed assets account(at Cost)

To balance B/D 2,50,000 By Cash (sale) 16,000

To Cash (purchase) (?) 40,000 By prov. for depreciation 10,000

(application) By Adj P&L ac (Loss) 4,000

By Balance C/D 2,60,000

2,90,000 2,90,000

29.

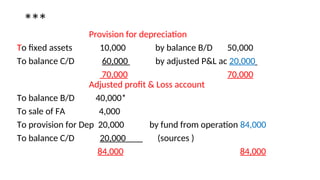

***

Provision for depreciation

Tofixed assets 10,000 by balance B/D 50,000

To balance C/D 60,000 by adjusted P&L ac 20,000

70,000 70,000

Adjusted profit & Loss account

To balance B/D 40,000*

To sale of FA 4,000

To provision for Dep 20,000 by fund from operation 84,000

To balance C/D 20,000 (sources )

84,000 84,000

30.

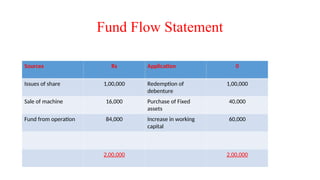

Fund Flow Statement

SourcesRs Application 0

Issues of share 1,00,000 Redemption of

debenture

1,00,000

Sale of machine 16,000 Purchase of Fixed

assets

40,000

Fund from operation 84,000 Increase in working

capital

60,000

2,00,000 2,00,000

31.

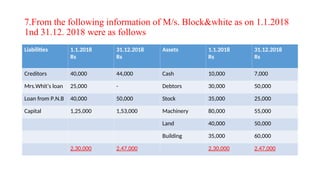

7.From the followinginformation of M/s. Block&white as on 1.1.2018

1nd 31.12. 2018 were as follows

Liabilities 1.1.2018

Rs

31.12.2018

Rs

Assets 1.1.2018

Rs

31.12.2018

Rs

Creditors 40,000 44,000 Cash 10,000 7,000

Mrs.Whit’s loan 25,000 - Debtors 30,000 50,000

Loan from P.N.B 40,000 50,000 Stock 35,000 25,000

Capital 1,25,000 1,53,000 Machinery 80,000 55,000

Land 40,000 50,000

Building 35,000 60,000

2,30,000 2,47,000 2,30,000 2,47,000

32.

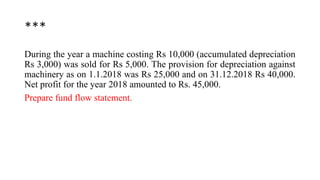

***

During the yeara machine costing Rs 10,000 (accumulated depreciation

Rs 3,000) was sold for Rs 5,000. The provision for depreciation against

machinery as on 1.1.2018 was Rs 25,000 and on 31.12.2018 Rs 40,000.

Net profit for the year 2018 amounted to Rs. 45,000.

Prepare fund flow statement.

33.

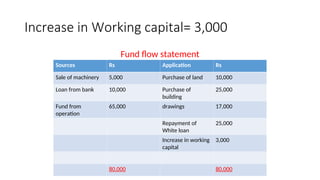

Increase in Workingcapital= 3,000

Fund flow statement

Sources Rs Application Rs

Sale of machinery 5,000 Purchase of land 10,000

Loan from bank 10,000 Purchase of

building

25,000

Fund from

operation

65,000 drawings 17,000

Repayment of

White loan

25,000

Increase in working

capital

3,000

80,000 80,000

34.

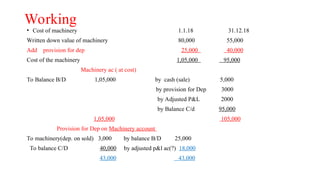

Working

• Cost ofmachinery 1.1.18 31.12.18

Written down value of machinery 80,000 55,000

Add provision for dep 25,000 40,000

Cost of the machinery 1,05,000 95,000

Machinery ac ( at cost)

To Balance B/D 1,05,000 by cash (sale) 5,000

by provision for Dep 3000

by Adjusted P&L 2000

by Balance C/d 95,000

1,05,000 105,000

Provision for Dep on Machinery account

To machinery(dep. on sold) 3,000 by balance B/D 25,000

To balance C/D 40,000 by adjusted p&l ac(?) 18,000

43,000 43,000

35.

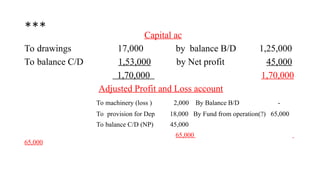

*** Capital ac

Todrawings 17,000 by balance B/D 1,25,000

To balance C/D 1,53,000 by Net profit 45,000

1,70,000 1,70,000

Adjusted Profit and Loss account

To machinery (loss ) 2,000 By Balance B/D -

To provision for Dep 18,000 By Fund from operation(?) 65,000

To balance C/D (NP) 45,000

65,000

65,000

36.

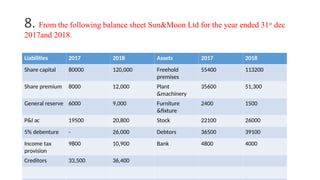

8. From thefollowing balance sheet Sun&Moon Ltd for the year ended 31st

dec

2017and 2018.

Liabilities 2017 2018 Assets 2017 2018

Share capital 80000 120,000 Freehold

premises

55400 113200

Share premium 8000 12,000 Plant

&machinery

35600 51,300

General reserve 6000 9,000 Furniture

&fixture

2400 1500

P&l ac 19500 20,800 Stock 22100 26000

5% debenture - 26,000 Debtors 36500 39100

Income tax

provision

9800 10,900 Bank 4800 4000

Creditors 33,500 36,400

37.

Additional information

• Depreciationwritten off during the year 2018 was as under:

a.Plant & machinery Rs 12,800

b.Furniture &fixture Rs.400

c.Prepare a statement of sources and uses of funds.

Ans: increase in WC= 1700

Fund from operation= 17500

FFS= 88000