The document provides an introduction to audits and regulatory compliance. It defines auditing as the systematic inspection of a process or system to ensure compliance. The scope of auditing has expanded beyond fraud detection to determine a true and fair view of financial statements based on various legislations. An auditor must be honest, impartial, and have skills like common sense, questioning abilities, and thorough knowledge. Techniques include checking transactions and verifying assets. The objectives of audits are to ensure fairness, compliance with laws, assess accounting policies, and provide an independent opinion. Management is responsible for the audit process and must provide resources and access to auditors.

An overview of auditing importance, purpose, and content outline, emphasizing regulatory compliance.

Definitions and scope of audits, focusing on systematic examinations and legislative regulations in auditing.

Key qualities of effective auditors and common techniques used to perform thorough audits.

Introduction to quality audits, detailing internal and external audit types.

Exploration of primary, secondary, and special objectives of audits, including compliance and fraud detection.

Discussion on audit management strategies, team organization, and roles involved in conducting audits.Detailed responsibilities of audit team leaders and members in conducting audits effectively.

List of references used in the presentation and a brief conclusion thanking the audience.

Introduction of Auditsand Regulatory

Compliance

Presented By :- Guided By:-

Jitendra K. Sonawane Dr.L.R.Zawar

M.Pharm (QA)

H. R. Patel Institute of Pharmaceutical Education and

Research, Shirpur

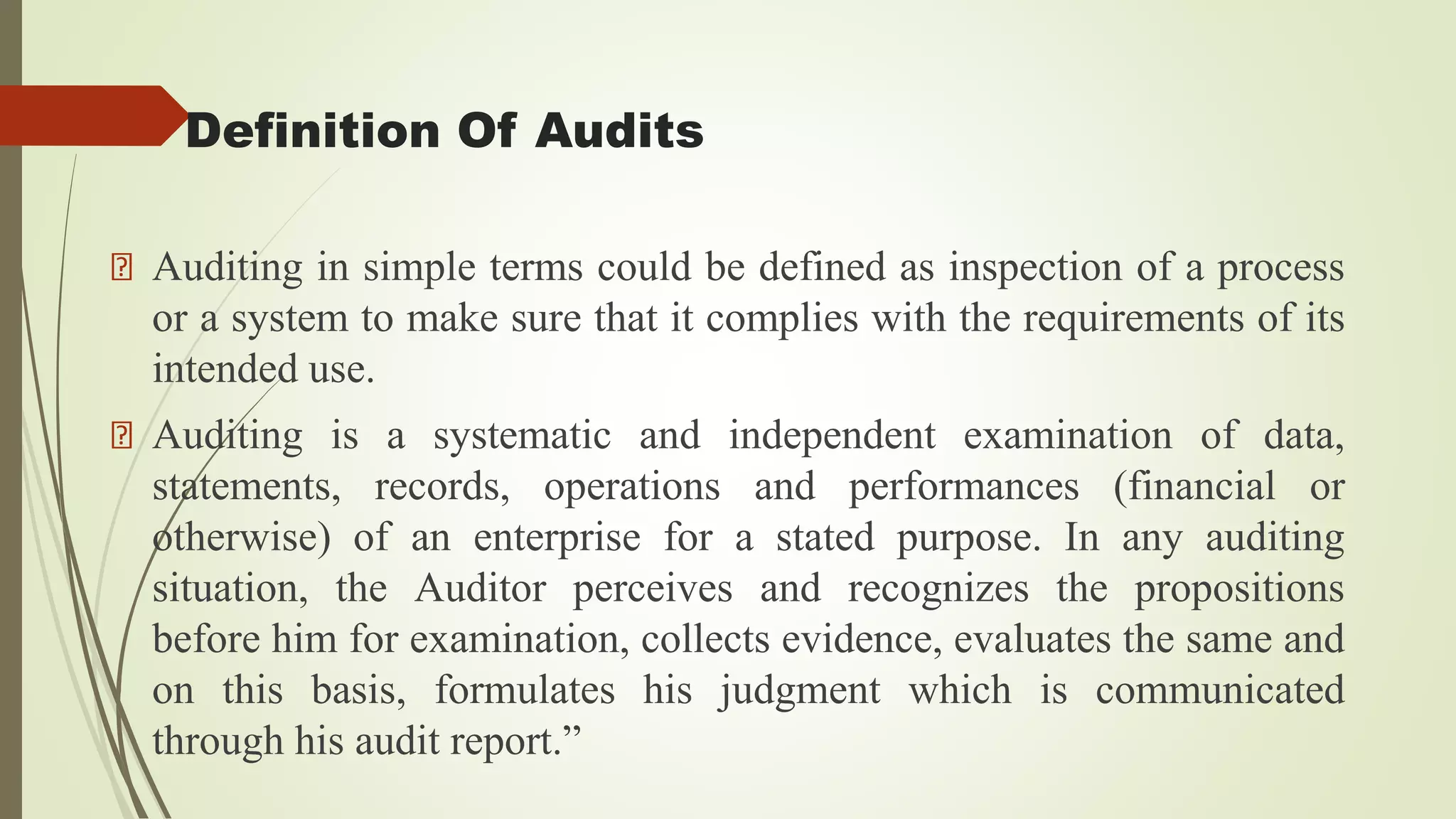

Definition Of Audits

Auditingin simple terms could be defined as inspection of a process

or a system to make sure that it complies with the requirements of its

intended use.

Auditing is a systematic and independent examination of data,

statements, records, operations and performances (financial or

otherwise) of an enterprise for a stated purpose. In any auditing

situation, the Auditor perceives and recognizes the propositions

before him for examination, collects evidence, evaluates the same and

on this basis, formulates his judgment which is communicated

through his audit report.”

4.

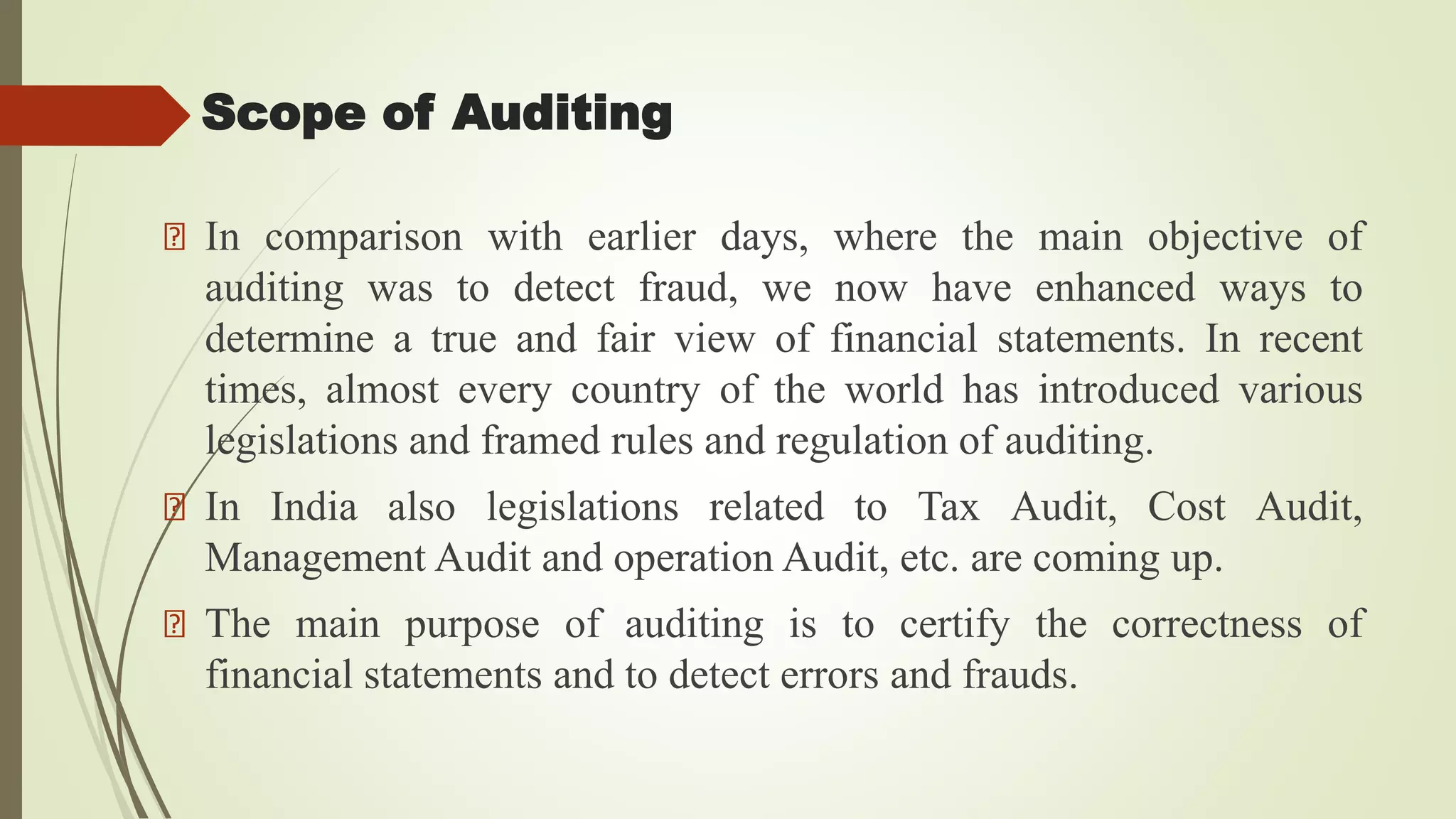

Scope of Auditing

Incomparison with earlier days, where the main objective of

auditing was to detect fraud, we now have enhanced ways to

determine a true and fair view of financial statements. In recent

times, almost every country of the world has introduced various

legislations and framed rules and regulation of auditing.

In India also legislations related to Tax Audit, Cost Audit,

Management Audit and operation Audit, etc. are coming up.

The main purpose of auditing is to certify the correctness of

financial statements and to detect errors and frauds.

5.

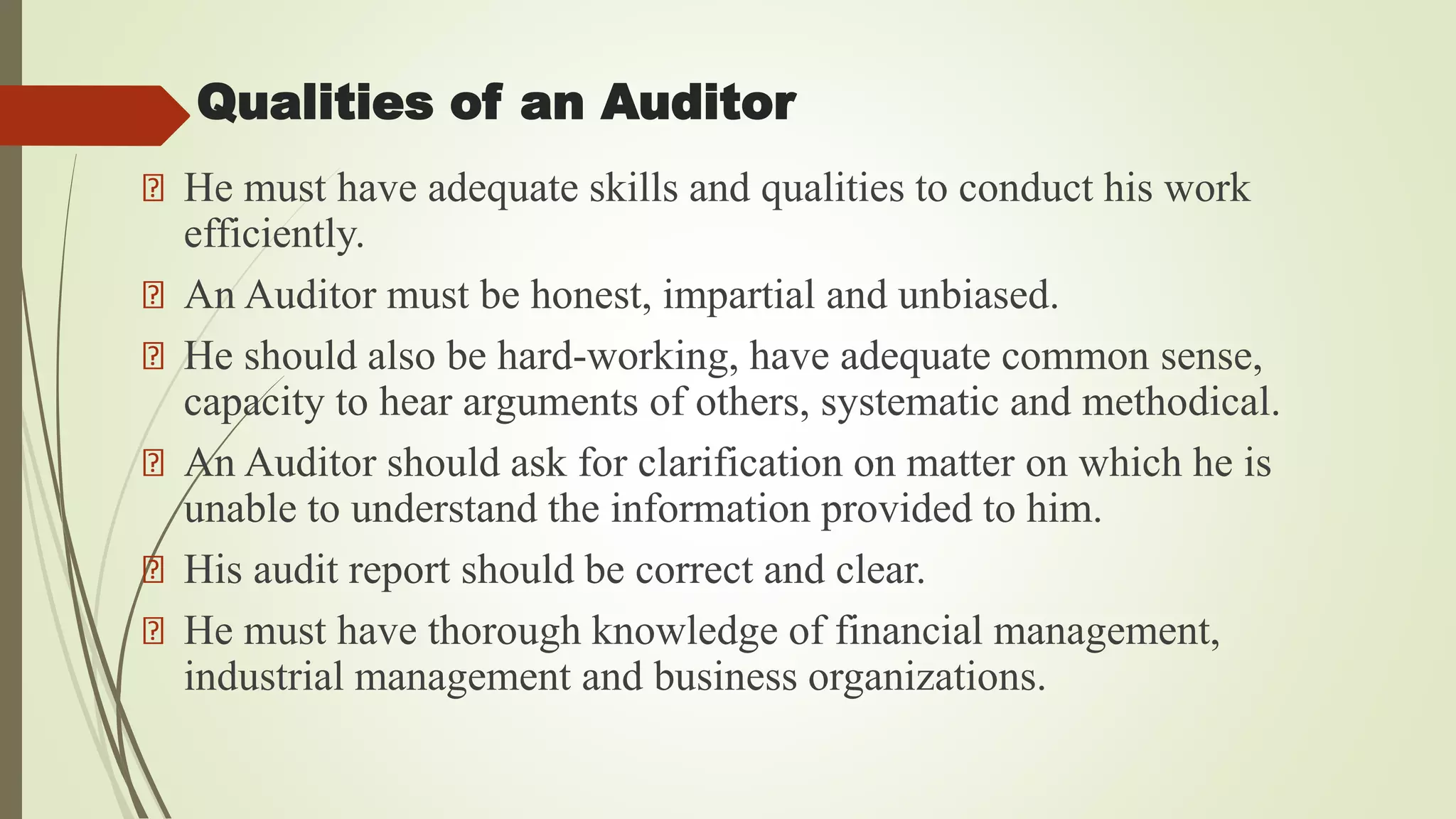

Qualities of anAuditor

He must have adequate skills and qualities to conduct his work

efficiently.

An Auditor must be honest, impartial and unbiased.

He should also be hard-working, have adequate common sense,

capacity to hear arguments of others, systematic and methodical.

An Auditor should ask for clarification on matter on which he is

unable to understand the information provided to him.

His audit report should be correct and clear.

He must have thorough knowledge of financial management,

industrial management and business organizations.

6.

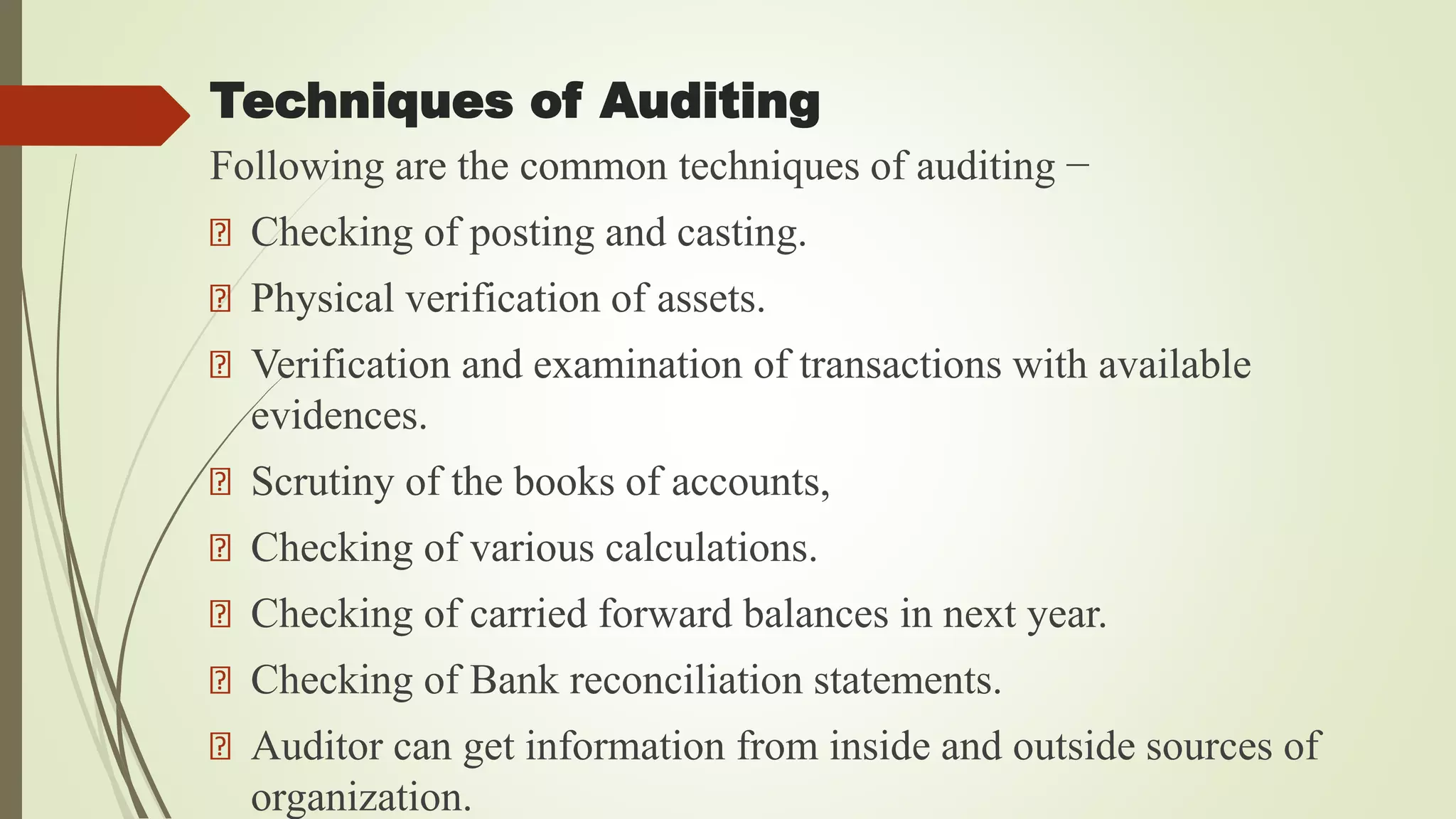

Techniques of Auditing

Followingare the common techniques of auditing −

Checking of posting and casting.

Physical verification of assets.

Verification and examination of transactions with available

evidences.

Scrutiny of the books of accounts,

Checking of various calculations.

Checking of carried forward balances in next year.

Checking of Bank reconciliation statements.

Auditor can get information from inside and outside sources of

organization.

7.

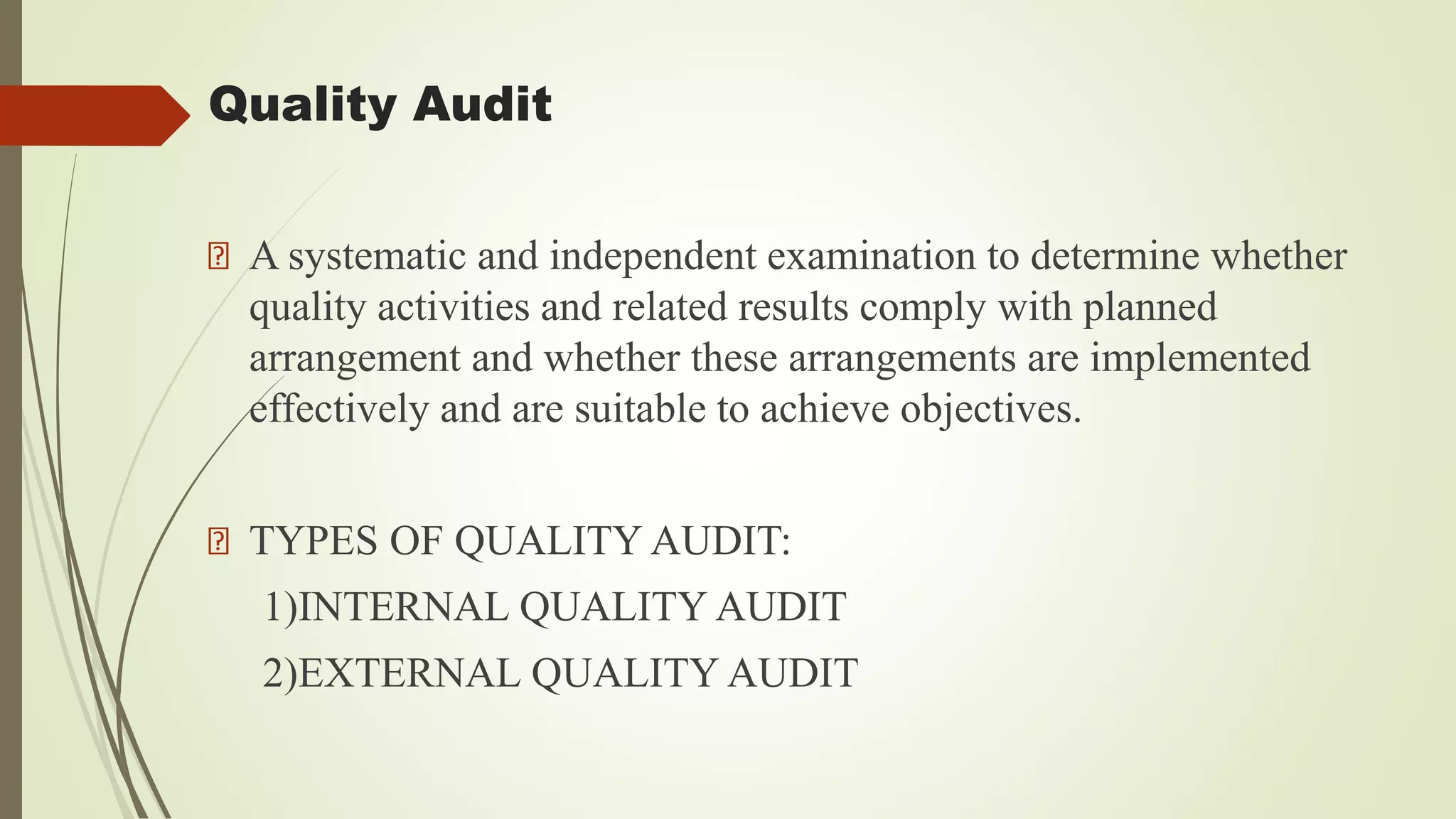

Quality Audit

A systematicand independent examination to determine whether

quality activities and related results comply with planned

arrangement and whether these arrangements are implemented

effectively and are suitable to achieve objectives.

TYPES OF QUALITY AUDIT:

1)INTERNAL QUALITY AUDIT

2)EXTERNAL QUALITY AUDIT

8.

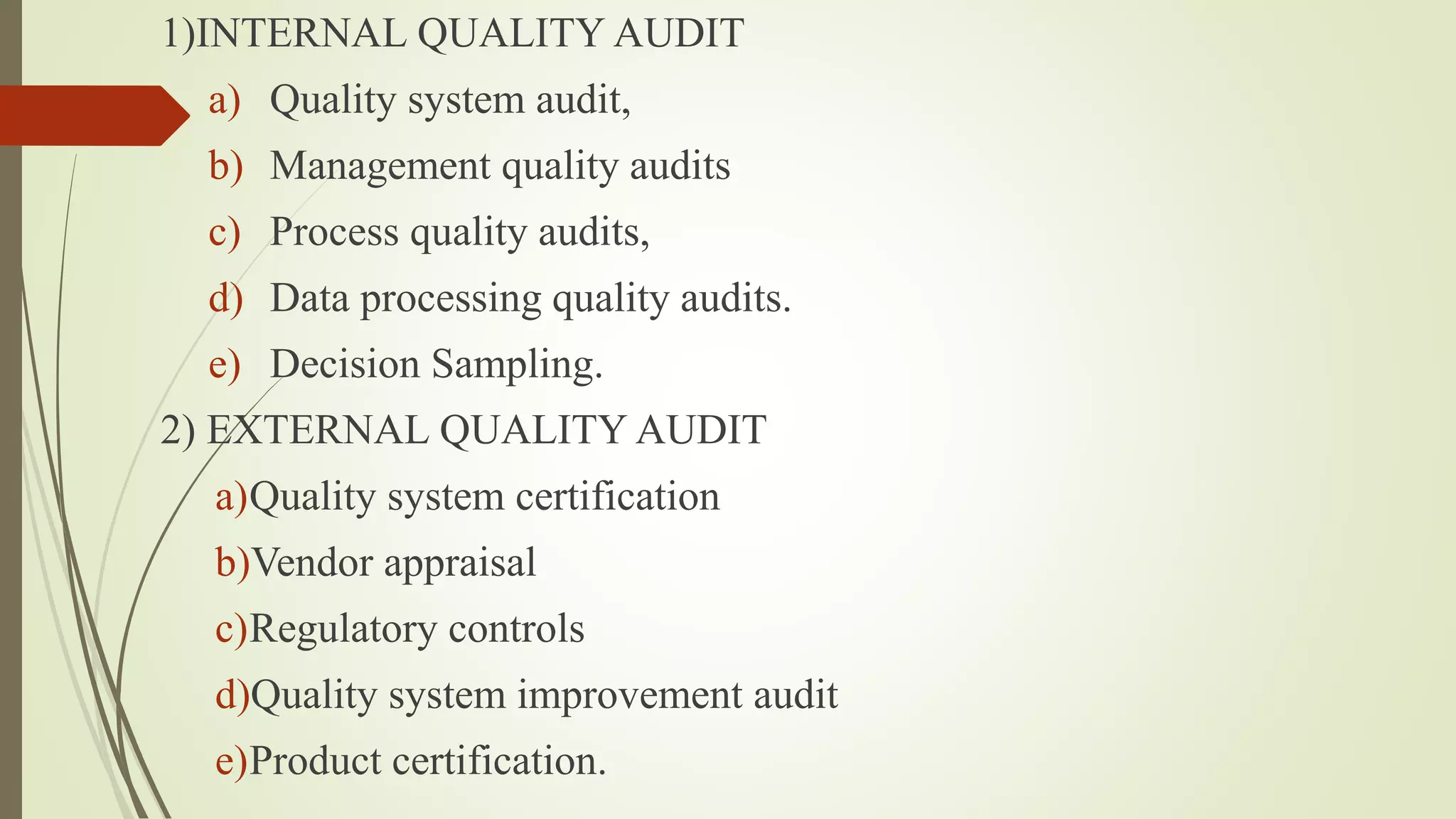

1)INTERNAL QUALITY AUDIT

a)Quality system audit,

b) Management quality audits

c) Process quality audits,

d) Data processing quality audits.

e) Decision Sampling.

2) EXTERNAL QUALITY AUDIT

a)Quality system certification

b)Vendor appraisal

c)Regulatory controls

d)Quality system improvement audit

e)Product certification.

9.

Objectives of Audits

Thereare Three type of objectives of auditing are discussed

as follow;-

A) PRIMARY OBJECTIVES

B) SECONDARY OBJECTIVES

C) SPECIAL OBJECTIVES

10.

A ) PRIMARYOBJECTIVES

The Primary objectives of auditing are as below;-

1) FAIRNESS OF STATEMENTS: The purpose of auditing is to

determine the fairness of statements. The financial statements can

show true and fair view after auditing. Due to limitations of

financial statements it is not possible to provide cent percent

accuracy, So an attempt is made to show the fair view of financial

statements.

2) PRESCRIBED LAWS: The purpose of the audit is to check that

prescribed laws have been followed in the preparation of financial

statements. There are various laws that govern the working of

many businesses. The auditor can indicate whether the prescribed

laws were followed in the preparation of final accounts.

11.

3) ACCOUNTING POLICIES:The purpose of auditing is to

examine the accounting policies. There is need to follow the

accounting policies for preparing accounting records. The effective

accounting system can provide better results. The auditor can

express an opinion on the accounting policies in the best interest of

business.

4) INDEPENDENT OPINION: The purpose of the audit is to

express an independent opinion. The auditor must be honest in his

work. Management and other persons must not influence him

There must be high ethical standard for independent reporting.

12.

B) SECONDARY OBJECTIVES

TheSecondary objectives of auditing are as below;-

1. DETECTION OF ERRORS: The purpose of auditing is to detect

the errors. The auditor can use ways to find out errors in the accounting

records.

2. DETECTION OF FRAUDS: The purpose of auditing is to detect

frauds. The management is responsible for the detection of frauds. The

management can take steps to correct the wrong effects of frauds for

the benefit of owners.

3.PREVENTION OF FRAUDS: The purpose of auditing is to Prevent

frauds. In accounting, it includes manipulation or alteration of records

and misappropriation of assets, an omission of the effects of the

transaction from records or documents, recording of the transaction

without substance and misapplication of accounting policies.

13.

C SPECIAL OBJECTIVES

TheSpecial objectives of auditing are as below;-

1. MANAGEMENT AUDIT: The purpose of management audit is to assess the

performing, review the organizational structure and suggest the best course of

action. It is a voluntary audit.

2. TAX AUDIT: The purpose of auditing is to satisfy the taxation officers. These

can be conducted to determine the income. The sole proprietors and partnership

firms can settle their tax matters through tax audit

3. SOCIALAUDIT: The purpose of the social audit is to measure social

performance of the business. The society is concerned with the Protection of natural

environment The social audit can examine the business performance of the society.

4. PROPRIETY AUDIT. the purpose of propriety audit is to examine the proper

use of money. There is a requirement of economic use of resources in the best

interest of business. There must be a justification for spending every rupee for the

benefit of business. The audit can determine the wise use of money.

14.

5. COST AUDIT:The purpose of cost audit is to verify the correctness of cost

accounts. The management must have followed the cost objectives in

maintaining books and other records. The cost audit can help the management

to improve the efficiency in doing business.

6, OPERATIONS; The purpose of operations audit is to prevent misuse of

resources It is a part of social audit The management must use prudence in

spending money. There is need of intelligent use of resources for optimum

output with lowest possible cost.

7. BID OFFER: The purpose of the audit is to determine the real value of the

business forbid offer. The value of net tangible assets becomes the basis of

Sales. The bidders can offer bid price on the basis of such price. The audited

accounts serve as a guideline to arrive at a certain decision.

8. PURCHASE CONSIDERATION: The purpose of the audit is to determine

the purchase price of a business. The audited accounts determine value of assets

and liabilities. The buyers and sellers Come to know the real value of a

business. They can make a deal to amalgamate or merge business.

15.

9. LOAN: Thepurpose of the audit may be a loan. The

management can approach banks and other lenders. The bankers

rely on audited accounts for the supply of money. The audited

accounts are legal requirements of the loan facility.

10. ADMISSION: The purpose of the audit may be an admission

of a partner. The audited accounts can provide information to new

as well as old partners. They can decide terms and conditions for

admission. The value of assets and liabilities is agreed upon.

11. PROFITS: The purpose Of audit may be checking variations

in profits. The fluctuation in profits can be analyzed by an expert

auditor. The file of business depends on reasonable profits.

16.

Management of Audit

Isa systematic examination of decisions and actions of the

management to analyse the performance.

audit involves the review of managerial aspects like

organizational objective, policies, procedures, structure, control

and system in order to check the efficiency or performance of

the management over the activities of the Company.

Audit management helps simplify and well-organise the work

flow and collaboration process of compiling audits.

Most audit teams heavily rely on email and shared drive for

sharing information between each other.

17.

Typically task suchas submitting client request, sender reminder

and following up on findings are all done from using broad

tools.

Audit management oversees the internal/external audit staff,

establishes audit programs, and hires and trains the appropriate

audit personnel.

The staff should have the necessary skills and expertise to

identify inherent risks of the business and assess the overall

effectiveness of controls in place relating to the company's

internal controls.

18.

To manage anaudit team in a manner to achieve good

results, it is important that audit managers have strong

leadership skills,

Auditing involves planning, method, facts, procedures,

controls, risk, and management.

Communication skills is key to many successful auditors.

19.

Responsibilities

1) Appointing responsibleindividual (s) to work with the

auditor(s)

2. Providing a work area and facilities for the auditor

3. Ensuring auditor(s) access to the necessary facilities

4. Attending specific meetings with the auditor (s)

5. Reviewing the audit findings to ensure agreement with

the facts.

20.

Responsibilities

A. Team LeaderResponsibilities

➢Make final decision for all phases of the audit.

➢Prepare Audit Plan.

➢Brief the team.

➢Review working documents to ensure adequacy.

➢Report critical nonconformities to the auditee

immediately.

➢Report any major obstacles encountered during the audit.

➢Represent the audit team at opening and closing meetings.

➢Submit the audit report.

21.

B. Team MemberResponsibilities:

➢Prepare any work documents (Including check-list)

necessary to carry out those tasks.

➢Review all relevant information related to their assigned

tasks.

➢Report deficiencies and audit findings to team leader.

➢Communicate the audit requirements to the auditee.

➢Collect objective evidence from the audit.

➢Report the audit findings to auditee.

➢Verify corrective actions taken in response to CAR’s

22.

References

https://www.wikihow.com/Manage-Auditors-and-

Regulators.

"Audit, accounting andreporting". Retrieved 4 Nov 2015.

"Help your teams become more audit efficient with ACL's

audit management solution". 4 Feb 2015. Retrieved 29

Oct 2015.

"MANAGEMENT AUDIT". Retrieved 3 November 2015.

"Communication Skills for Auditors". Retrieved 3 Nov 2015.

https://en.wikipedia.org/wiki/Management_auditing.

Audit Plan https://en.wikipedia.org/wiki/Audit_plan

![AUDIT REPORT [ AUDITING ]](https://cdn.slidesharecdn.com/ss_thumbnails/auditingtypesofauditreport-210303052610-thumbnail.jpg?width=640&height=640&fit=bounds)