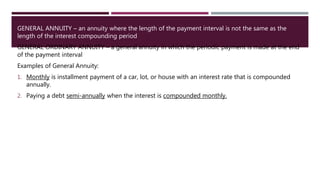

This document discusses general annuities where the payment interval is different from the compounding period. It provides examples of general annuities including monthly car payments with annual interest compounding and semi-annual debt payments with monthly compounding. The document also presents the formulas for calculating the future and present value of a general ordinary annuity. It includes two examples of using the formulas to solve problems involving equivalent interest rates, payment amounts, and time periods.

![Example 1. Cris started to deposit P 1,000.00 in a fund that pays 6% compounded quarterly. How much will be in

the fund after 15 years?

Given: R = P 1,000.00 n = (12)(15) = 180 payments i(4) = 0.06 = 4

(1) Convert 6% compounded quarterly to its equivalent (2) Apply the formula in finding the future value of an

interest rate for monthly payment interval. ordinary annuity using the value computed equivalent

rate.

F1 = F2

P{(1 + i(12))/12)} (12)t = P{(1 + i(4))/4)} (4)t

{(1 + i(12))/12)} (12) = {(1 + 0.06/4)} (4)

{(1 + i(12))/12)} (12) = (1.015)4

{(1 + i(12))/12)} = {(1.015)4} (1/12)

i(12))/12 = (1.015)(1/3) – 1

i(12))/12 = 0.00497521 = j

F = R [(1 + j)n – 1)/j)]

F = P 1,000.00[(1 + 0.00497521)180 – 1)/0.00497521]

F = P 290,082.51

Thus, Cris will have P 290,082.51 in the fund after 20

years.](https://image.slidesharecdn.com/lesson8-generalannuity-200930072214/85/Lesson-8-general-annuity-4-320.jpg)

![Example 2. A teacher saves P 5,000.00 every 6 months in a bank that pays 0.25% compounded monthly. How

much will be her savings after 10 years?

Given: R = P 5,000.00 n = (2)(10) = 20 payments i(12) = 0.25% = 0.0025 m = 12

(1) Convert 0.25% compounded monthly to its equivalent (2) Apply the formula in finding the future value of

an

interest rate for each semi-annual payment interval. ordinary annuity using the value computed

equivalent rate.F1 = F2

P{(1 + i(2))/2)} (2)t = P{(1 + i(12))/12)}(12)t

{(1 + i(2))/2)} (2) = {(1 + 0.0025/12)} (12)

{(1 + i(2))/2)} (2) = (1.00020833)12

{(1 + i(2))/2)} = {(1.015)12} (1/2)

i(2))/2 = (1.00020833)(6) – 1

i(2))/2 = 0.00125063 = j

F = R [(1 + j)n – 1)/j)]

F = P 5,000.00[(1 + 0.00125063)20 – 1)/0.00125063]

F = P 101,197.06

Thus, the teacher will be able to save P 101,197.06 after

10 years.](https://image.slidesharecdn.com/lesson8-generalannuity-200930072214/85/Lesson-8-general-annuity-5-320.jpg)