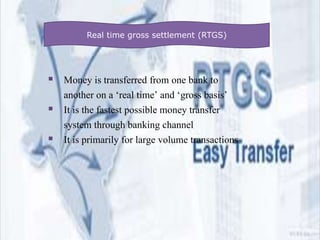

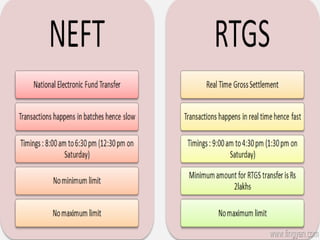

The document discusses the evolution of e-banking and various technologies used in the banking sector. It describes traditional banking services and the emergence of electronic delivery channels like ATMs, debit/credit cards, internet banking, mobile banking, RTGS and NEFT systems. While e-banking provides benefits like convenience, speed and lower costs, security issues remain a challenge. Both banks and customers must take steps to reduce security threats in order to increase popularity of e-banking.

![E banking by sanjeev kumar chaswal [compatibility mode]](https://cdn.slidesharecdn.com/ss_thumbnails/e-bankingbysanjeevkumarchaswalcompatibilitymode-130122093515-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)