Downloaded 83 times

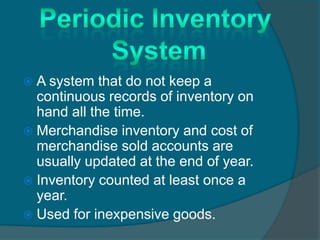

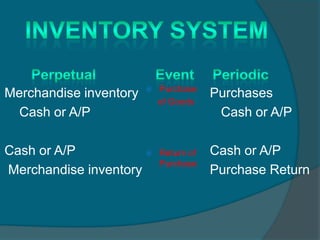

The document discusses key concepts related to inventory accounting including: 1) It defines merchandise inventory as goods owned by a business that are held for sale to customers. 2) It explains the difference between perpetual and periodic inventory systems, with perpetual updating inventory records continuously and periodic conducting a physical count annually. 3) It outlines different inventory costing methods including FIFO, LIFO, and average cost.