Download to read offline

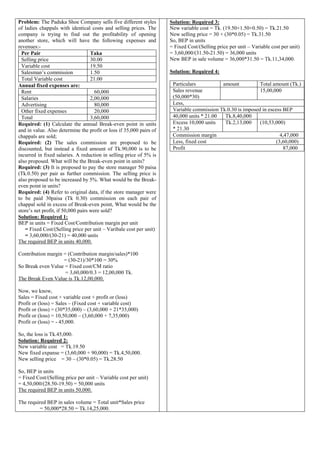

The break-even point is the level of output or sales at which total revenue equals total costs. It represents the point at which a company neither makes a profit nor a loss. The document discusses break-even analysis, including its assumptions, limitations, and applications. It also provides an example problem calculating break-even points, contribution margins, and profits for a shoe company considering opening a new store.