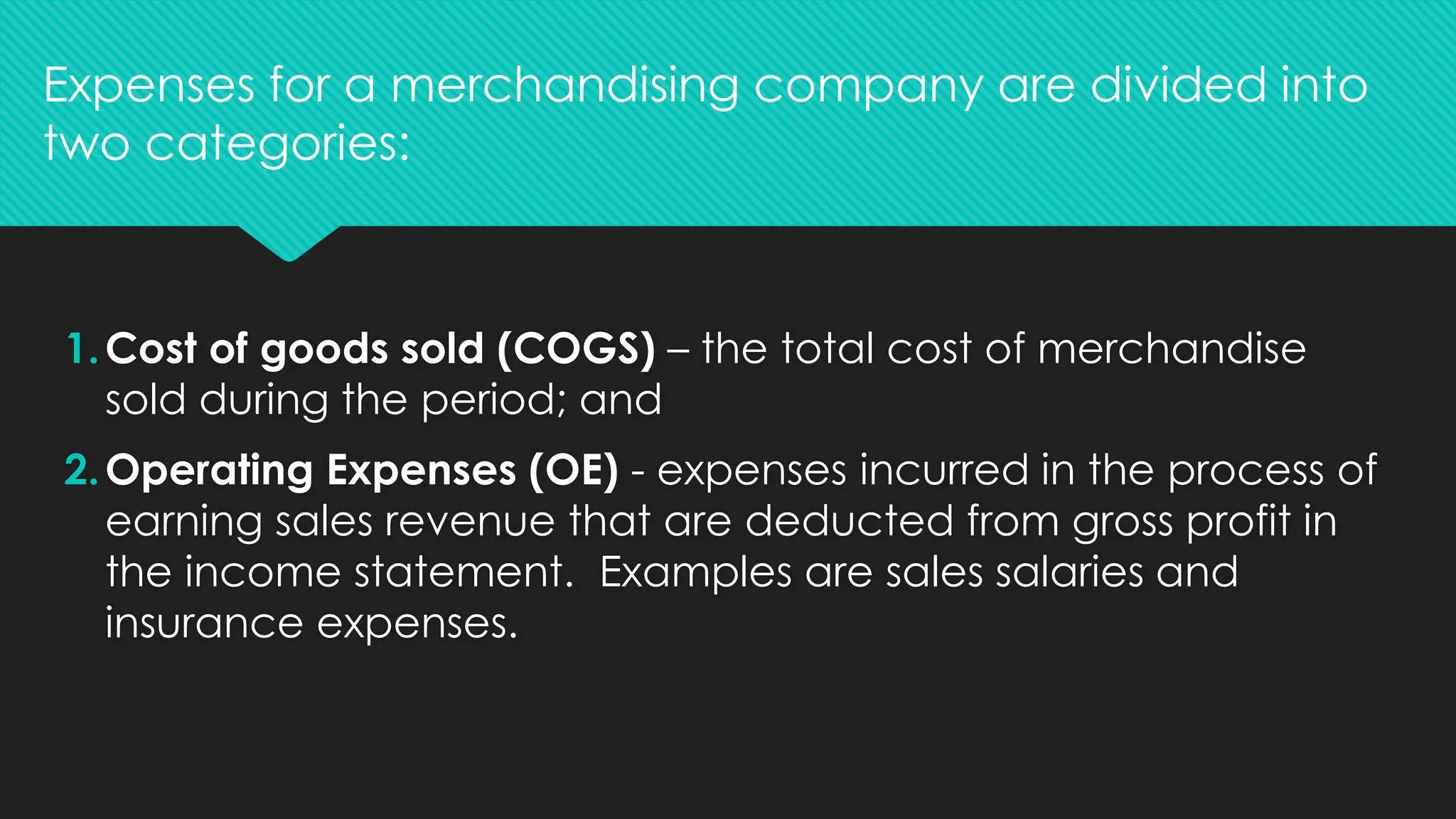

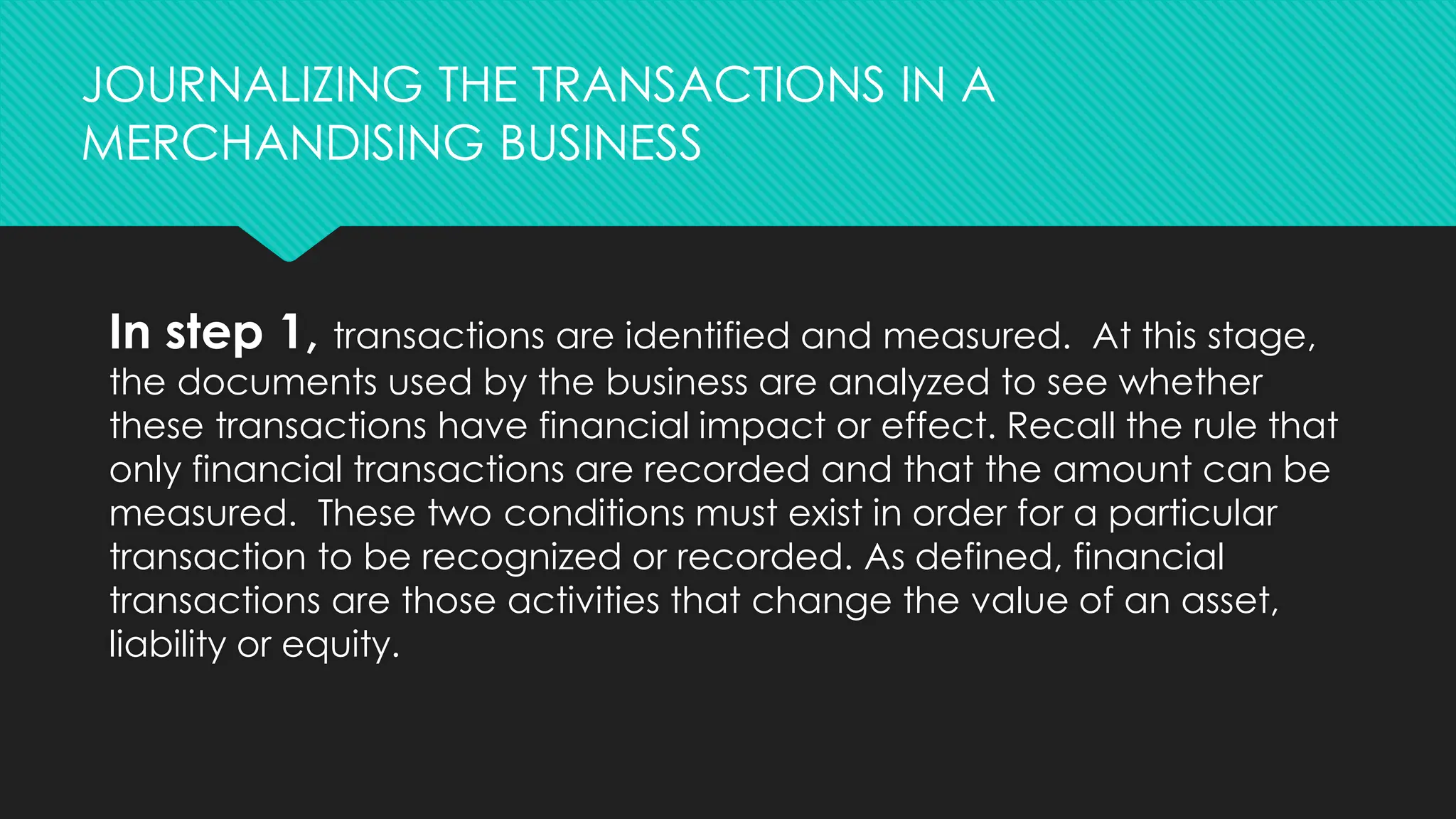

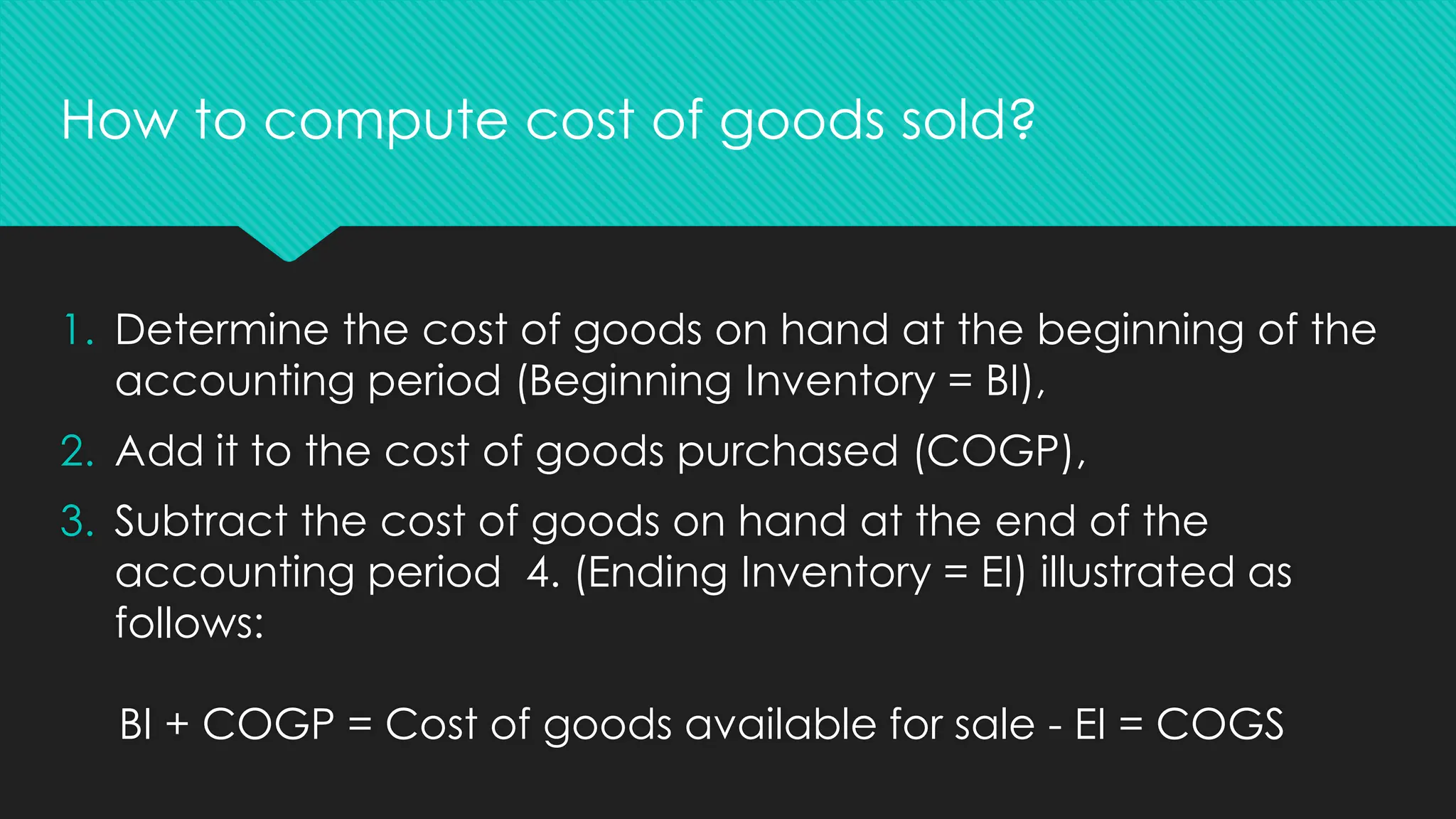

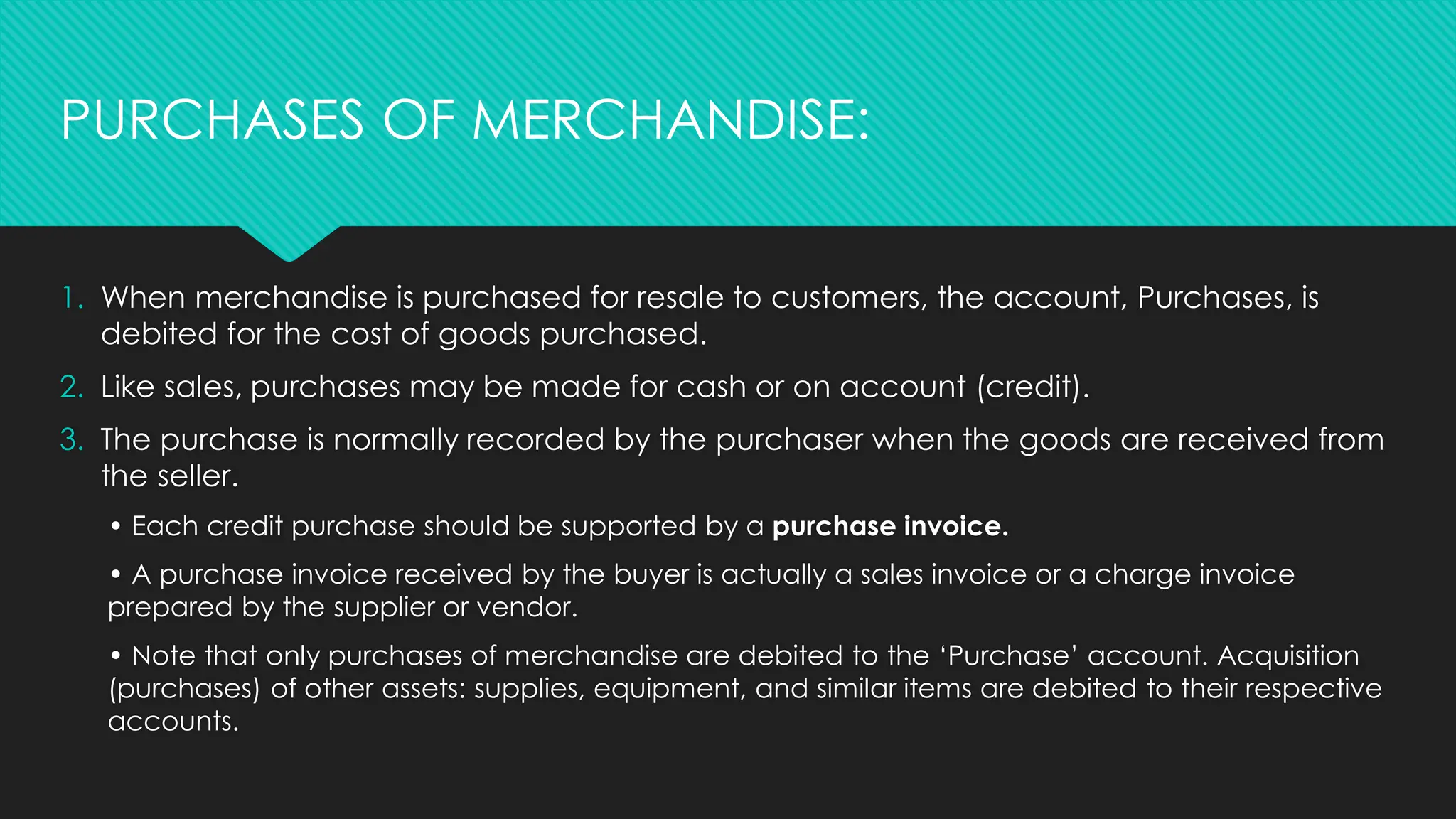

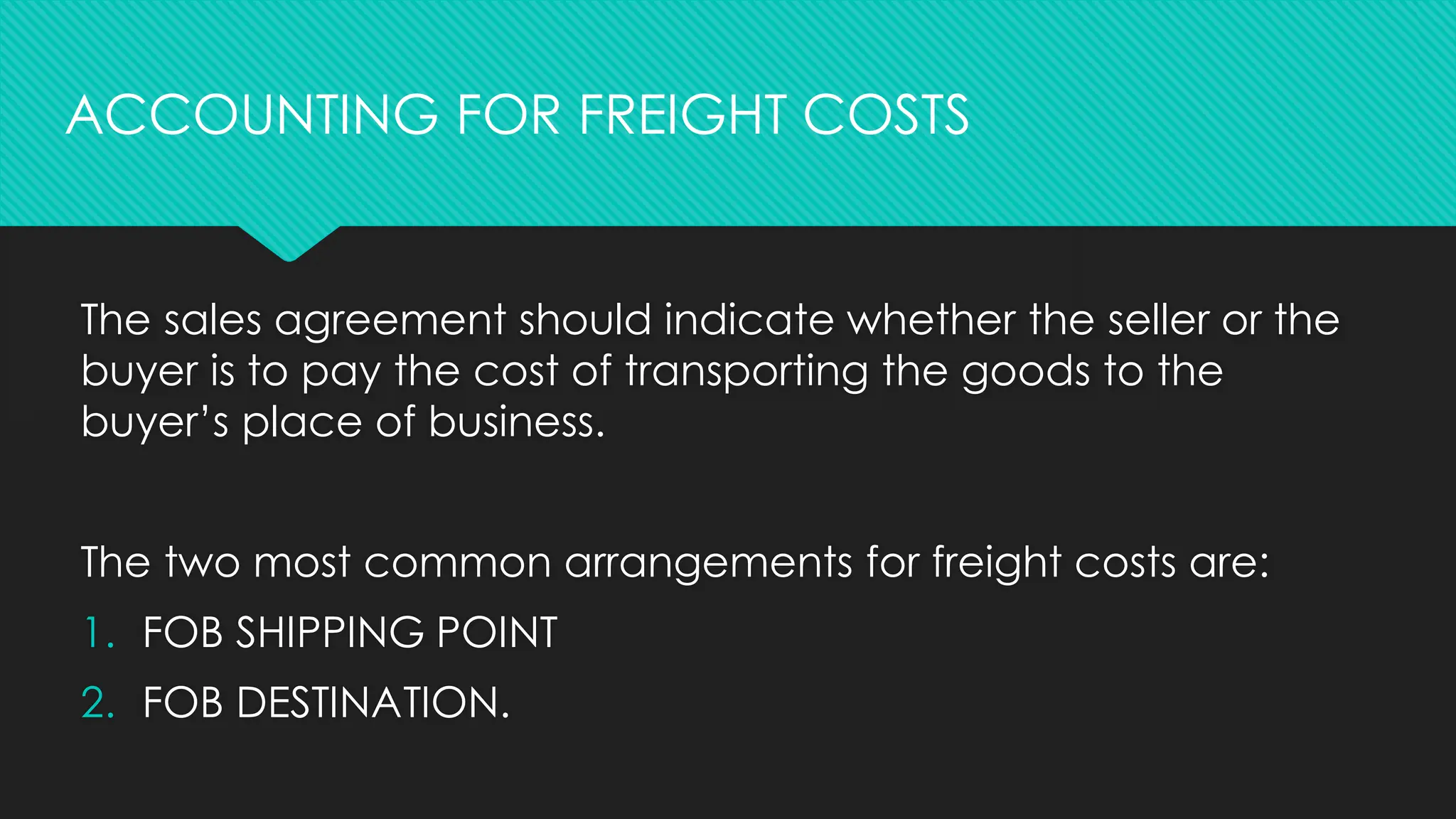

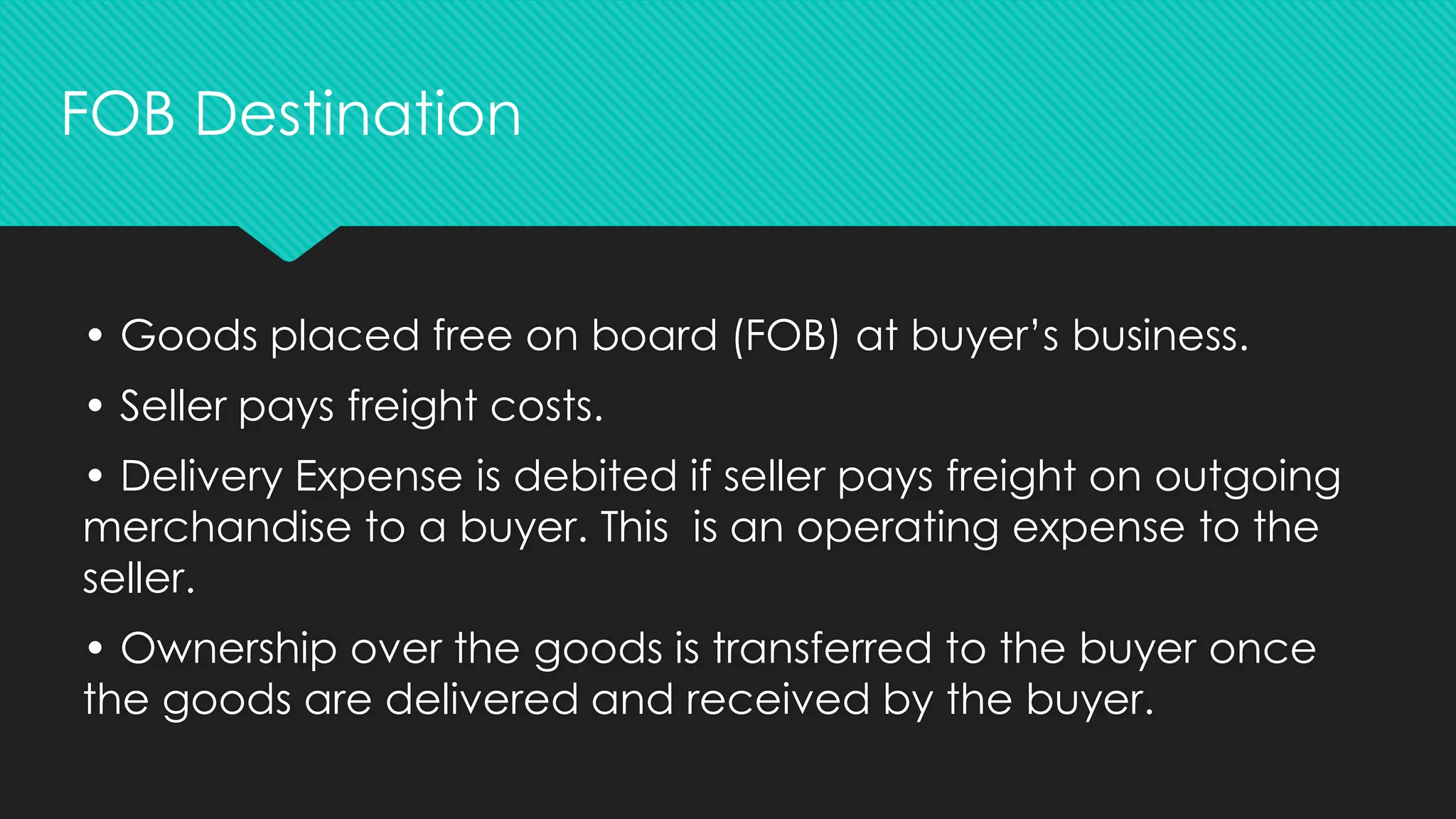

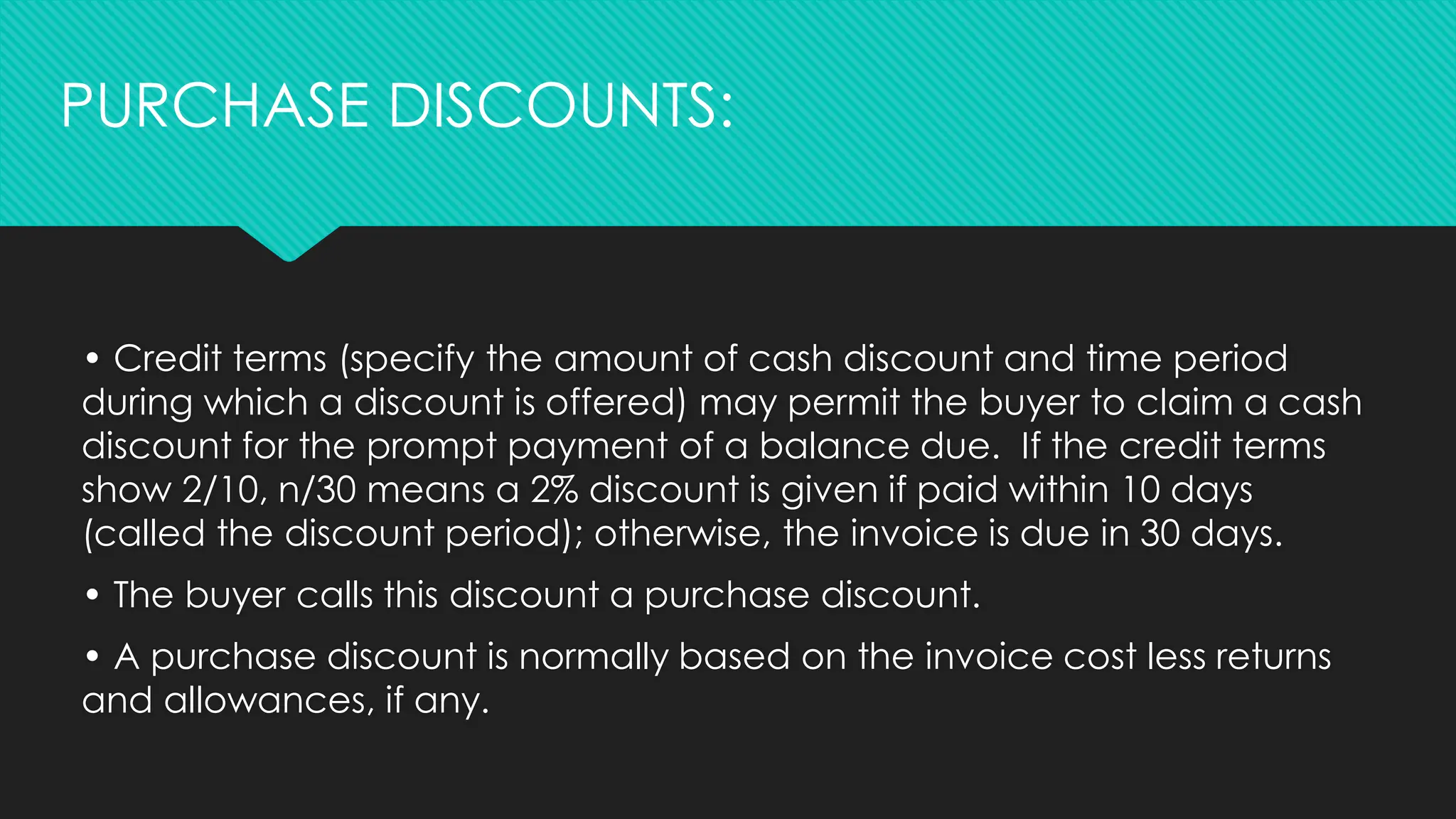

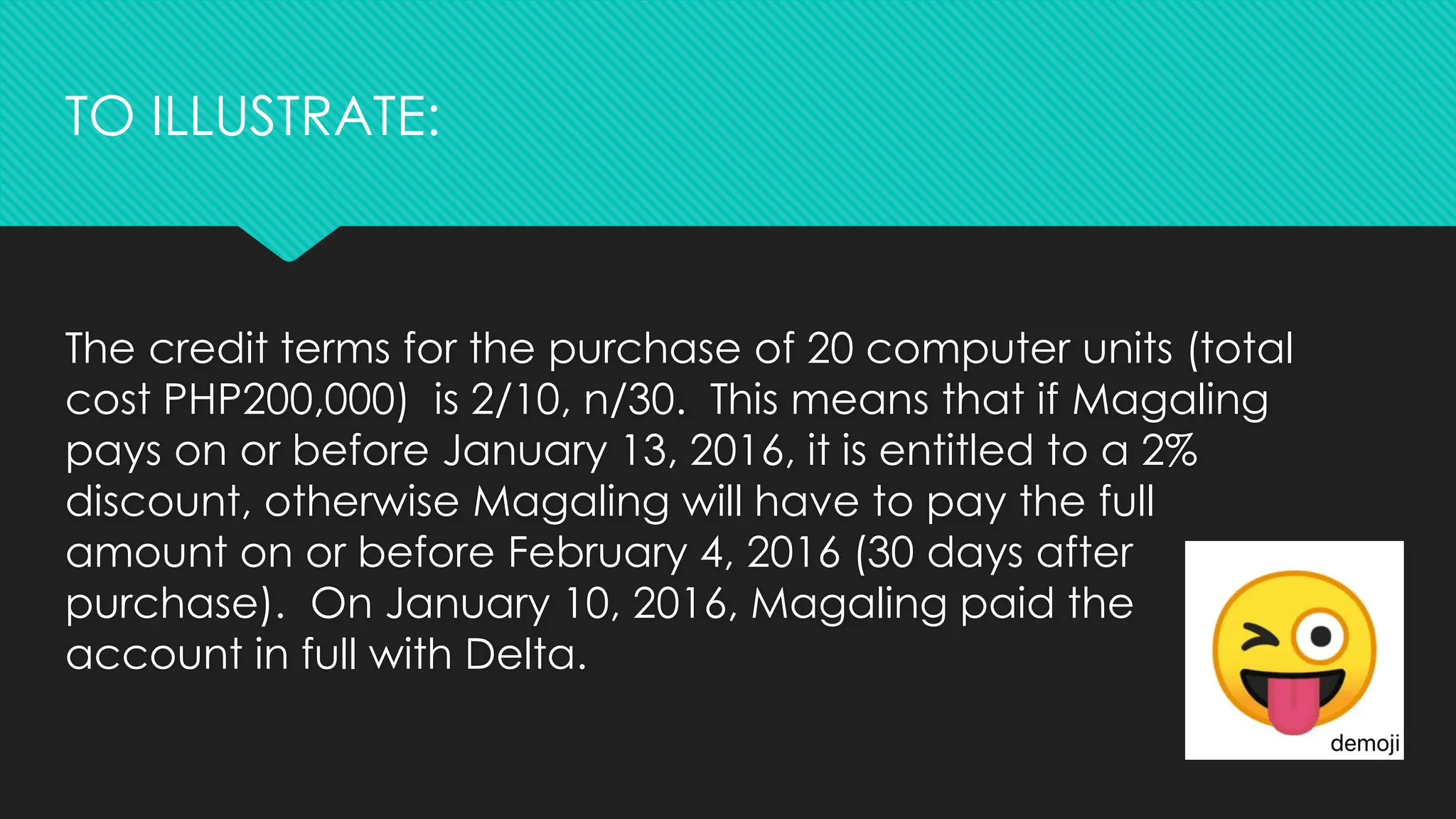

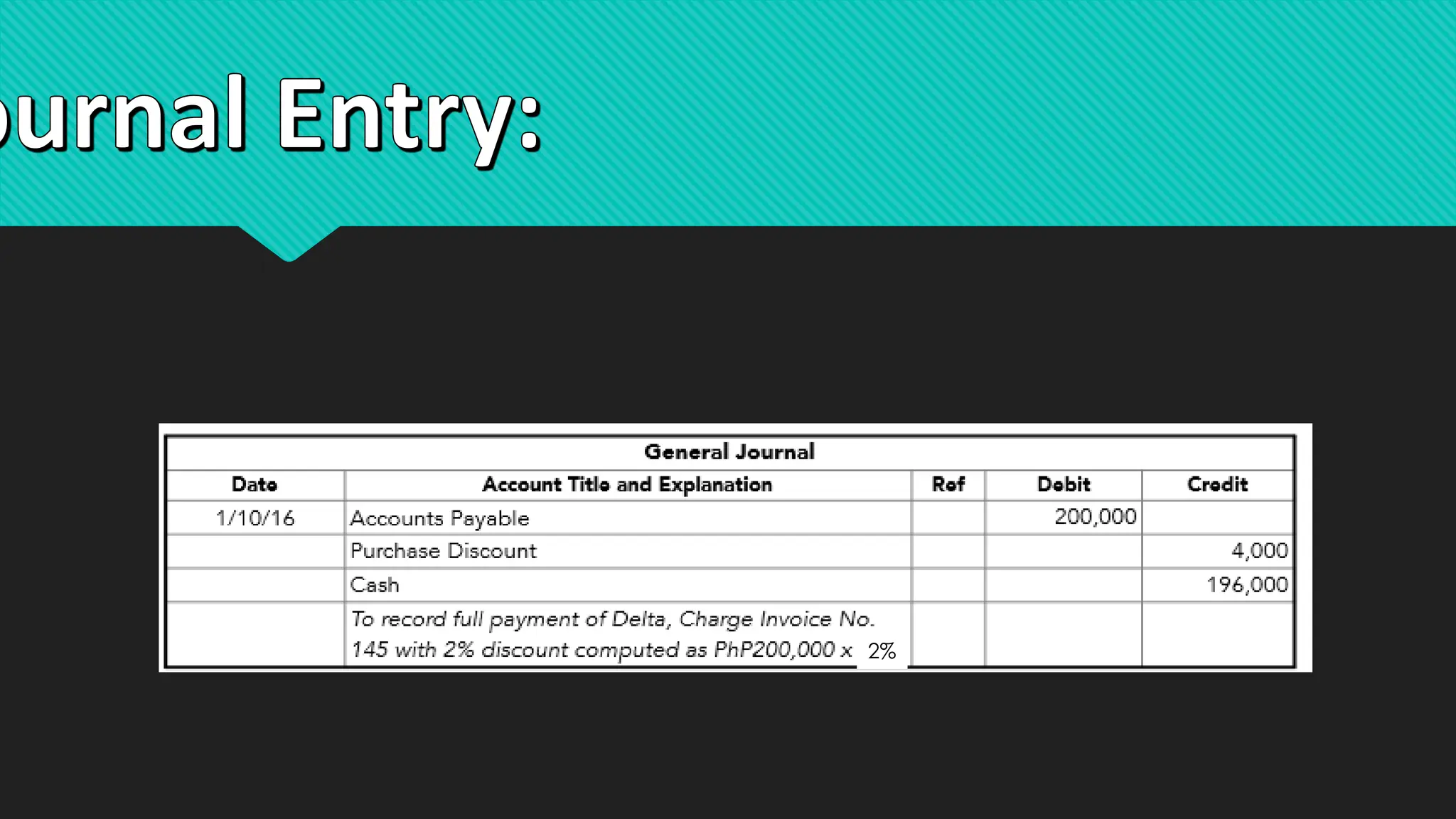

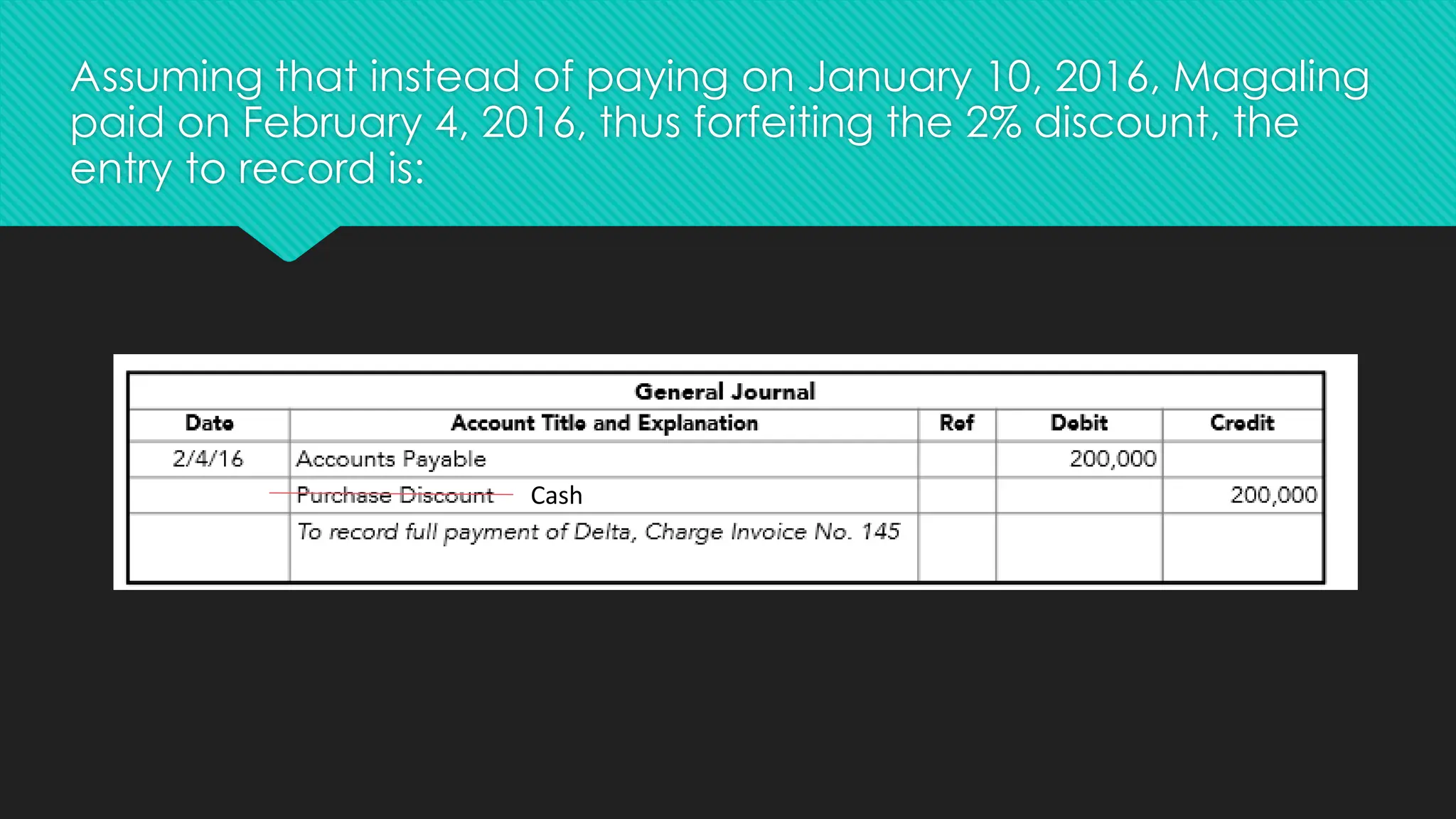

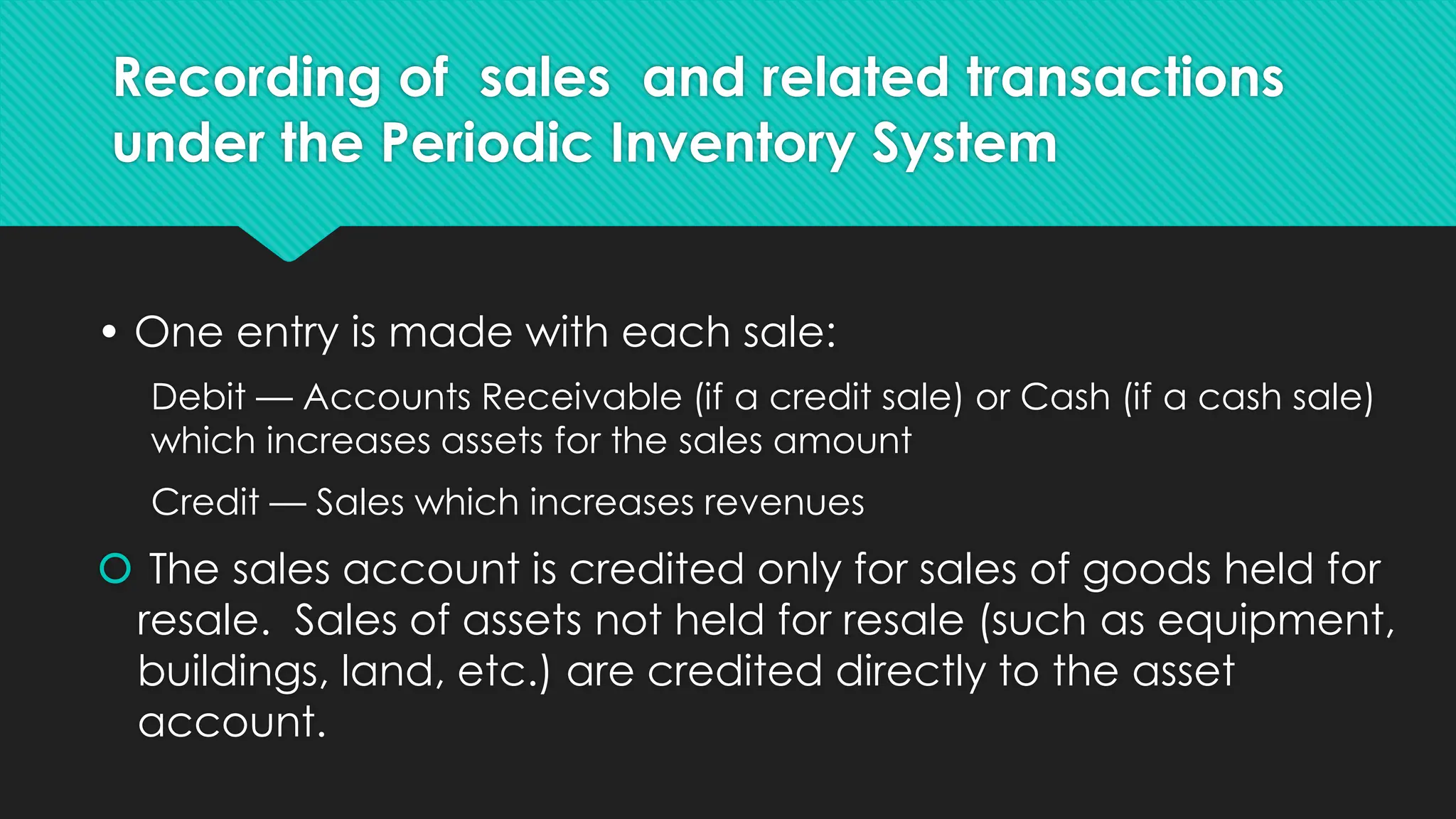

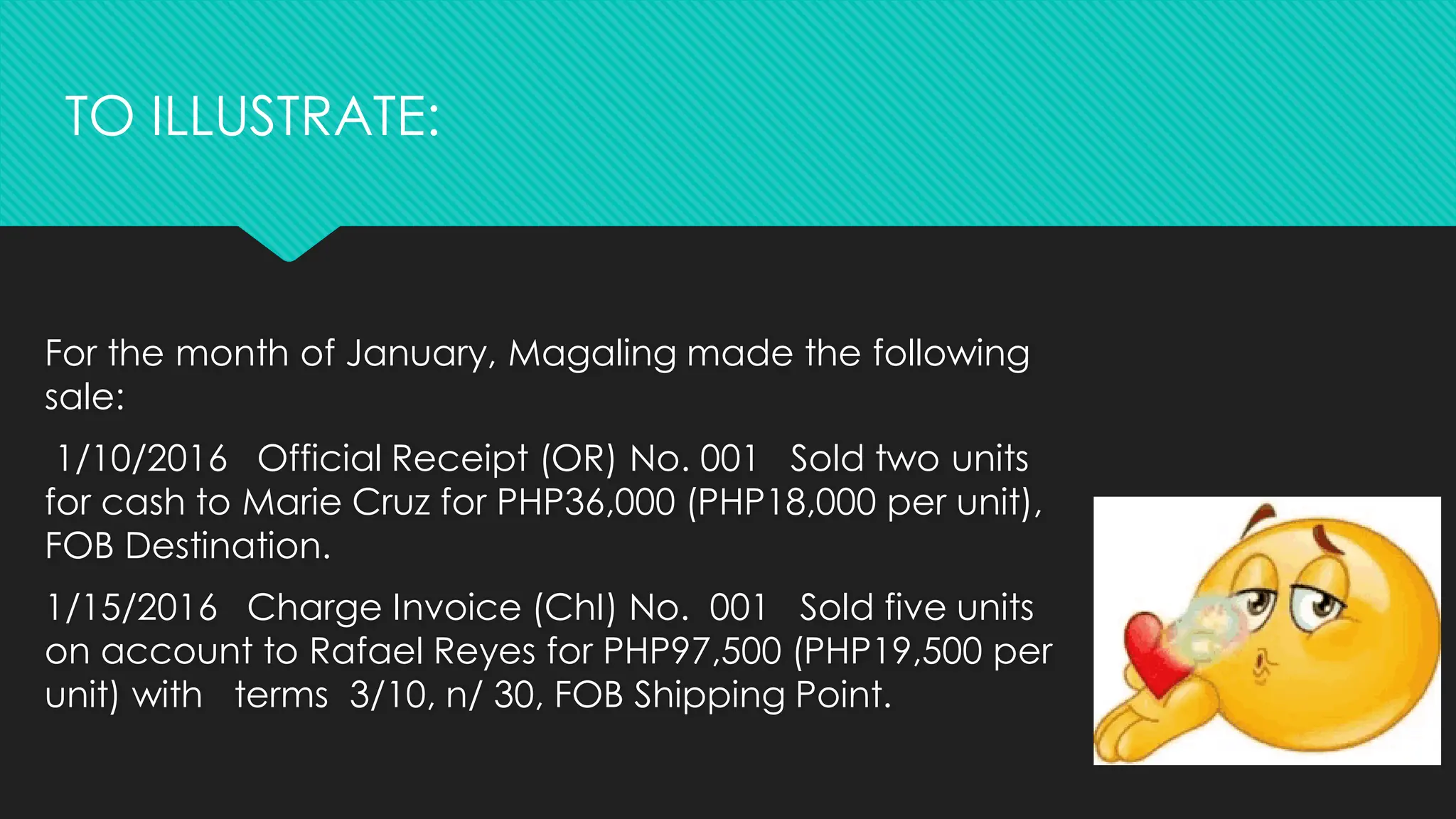

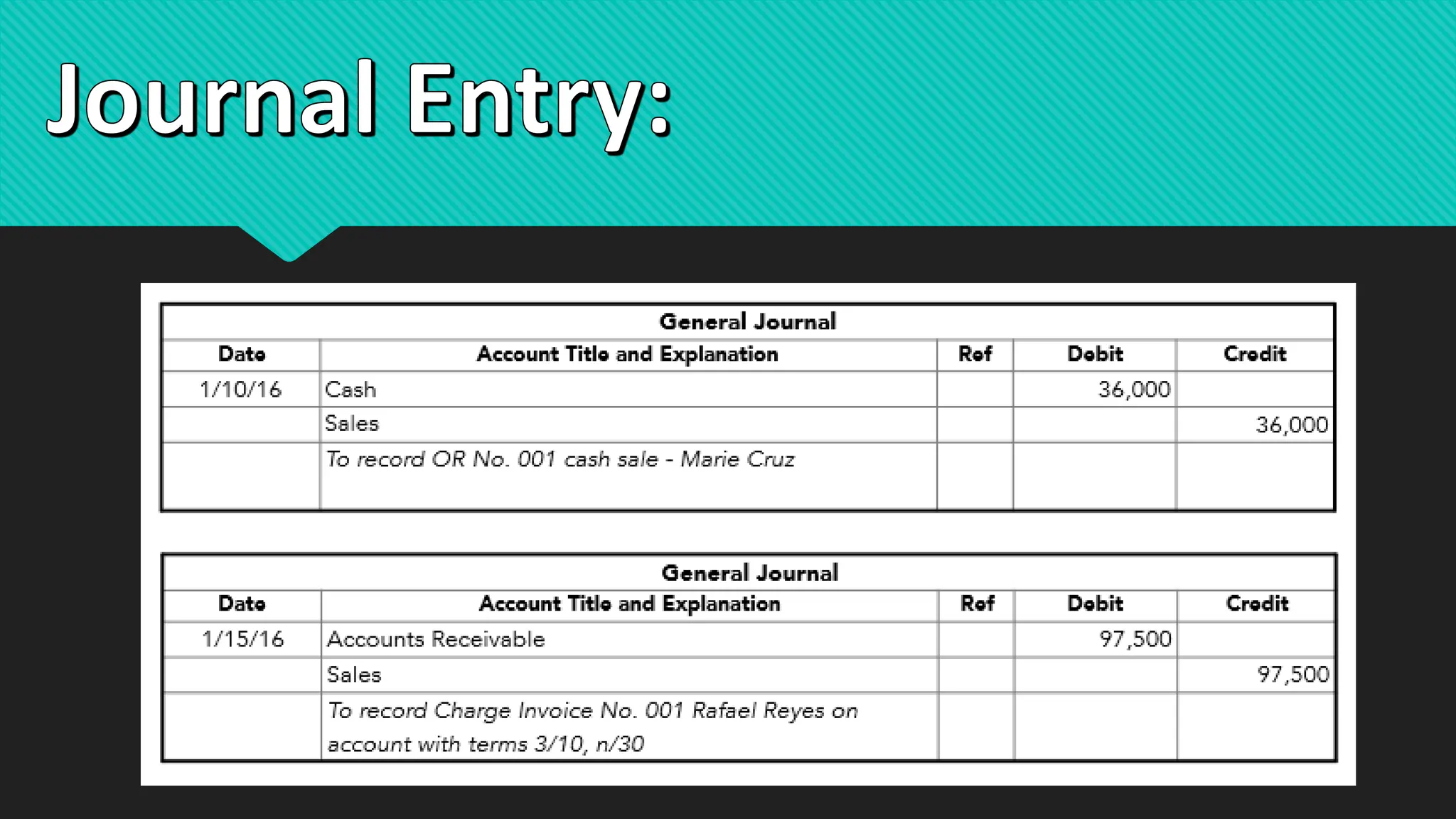

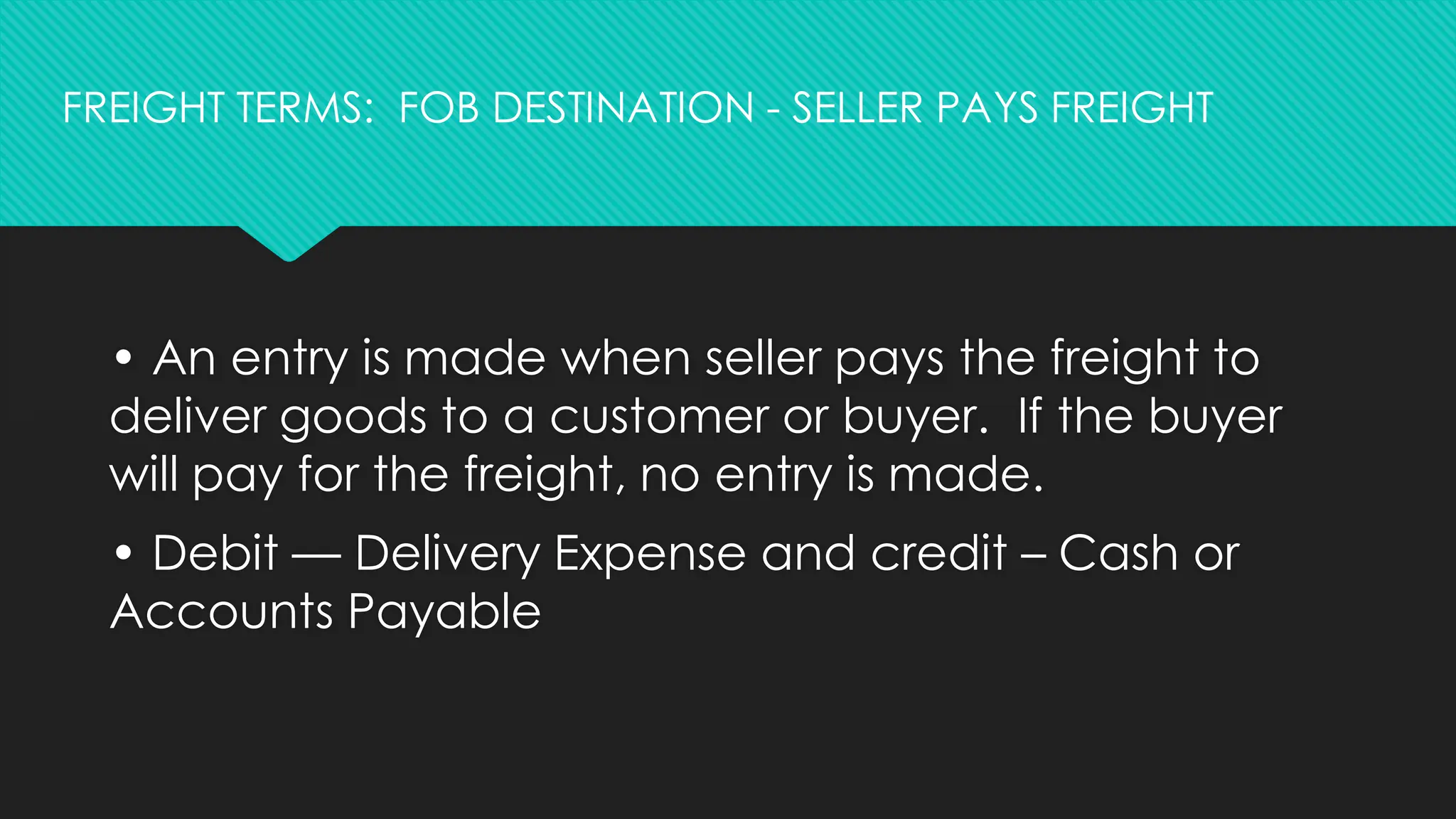

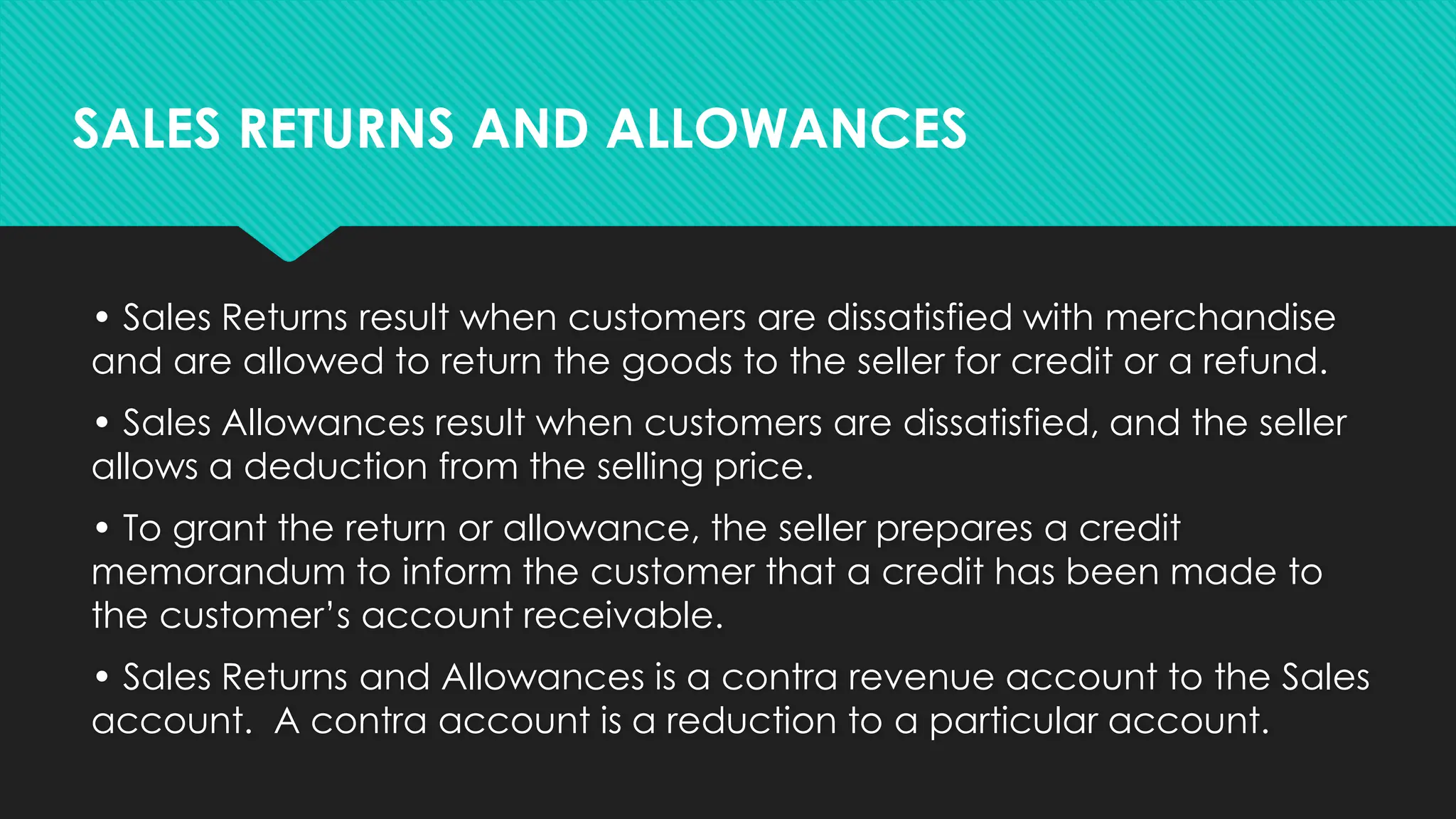

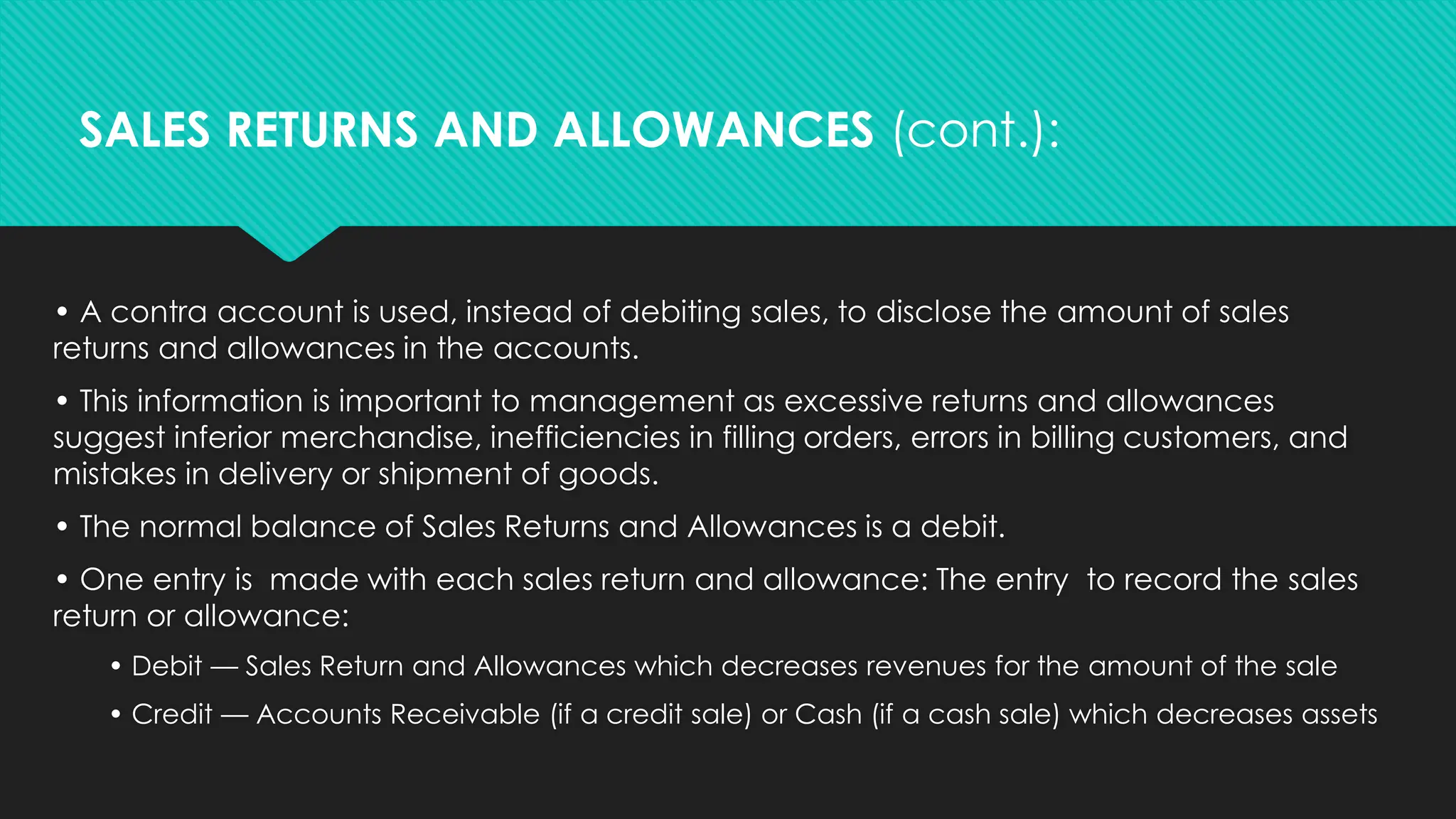

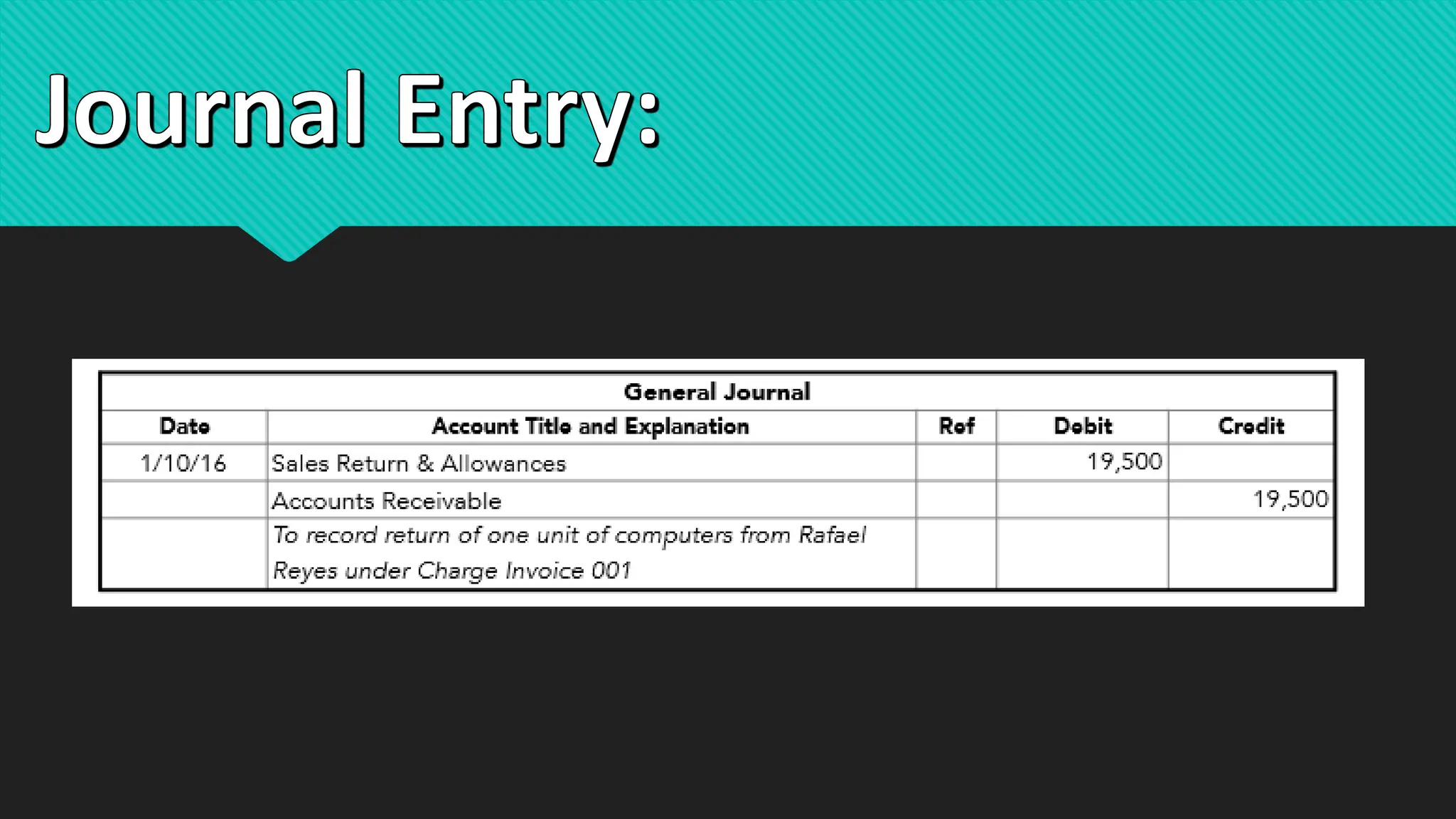

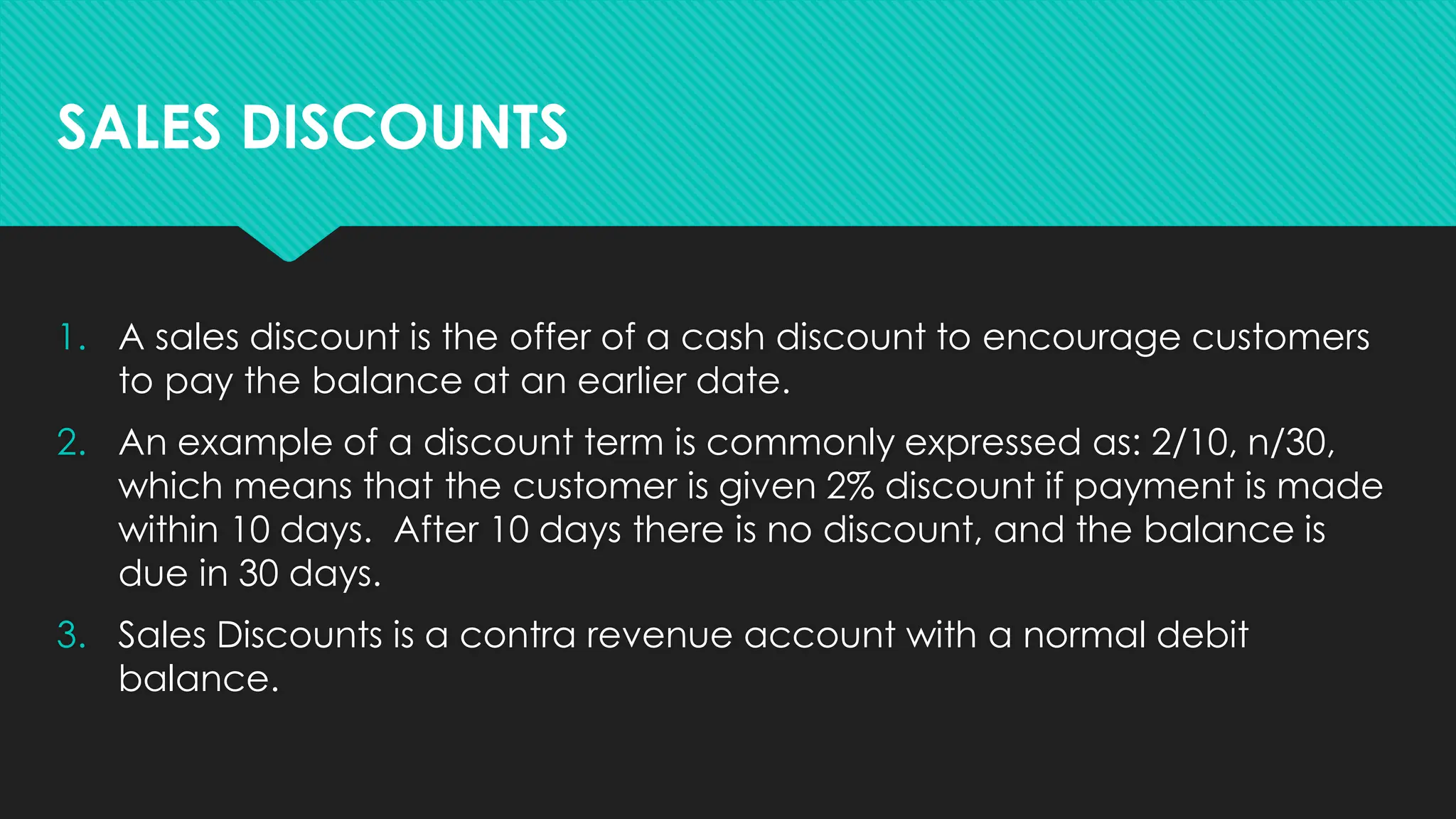

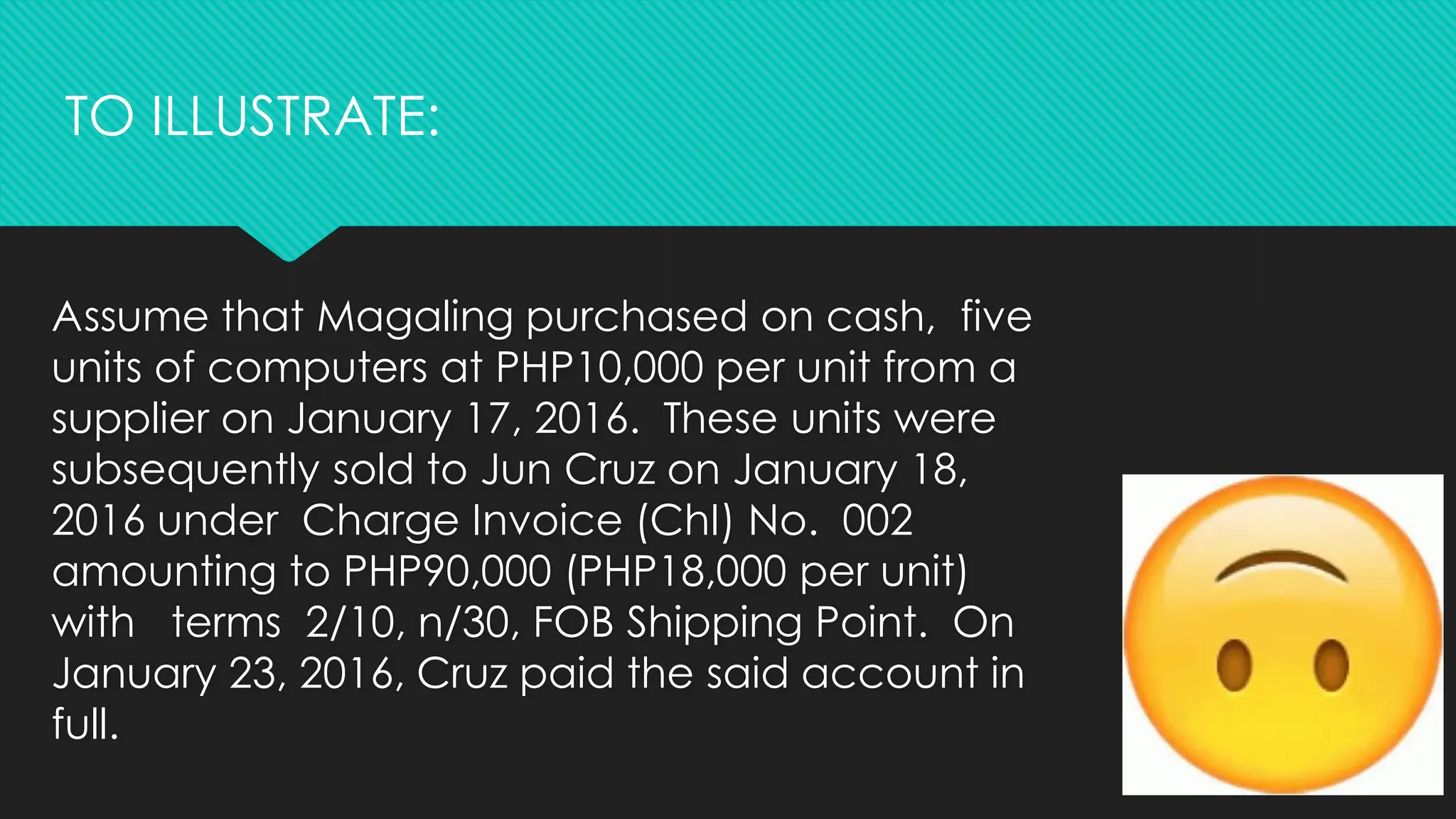

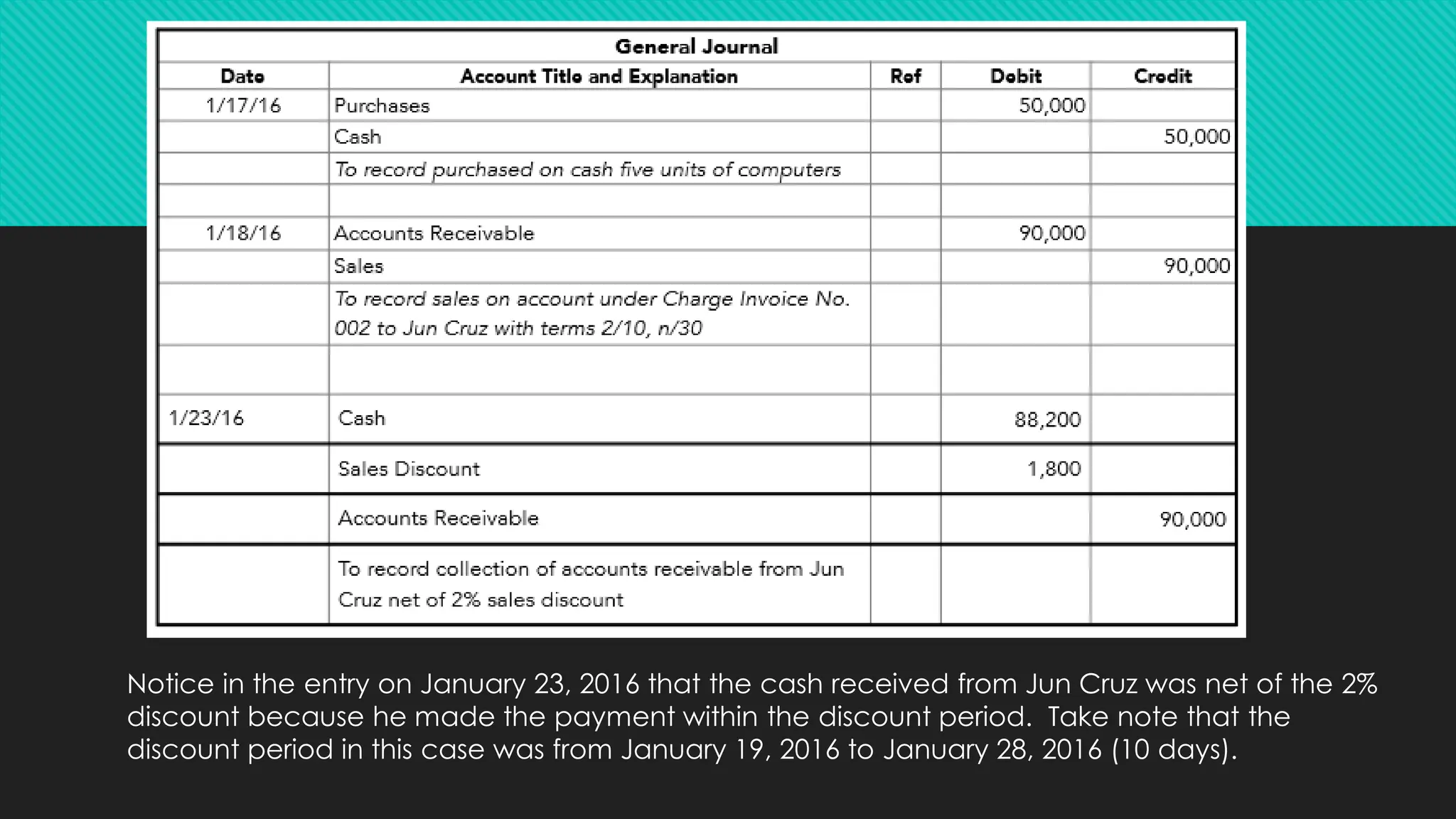

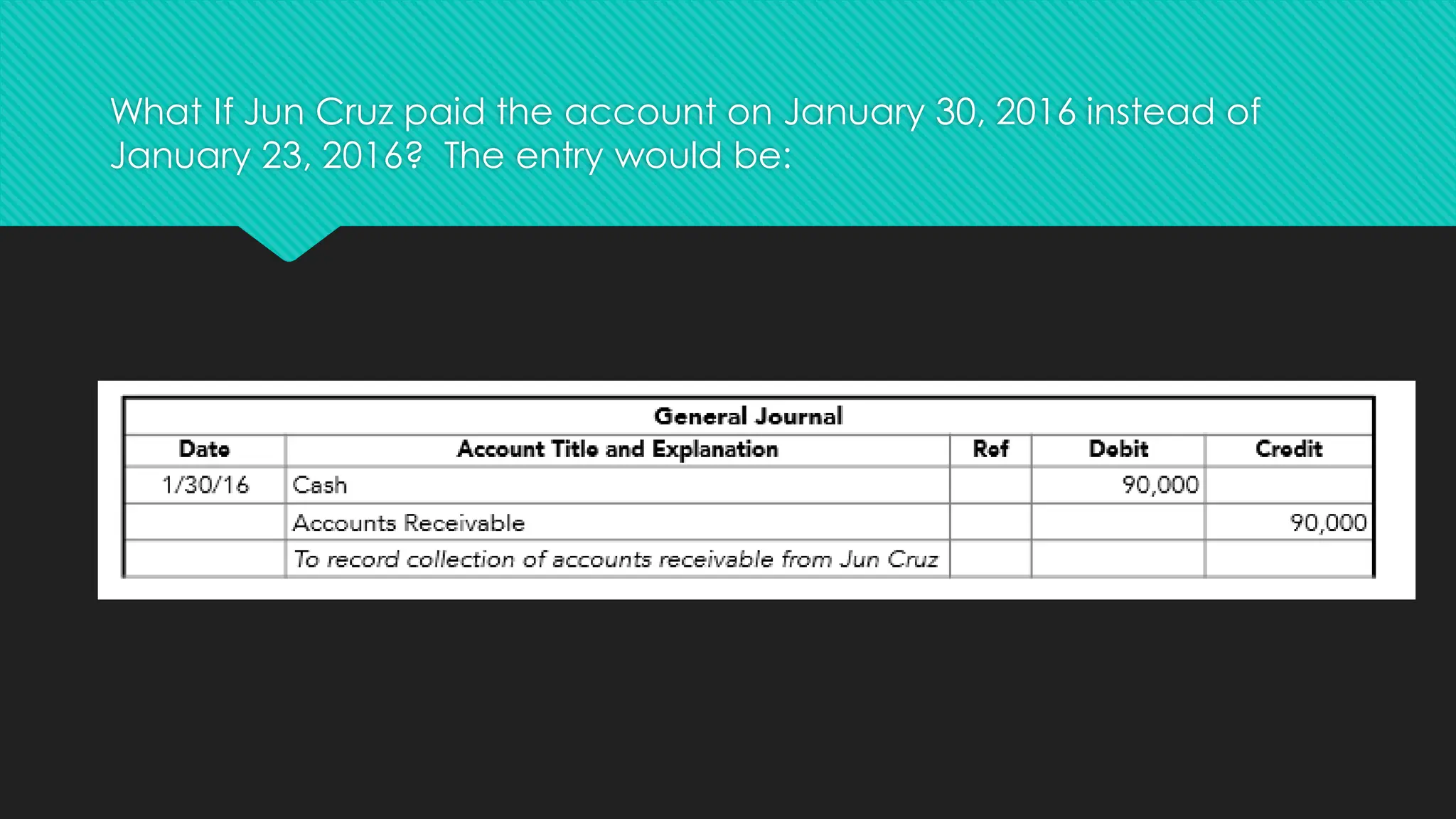

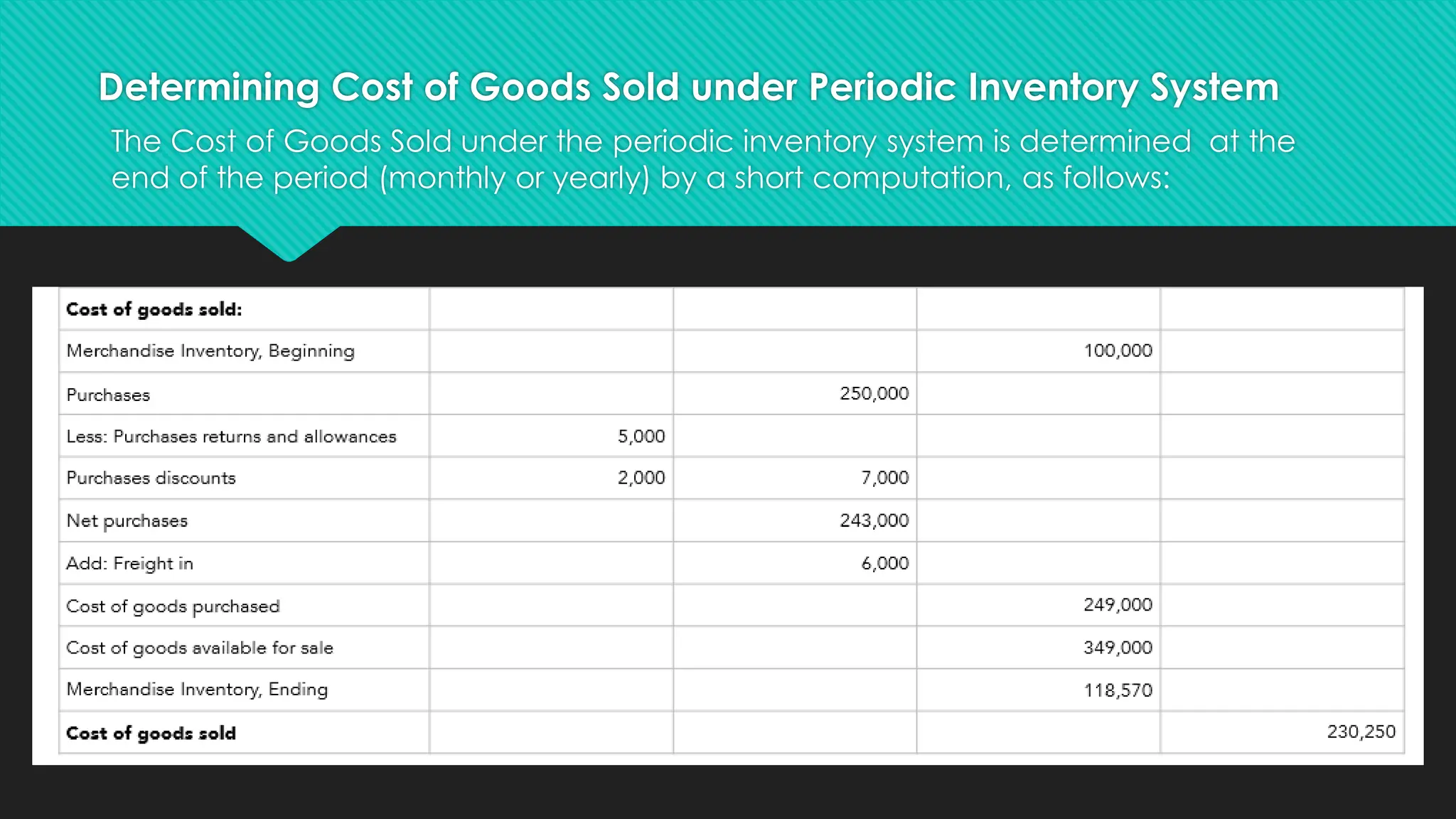

The document discusses the operations of merchandising businesses, focusing on sales revenue, cost of goods sold (COGS), and various inventory accounting methods. It explains the operating cycle, journalizing transactions, and the need for special journals due to high transaction volumes. Additionally, it outlines freight costs, sales returns and allowances, and the periodic inventory system for determining COGS at the end of an accounting period.