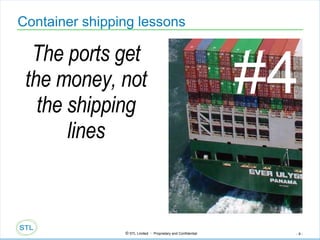

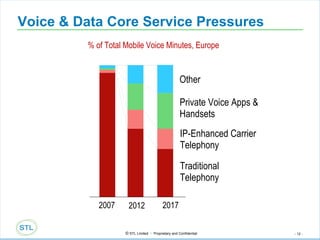

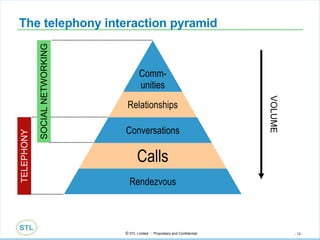

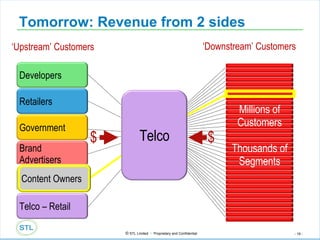

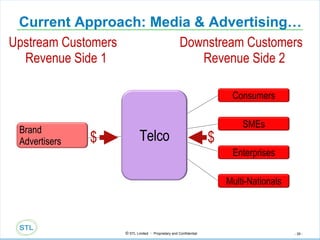

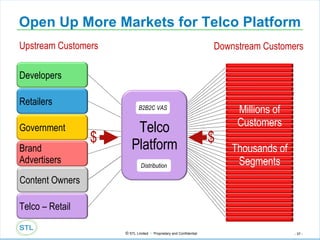

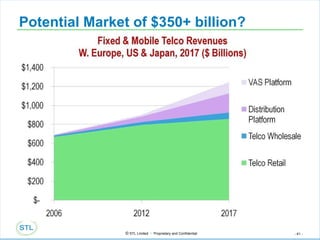

The document discusses how telecom companies can adopt a two-sided business model like other industries such as container shipping and online platforms. It argues that telecom companies have valuable customer data and assets that could be leveraged to provide logistics and value-added services to both upstream business customers and downstream end users, opening up new revenue opportunities beyond traditional voice and data services. By creating open platforms and focusing on scale, packaging solutions, rewards, privacy, and reliability, telecom companies could tap into a potential $350 billion market for these two-sided services.

![The Two-sided Telecoms Business Model Re-thinking the phone company 14 March 2008 Martin Geddes, Chief Analyst, STL Partners [email_address]](https://image.slidesharecdn.com/martingeddesecomm2008-1207763517808813-9/85/Martin-Geddes-s-presentation-at-eComm-2008-1-320.jpg)

![The Two-sided Telecoms Business Model Re-thinking the phone company 14 March 2008 Martin Geddes, Chief Analyst, STL Partners [email_address]](https://image.slidesharecdn.com/martingeddesecomm2008-1207763517808813-9/75/Martin-Geddes-s-presentation-at-eComm-2008-1-2048.jpg)

![Telco 2[1].0 Two Telco2.0,Two Sided Telecoms Bus Models,Simon Torrance,08,18p](https://cdn.slidesharecdn.com/ss_thumbnails/telco21-0-two-telco2-0two-sided-telecomsbus-modelssimontorrance0818p-090519042227-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)